Submitted by QTR’s Fringe Finance

Friend of Fringe Finance Lawrence Lepard released his most recent investor letter this week. He gets little coverage in the mainstream media, which, in my opinion, makes him someone worth listening to twice as closely.

Larry was kind enough to allow me to share his thoughts heading into Q2 2024. The letter has been edited ever-so-slightly for formatting, grammar and visuals.

This is Part 2 of his letter, Part 1 was released earlier this week.

STOCK MARKET UPDATE

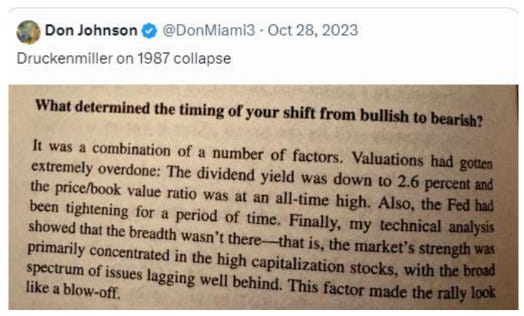

The U.S. Stock Market is very overvalued and vulnerable to a significant correction. We cannot predict how or when this correction will occur. This tweet regarding Stan Druckenmiller’s reflection of the 1987 crash sounds awfully familiar with recent times.

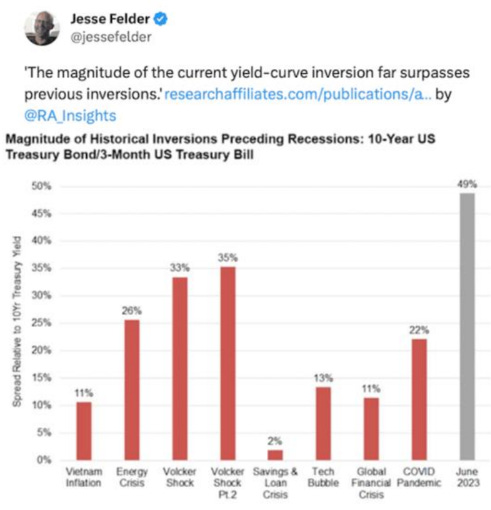

We note the following three data points in today’s markets: First, as shown in the tweet below by Jesse Felder, the magnitude of the yield curve inversion that took place during this Fed rate hiking cycle is historically large and all of these prior events led to recessions.

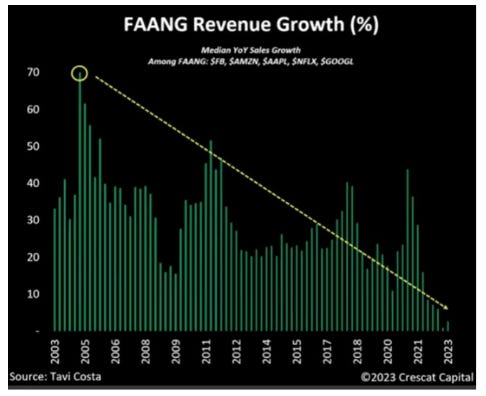

Second, the U.S. Stock Market performance has been driven by the FAANG stocks and the Magnificent 7. As the chart below shows, there is a distinct slow-down in the revenue growth of these stocks.

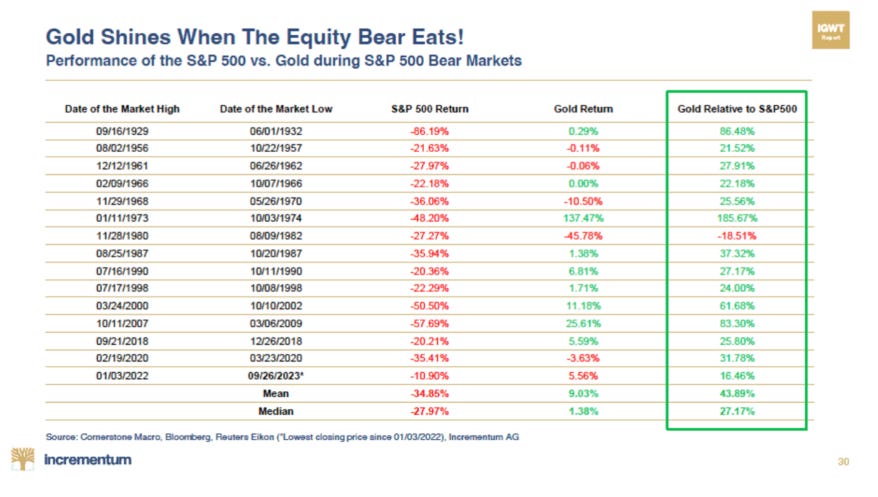

Our final point would be that when this equity market declines, all of that capital will be looking for a new home that is performing well. Notably, as shown in the excellent chart below by Ronni Stoeferle, gold does extremely well on a relative basis during equity bear markets.

INFLATION UPDATE

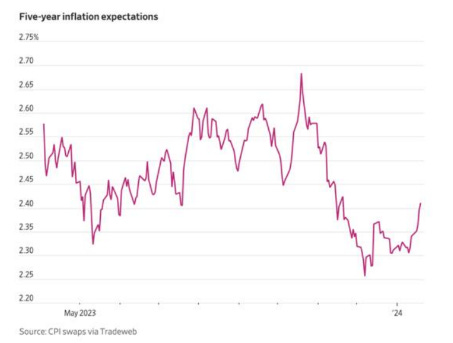

One reason the stock market has marched higher (and gold has been rather contained) is the consensus view that inflation is contained and will return to the Fed’s 2% target rate. The chart below shows these expectations, but note they are changing.

When it comes to inflation projections, we will take the over. Recent data suggests that inflation is sticky in the 3.0-3.5% range and the Fed is going to have a difficult time achieving their target. This does not come as a surprise to us as we believe that we reached “peak deflation” in March 2020 and since that time we now live in an inflationary world.

History shows that once inflation is let loose, it is difficult to contain. We have often referred to the three waves of inflation which occurred in the 1970s. We think the next decade will look very similar. The following charts show inflation appears to be an ongoing problem. We start with a look at wage and salary inflation, which we can see is running at roughly 6% per year and a far cry from the 2% target.

Next, we can see that roughly 30% of companies surveyed intend to raise prices in the next year and that commodity prices are rising again.

In our opinion, inflation is not dead, or under control, and as the next wave up unfolds it will present real problems for the stock and bond markets and it will fuel continued growth in the prices of sound money assets.

WHAT IS DRIVING THE GOLD BREAK OUT?

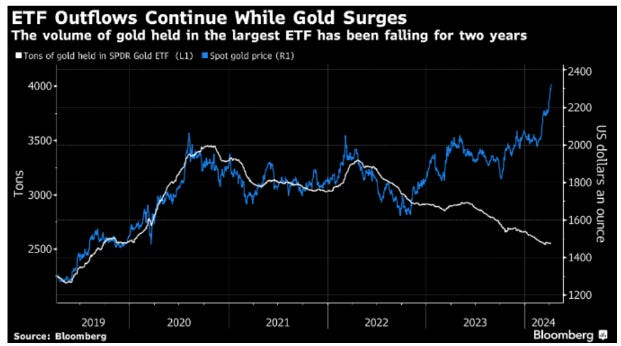

One of the more interesting developments of the quarter is that we have seen Western ETFs like GLD (the largest gold ETF) shrink in size while the price of gold has gone on to reach record highs.

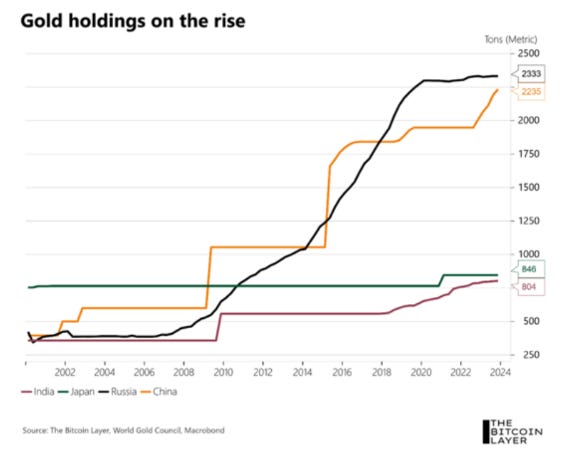

Yet gold prices rose despite U.S. ETF withdrawals due to the relentless gold buying by global Central Banks – particularly from China. The US 10 Year Treasury bond used to be the World’s Reserve Asset. However, in 2014, foreigners reduced their buying of treasuries and increased their buying of gold. Accordingly, foreign treasury holdings have decreased while gold holdings have increased.

In particular, China and Russia have been enormous buyers:

GOLD IS REPLACING TREASURIES AS THE NEUTRAL RESERVE ASSET

We believe there are a lot of reasons for this buying on the part of foreigners and foreign Central Banks and we will touch on a few of them. First, there was the Russian invasion of Ukraine and the U.S. Treasury seized over $600B of Russian assets stored in the U.S. Banking system. This seizure sent chills into all countries that held financial assets in the United States. Suddenly, theoretically risk-free assets held in the U.S. system were not so “risk-free”.

🔥 50% OFF ALL SUBSCRIPTIONS: Subscribe and get 50% off and no price hikes for as long as you wish to be a subscriber.

Second, the behavior of the United States in weaponizing the dollar accelerated the trend toward countries using their native currencies to trade with each other instead of using the U.S. dollar to purchase oil. This is a huge deal because oil is the largest commodity market and oil being priced in dollars created a huge bid for dollars and by extension U.S. Treasury securities as well. We have seen many of the Gulf State Countries and Russia, India, and China moving their oil trade into Yuan, Rubles, and Rupees. These alternative currencies can be settled and then exchanged back for goods and services or if imbalances exist, they can be exchanged for gold as a neutral reserve asset versus dollar-denominated assets.

We think that this trend is hugely important and is helping to drive the price of gold much higher since the gold market is much smaller than the oil market. Brilliant macro analyst Luke Gromen has been all over this and has a thesis that gold is becoming an oil-based currency. We agree and note that this is very positive for the price of gold. Tavi has a few excellent charts that lay out this trend very clearly and also show how early we are given how low the ratio of gold as a % of International Reserves is vs. 1980.

THE CASE FOR GOLD AND MINERS

In spite of the trend toward central banks favoring gold over bonds, the average U.S. investor has not caught on yet. As the charts below show almost no one owns gold or gold mining equities. And as the chart above on page 16 shows, U.S. investors are selling the biggest gold ETF, GLD. By the way, we expect this trend to reverse, and it will turbocharge gold prices upwards going forward. The following two charts show the weighting of gold versus other assets. As people become aware of the gold price break-out and the increased portfolio performance achievable by owning gold, the numbers shown in the charts will change significantly and create increased room for higher gold prices. Today, we estimate that Gold and Gold Miners are only 2% of global assets vs. 20-30% at the end of prior bull markets shown below:

If you are a fan of technical analysis the next chart provides an interesting perspective of what could unfold if we enter into a full-fledged bull market for gold. It is not uncommon for gold to appreciate by multiples in gold bull markets. For example, from 1971 to 1980 the gold price went from $35 to $800 which is 22x the starting level. In the 2000 example gold went from $260 to 1,900 or 7x the starting level. This bull market began at $1,050 in December 2015. We are up to $2,300 or over 2x the starting level. With the severe monetary dysfunction that we have outlined above we see no reason why the endpoint of this bull market could not be a similar multiple. Even if we do not get to 22x or 7x as in previous bull markets, we will achieve outstanding fund performance even if gold only gets to $3,000 per ounce.

GOLD MINERS ARE DEEPLY MISUNDERSTOOD

Many of our investors have asked us “Hey gold is doing well. Why are the gold and silver miners such dogs?” There are a number of reasons. The first is that the U.S. stock market has been an Energizer Bunny and has managed to bounce back strongly from every correction in its relentless path upward. When your existing portfolio is performing well, the need to diversify and think about alternatives is diminished. Secondly, we believe that some investors still suffer from “battered gold stock bull syndrome.” The market downturn in gold stocks from 2011 to 2015 was so severe and devastating that many investors concluded that gold stocks were un-investable. And investors were not off base because of how poorly some of the companies in the industry are managed with continual dilution and wasteful spending. Stock picking skills are very important in this sector.

But, we believe that the primary reason why the stocks have underperformed is the combination of rising mining costs and the expectation of flat gold prices.

Gold mining is really a spread business. The gold miners own deposits in the ground (measured via 43-101 compliant reports) and then spend money (CAPEX) to develop the mining capacity to pull these ounces out of the ground and sell them. So, the cost to mine is the initial CAPEX investment, plus the actual cost per ounce to operate the mine, once built. These mining costs are measured in two ways. First, there is the cash cost to mine an ounce which represents the total cash amount spent to extract the metal (labor, explosives, oil, energy, etc.). Industry-wide, today average cash costs are in the range of $900 to $1,000 per ounce mined.

The problem with cash costs per ounce is that they reflect the bare minimum costs and do not account for the cost of replacing the ore which was mined and the on-going CAPEX to keep the mine running. With this in mind, the industry established a new performance metric called All-In-Sustaining-Cost (ASIC). ASICs are larger than cash costs and more accurately reflect the true profit per ounce mined. Industry average ASICs today are roughly $1,350 per ounce but this is up sharply from a pre-COVID level of closer to $1,000 per ounce.

Mining ASICs have not been immune to global inflation; costs have been increasing by 10-12% per year. This becomes a problem if the price of gold does not appreciate by the same amount. This is the primary reason why the gold stocks trade so poorly. As it turns out the world still thinks we are returning to a low inflation environment and that gold prices will be stagnant. Our friend summarizes this in his excellent Tweet below pointing out that Bloomberg Analysts’ median consensus price of gold is only $1,725 in 2028. If ASIC costs only inflate by 8%/ year, the average cost of mining an ounce of gold will be $1,836 in 2028. The entire industry would be unprofitable. No wonder the stocks trade horribly.

Of course, our view is that there is no way in hell that the gold price will only be $1,725 in 2028. We expect it to be between $3,000 and $5,000 per ounce. Using our estimate, the gold miners will be wildly profitable and the stocks will trade at multiples of their current values. Another factor that has contributed to the malaise in the gold stocks is that investors still remember the 2003 to 2018 period when, with a few years of exception, the gold miners were deeply cash flow negative. This led to the industry cleaning up their act in 2018 so that higher prices in 2019 and 2020 led to significant free cash flows. Note how in 2021 and 2022, these cash flows tapered off as ASICs marched higher and the gold price remained stuck in the $1,900 to $2,000 range. As Tavi’s chart suggests, with the current break out in the gold price, the spread between the selling price and ASICs is about to widen again, which will drive the stock prices much higher.

When we talk to investors, we explain that there are three things that will make a gold stock go up.

1. The company expands its production and mines more ounces to drive cash flows higher.

2. Gold prices go up and profit margins expand (higher operating leverage on fixed cost business).

3. The stock multiple expands as investors are willing to pay more for a growing free cash flow stream.

We strongly believe that we are about to enter a positive feedback loop on all three of the above. We have selected companies that have invested intelligently and will increase their production capacity in the years ahead.

We expect the price of gold to go up and because of the operating leverage, a 30% increase in the price of gold can lead to a 100% increase in operating cash flow. Multiples of cash flow are incredibly low, and we have many companies that are trading at 3-5x cash flow vs. 10x to 20x at bull market peaks. You can see why we are so excited about the opportunity to multiply our capital in this sector at this time.

This next chart shows a ratio of just how cheap mining stocks are vs. the price of the metal. The chart shows the XAU Gold and Silver stock index divided by the price of gold. Note how the XAU index has declined to a record low versus the gold price with perhaps the exception of 2015 and the brief spike down in March 2020. If this ratio were to return to its historical mean, the gold stocks would go up 3x from here, and consider that the price of gold may be higher too making the absolute return even higher.

CONCLUSION

Let’s face it: the past three years have been tough, especially for those of you who joined us at the peak in 2020 and did not participate in the…(READ MORE).

Now read:

- “The Federal Reserve Is Clearly Trapped”: Lawrence Lepard

- Hard Money Heat Check

- Did Lockdowns Set a Global Revolt in Motion?

- Trading The Sh*t Show: April 2024 Portfolio Review

- The “Holy Grail” Of Precious Metal Stocks: Harris Kupperman

- The Musk Of Desperation

- “Havana Syndrome”: Russian Aggression or Media Conspiracy Theory?

- “What I’m Smelling Just Don’t Smell Right”: Phil Bak

- Bitcoin Redundancy Realizations

QTR’s Disclaimer: I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have not been fact checked and are the opinions of their authors. They are either submitted to QTR, reprinted under a Creative Commons license or with the permission of the author. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Larry’s Disclaimer: These presentation materials shall not be construed as an offer to purchase or sell, or the solicitation of an offer to purchase or sell, any securities or services. Any such offering may only be made at the time a qualified investor receives from EMA formal materials describing an offering plus related subscription documentation (“offering materials”). In the case of any inconsistency between the information in this presentation and any such offering materials, including an offering memorandum, the offering materials shall control.

Securities shall not be offered or sold in any jurisdiction in which such offer or sale would be unlawful unless the requirements of the applicable laws of such jurisdiction have been satisfied. Any decision to invest in securities must be based solely upon the information set forth in the applicable offering materials, which should be read carefully by prospective investors prior to investing. An investment in EMA not suitable or desirable for all investors; investors may lose all or a portion of the capital invested. Investors may be required to bear the financial risks of an investment for an indefinite period of time. Investors and prospective investors are urged to consult with their own legal, financial and tax advisors before making any investment.

The statements contained in this presentation are made as of the date printed on the cover, and access to this presentation at any given time shall not give rise to any implication that there has been no change in the facts and circumstances set forth in this presentation since that date. These presentation materials may contain forward-looking statements within the meaning of US securities laws. The forward-looking statements are based on EMA’s beliefs, assumptions and expectations of its future performance, taking into account all information currently available to it, and can change as a result of known (and unknown) risks, uncertainties and other unpredictable factors. No representations or warranties are made as to the accuracy of such forward-looking statements. EMA does not undertake any obligation to update any forward

looking statements to reflect circumstances or events that occur after the date on which such statements were made. Historical data and other information contained herein, including information obtained from third-party sources, are believed to be reliable but no representation is made to its accuracy, completeness, or suitability for any specific purpose.

No representation is being made that any investment will or is likely to achieve profits or losses similar to those shown. Past performance is not indicative of future results. This report is prepared for the exclusive use of EMA investors and other persons that EMA has determined should receive these presentation materials. This presentation may not be reproduced, distributed or disclosed without the express permission of EMA.

Tyler Durden

Sun, 04/21/2024 – 10:30