Authored by David Stockman via InternationalMan.com,

Every headline in the financial press earlier this week says the same thing. The Fed’s “Great Pause” has now commenced.

The Federal Reserve raised interest rates by a quarter point—and could be done.

Well, they might be done “raising” rates, but they shouldn’t be in the rate setting business—up, down or sideways— in the first place. That’s because market capitalism doesn’t work if financial asset prices are being pegged artificially and falsely by a 12-man monetary politburo rather than the vast throng of suppliers and users of funds in the global marketplace.

Here is the madness that rate pegging has led to over the last 22 years.

To wit, the Fed has made overnight money so ungodly cheap that it has distorted, tortured and twisted the very warp and woof of the entire financial system. All financial asset prices have been drastically falsified because 221 months of negative carry costs in real terms have triggered reckless leveraged speculations, rampant options chasing and dangerous financial asset arbitrages like never before.

Inflation-Adjusted Fed Funds Rate Since October 2001

Alas, none of this is stable or sustainable. So here we are with another day in which the stock market is open, and like clockwork a new batch of regional banks are hitting the skids.

% Stock Price Change Today/From Recent Peak:

-

PacWest: -50%/-93%;

-

First Horizon: -33%/-55%;

-

Western Alliance: -40%/-84%;

-

Zions Bancorp: -12%/-73%

In all, this batch of plummeting regional banks posted a combined market cap of just $10.6 billion at last Thursday’s close, down from $40 billion at recent valuation peaks. And again, the collapse is not because trailing earnings have cratered.

In fact, the above four regionals posted $3.2 billion of net income in 2022, meaning that as a group they closed last Thursday’s session at just 3.2X trailing net income.

Obviously, investors and traders are spooked big time not by trailing results, but by what is surely coming down the pike. The combination of faltering asset books and fleeing deposits is just plain deadly, as KBW CEO Tom Michaud said on CNBC today:

Investors are very nervous, and I think what they’re nervous about is the fact that Silicon Valley lost 75% of their deposits in 36 hours. There’s not a bank in the world that could really sustain that….

To be sure, there is no mystery as to why these thundering bank runs are now underway. The Fed caused these banks to be flooded with absurdly cheap deposits, which, in turn, were pumped into higher yielding long-term debt securities (blue area), commercial real estate (red area) and business loans (black area).

The problem, of course, is that the cheap deposits are now fleeing with alacrity, while small bank loan and securities books are increasingly underwater. Sharply rising interest rates and an economy visibly sliding into recession will do that!

Stated differently, these deposits never had a chance of being permanent at 25 basis points or less. Likewise, there was nothing sound about asset books which grew by 10% per annum between 2014 and the present in the three above mentioned categories.

After all, during the same eight year period nominal GDP grew by only 3.2% per annum. Needless to say, true underlying demand for money at honest market rates did not grow at anything close to 3X GDP, meaning that these loans were not underwritten based on anything that even remotely resembled normal interest rates and a sustainable main street economy.

Growth Of Small Bank CRE loans, C&I loans and Treasury/Agency Debt Securities, 2014-2023

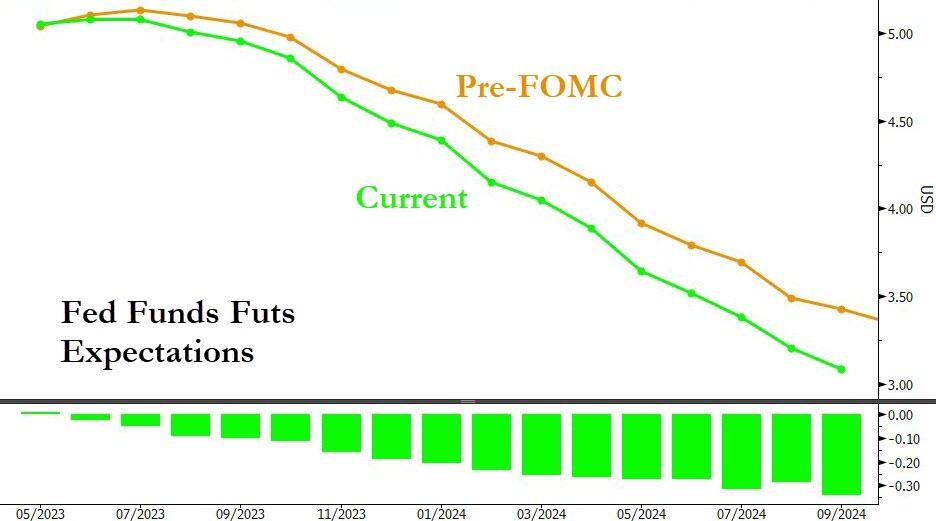

Now that a consequent cyclone is ripping through the small banking sector, this supposedly warrants a Fed pause, and then a sharp reversal to rate cuts during the second half of the year and unto 2024. In fact, the market is anticipating approximately 180 basis points of rate reductions from the Federal Reserve in the second half of this year and the first half of next year.

But that would truly be another case of Einstein’s famous definition of insanity—doing the same thing over and over and expecting a different result. The truth is, all three interest rate cutting sprees since the turn of the century—2001-2005, 2008-2011 and 2020-2022—were not remotely warranted. As shown in the first chart above, they simply drove real interest rates deeply underwater and caused the US economy to become submerged in excess debt, speculation and macroeconomic instability.

Indeed, each of these cheap money cycles fueled ever more reckless and excessive risk taking in the financial system. The resulting bubbles and malinvestments are now hitting the wall, with the small banking sector being simply the initial venue for the great reckoning underway.

This time, therefore, the Fed needs to let nature take it course, and purge the massive accumulated rot that has accrued in the financial system. To stop now and pivot to a fourth round of rate-cutting will only intensify the eventual conflagration.

However, the imperative at hand is not merely to persevere with the process of interest rate normalization, although that is surely warranted given that the Fed funds rate is still significantly negative in real terms. What normalization is actually about is not simply bringing the stubborn current inflation to heel, but the need for a regime change in terms of the Fed’s modus operandi.

To wit, both interest rate pegging and massive bond buying are terrible monetary policy mechanisms which are not fit for purpose. The latter causes long-term debt to be systematically under-priced, while pegging the overnight Federal funds rate is an exceedingly flimsy instrument of control that can’t hope to actually move the massive main street economy.

Indeed, yesterday’s commentary on bubble-vision in anticipation of the foregone conclusion that the Fed would raise its policy rate by 25 basis points told you all you need to know. One CNBC host even suggested that the fate of the world economy would therefore hang on Powell’s words, tone and eyebrow inflections.

Well, holy moly. We have a $26 trillion domestic economy and $90 trillion global economy composed of tens of millions of significant players, all pursuing the facts and their own best interests as they see it. Yet we are supposed to watch the eyebrows of one man, who was basically a so so Washington lawyer until elevated to the wanna be monetary politburo which is domiciled in the Eccles Building.

Sure enough, the Fed’s 25 basis point rate increase was ancient history within nanoseconds of its announcement. What mattered, according to the talking heads, was that one word had changed in the Fed’s post-meeting statement.

To wit, officials dropped a key word from their previous policy statement in March which said they “anticipated” some additional increases might be appropriate, and they replaced it with new language saying they would carefully monitor the economy and the effects of their rapid increases over the past year.

“That’s a meaningful change, that we’re no longer saying that we ‘anticipate’” additional increases, said Mr. Powell.

Well, give us a break!

What the Fed “anticipates” cannot possibly matter because the Fed has no idea what is coming down the pike. The have been wrong so often, so early and so unfailingly that their post-meeting statements are absolutely worthless—save for the speculative endeavors of fast money traders and robo-machines for a few seconds or minutes after their release.

In any event, the evident problem is that the Fed has backed itself into one hellacious corner. They are so addicted to interest rate pegging and manipulation that they cannot even see the absurdity of what they are actually doing.

To wit, since the turn of the century they have so thoroughly flooded the financial system with excess liquidity and cheap credit that they can no longer even peg their traditional instrument—the Fed funds rate.

That’s why they have set up what is called the O/N RRP facility in the trade. It stands for overnight reverse repo facility, and when you strip away all the Fed-speak, it amounts to a giant borrowing window operated by the FOMC’s technicians at Liberty Street.

Presently day in and day out they are “borrowing” $2.3 trillion for the account of a central bank that can print money at will; and, in fact, has expanded its balance sheet from $500 billion to a recent peak of $9 trillion during the last two decades.

Nevertheless, as recently a March 2021 these overnight borrowings at the Fed’s O/N RRP facility totaled only $1 billion (purple line). So there has been a 2,200X expansion of the facility during the last 24 months.

Say what?!

It’s actually very simple. The Fed needed to pretend that it was raising interest rates in a financial system flooded with rate-depressing excess liquidity. So it used the O/N RRP to set a floor under money market rates by sopping up massive amounts of excess liquidity, and then systematically raised the rate it pays overnight lenders from 5 basis points as recently as March 2022 to 480 basis points at present.

Outstanding Balances And Interest Rates On the Fed’s Overnight Reverse Repo Facility

So where does all the money come from that was definitely uninterested in lending to the Fed at 5 basis points but more than eager at a rate 96 times higher?

Why, it’s the money market funds, which are now laughing all the way to the bank, so to speak. And to continue with that metaphor, in fact, where does all the surging inflows to the money market funds come from?

Why, the regulated commercial banking system, and most especially the regional banks!

In a word, the Fed is so tangled up in the underwear of its own monetary mechanics that it is actually causing the regional banking system collapse, which, in turn, may soon become the excuse to stop rate normalization and initiate the same rate cutting disaster all over again.

So, yes, now is no time to stop. What is really needed is an end to Keynesian central banking and the abolition of monetary central planning.

* * *

The truth is, we’re on the cusp of an economic crisis that could eclipse anything we’ve seen before. And most people won’t be prepared for what’s coming. That’s exactly why bestselling author Doug Casey and his team just released a free report with all the details on how to survive an economic collapse. Click here to download the PDF now.

Tyler Durden

Sat, 05/13/2023 – 09:20