Summary (via BBG):

-

The Fed left interest rates unchanged in a range of 4.25%-4.50%, as expected. The big news was the downward revisions to growth forecasts and the upward revisions to inflation and unemployment projections (stagflationary). Policymakers now see much higher risks to their economic projections and also see higher uncertainty about the path of the economy.

-

In his press conference, Powell acknowledged that tariffs are already impacting the economy and have factored into economic forecasts. In fact, he said that the Fed has also factored in Reciprocal tariffs! Notably, and much to the anger of the left-leaning press corps, he said the base case remains for tariffs to have a transitory impact on inflation, but there’s a lot of uncertainty about that. Powell repeatedly dismissed notions that long-term inflation expectations were rising and added that the Fed doesn’t want to “get ahead” of surveys showing lower consumer sentiment. So far, he argued, the hard data is solid.

-

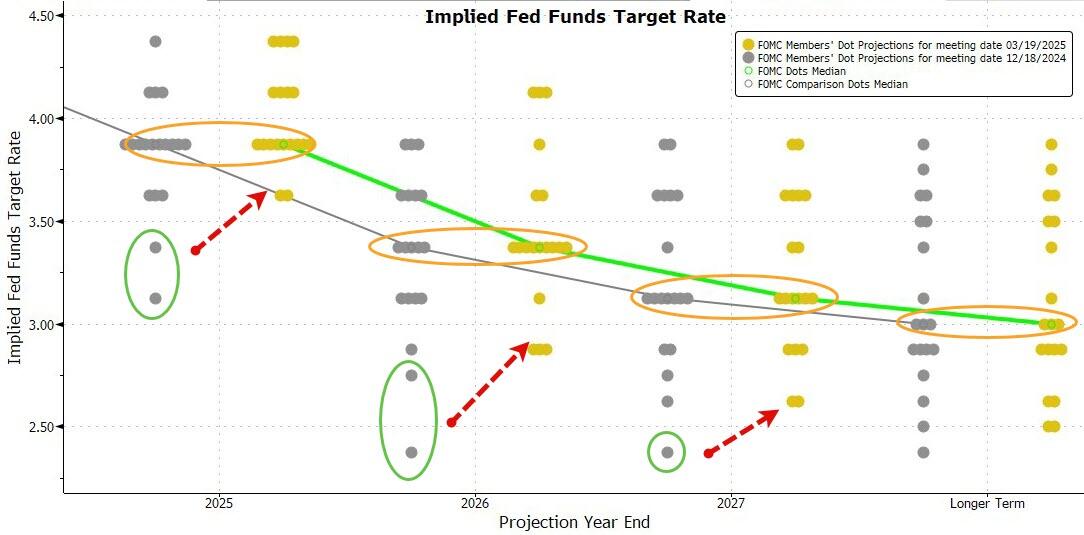

While the dot plot continued to show that policymakers expect two interest rate reductions this year, projections shifted to a significantly more hawkish stance compared with December’s forecasts. Eight participants now see just one or no cuts at all this year, and only two see three cuts.

-

QT Tapering: the Fed will slow the pace of runoff of its securities holdings beginning next month by cutting the monthly cap on Treasury securities redemption to $5 billion from $25 billion. It was a decision with broad support, Powell said, noting that participants preferred doing that to stopping quantitative tightening altogether. In other words, most believe the liquidity picture is starting to get challenging. Governor Chris Waller was the only one who dissented from the balance-sheet decision but supported the decision to hold rates steady.

-

Stocks and Treasuries rallied amid some relief that while the Fed boosted its inflation forecast, policymakers retained an expectation for rate cuts later this year. The S&P 500 was up 1.3% as of 3:33 p.m. in New York, heading for the best Fed day since 2022. Two-year yields were down 6 basis points,

The Fed is firmly in wait-and-see mode.

- Statement: hawkish

- Economic projections: mixed (stagflationary)

- Dots: hawkish

- QT taper: dovish

It’s interesting that the slowdown in QT is so sharp – from $25 billion down to $5 billion a month for the Fed’s Treasuries holdings.

Remember that it was $60 billion a month before the first slowdown.

Why not just cut it to zero?

Maybe the Fed wanted to send a signal that QT is still in place; it still wants to work down its balance sheet — and perhaps ramp the pace back up after the federal debt-limit standoff is over.

UBS sees a glimpse of a Powell Put:

Dare anyone say “Fed put”.

Perhaps not quite, but the Fed’s message is consistent with its work from September 2018 – that reacting to the inflationary consequences of tariffs only makes the growth hit worse than it needs be.

Not quite the “Fed put” the markets have been hoping for, but in the scheme of things, the outcome of the Fed is a little more dovish than the market had expected.

The Fed shrugging off the inflationary signals from its models and instead preferring to line the dot plot up with the growth deterioration.

Amid the uncertainties, the distribution of the dots for this year has actually narrowed.

* * *

Since the last FOMC meeting, on Jan 29th, a lot has changed…

From an economic perspective, growth expectations have plunged and inflation prints have been wildly noisy…

Source: Bloomberg

… (especially the idiotically partisan UMich inflation expectations)…

Source: Bloomberg

Gold has been the dramatic winner since the last FOMC meeting while oil and stocks have been clubbed like a baby seal. Bonds are bid but the dollar has been dumped…

Source: Bloomberg

Interestingly, as stocks have tumbled in the last two weeks, so have rate-cut expectations, back more in line with where they were after the last FOMC meeting (just 56bps now, from almost 100bps two weeks ago!)…

Source: Bloomberg

On the bright side, mortgage rates have plunged since the last FOMC meeting…

Source: Bloomberg

Finally, before everything goes just a little bit turbo, we note that the market is currently significantly more dovish than The Fed’s dots this year and dramatically more hawkish in 2027…

Source: Bloomberg

Rates are expected to be a nothingburger today.

So will today’s fresh Dot-Plot adjust to the market?

More importantly, what will The Fed do about its QT program?

Key Headlines:

As expected, no change in rates:

- *FED HOLDS BENCHMARK RATE IN 4.25%-4.50% TARGET RANGE

But, the economic projections are not pretty:

-

*FED SHARPLY REDUCES 2025 GROWTH PROJECTION, MARKS UP INFLATION

-

Fed cuts year-end GDP forecast from 2.1% to 1.7%

-

Fed raises year-end core PCE forecast from 2.5% to 2.8%

-

Fed raises year-end unemployment forecast from 4.3% to 4.4%

One of the fed members is very bearish on GDP growth…

Perhaps of most note:

Fed removes language that “risks to inflation and employment are roughly in balance”

Trump’s fault:

- *FED SAYS UNCERTAINTY AROUND ECONOMIC OUTLOOK HAS INCREASED

The median of the rate cut forecasts are unchanged from December (still at a two cut median)…

…but the dovish tails all shifted hawkishly…

-

four for 0 cuts in 2025 (up from just 1 in Dec)

-

four for 1 cut (up from 3 in Dec)

-

nine for 2 cuts now (down from 10 in Dec)

-

only two for 3 cuts (down from 3 in Dec)

-

and none of the FOMC members see 4 cuts in 2025 (down from 1 in Dec)

And finally, the QT Taper is on…

- *FED TO SLOW BALANCE-SHEET RUNOFF STARTING APRIL 1

Notably Fed’s Waller dissents because while he supported no change for the federal funds target range but preferred to continue the current pace of decline in securities holdings.

Read the full redline of the FOMC statement below:

Tyler Durden

Wed, 03/19/2025 – 15:40