Authored by Alasdair Macleod via GoldMoney.com,

With price inflation rising out of control and interest rates rising strongly, the trading environment for commercial banks has fundamentally changed. With bad debts looming and bond prices in entrenched downtrends, procrastination is now the enemy of bankers.

We are at the beginning of The Great Unwind, and this article elaborates on my first article for Goldmoney on the subject published here.

The imperative for bankers to respond to these conditions overrides all other matters if their businesses are to survive these changed conditions. We are entering a cyclical downdraft of the bank credit cycle which promises to be cataclysmic. And the monetary policy planners at the central banks can do nothing to stop it.

After outlining the scale of the problems faced by each global systemically important bank, this article looks at the future for the $600 trillion derivatives mountain.

It was born out of the long-term decline in interest rates from the mid-eighties, which ended last year. It is almost entirely distributed through banks and shadow banks.

The question to address is, what is the future for the derivative mountain, now that the long-term trend for falling interest rates is over? And what are the economic consequences?

If it’s you in the hot seat…

Imagine, for a moment, that you are the CEO of a commercial bank involved in lending to businesses and with profit centres acting in a range of financial activities. As CEO, you are answerable to the board of directors for the bank’s performance, and ultimately the bank’s shareholders for maintaining and advancing the value of their shares.

Furthermore, let us set this imaginary exercise in the present. These are the issues that should keep you awake at night:

-

In common with your competitors, the ratio of your balance sheet assets to total equity is almost the highest in the history of the bank, in many cases for other banks over twenty times leaveraged.

-

Official inflation, measured by the CPI is about ten per cent, and producer prices are rising somewhat faster. Your central bank expects a return to the 2% target in two- or three-years’ time. But your contacts at the central bank have privately admitted to you that they cannot imagine the circumstances where this would be true without a deep recession.

-

Bond yields are rising, and losses are beginning to impact on the bank’s investments. The bank has relatively little direct exposure to corporate bonds and equities, but they are commonly held as collateral against customer loans.

-

How are higher interest rates impacting the quality of the bank’s loan book? The bank supported its business customers through the covid pandemic, which increased the indebtedness of them all. This exposes the bank to excessive default risk if rates rise further.

-

The mortgage loan book has been a profitable business for decades. But the bank is beginning to see a material rise in delinquencies. If loan guarantees are not forthcoming from government agencies, the bank may have to shut this activity down.

-

What impact will higher interest rates have on the bank’s derivative exposure? What are the counterparty risks in derivative chains? Derivatives that involve inadequately capitalised counterparties should perhaps be sold on, or where the bank has the option to do so, closed down.

The underlying problem is that the conditions that led to the bank becoming increasingly involved in diversified activities, such as investment banking, trading, and investment management have now changed. Since financial deregulation in the 1980s, the bank has expanded into these profitable areas. The whole industry moved from dealing in credit into generating fee income. The growth in fee income can be directly related to the long-term trend of falling interest rates, which apart from interruptions such as the dot-com excesses and the Lehman crisis, stimulated growth in corporate finance, underwriting, investment management, and trading in financial securities. The expansion of these activities in turn led to a massive expansion of derivative markets, with new instruments being devised, such as credit default and interest rate swaps.

If, and this is really what should worry you, the long-term trend of falling global interest rates has ended and is now set to be reversed, not just temporarily but for the rest of the decade and perhaps beyond, then the reasons justifying the bank’s expansion away from its core lending business have come to an end. As CEO, how do you unwind the deep-rooted departmental interests, and keep the shareholders onside?

It is time for the whole executive to be urgently involved in a wide-ranging debate about how serious these threats might be and where you should take actions to protect the bank’s shareholders’ interests. Given the high level of balance sheet leverage, the bank’s survival is at stake if you act indecisively or too slowly. You are facing head-on the unpleasant prospect of The Great Unwind.

Balance sheet ratios

There are two ratios that concern bankers. The first is the relationship between liquid and illiquid assets with respect to sources of balance sheet funding. These are set by regulators through Basel regulations, now in their third iteration. Banks are required to submit details of their balance sheets periodically to bank regulators in accordance with the net stable funding requirement formula as set out in Basel III.

The second ratio is of less importance to regulators, which is the relationship between Tier 1 capital and the total balance sheet, which Basel regulations simply states that the maximum leverage ratio is for Tier 1 capital to not be less than 3% of the bank’s balance sheet assets. Put another way, subject to certain conditions, a bank can theoretically leverage its assets to equity as much as thirty-three times. But it should be noted that within that leverage ratio, a bank is permitted to net off certain classifications of credit, reducing its apparent balance sheet size. The following are examples of hidden forms of balance sheet assets and liabilities:

-

Security financing transactions, which include repos and other derivatives, can be netted off where they are between the same counterparty and maturity. For a true accounting picture, a bank balance sheet should reflect credit and debt obligations on both sides of its balance sheet until they are extinguished.

-

Long and short credit derivatives can be netted so long as there is no maturity mismatch. Again, the full obligations should be reflected on both sides of the balance sheet. And valuation methods give banks enormous wriggle room, an issue which regulators are unable to properly address.

-

Off-balance sheet items are only partially recognised through standardised credit conversion factors. Where a bank has off-balance sheet activities, they should be properly reflected in its accounts.

Therefore, true bank balance sheet leverage can be considerably greater than a bank complying with Basel regulations will declare in its audited accounts. But while conforming with Basel regulations, the board of a bank has a primary duty, often forgotten even by some directors, to their shareholders.

It is changes in the ratio between a bank’s assets and its shareholders’ equity which drive the cycle of bank credit expansion and contraction, which in turn drives the business cycle.

While they have a specific expertise in assessing lending risk, bankers are human. When they perceive lending risk to decline, they increase the quantity of credit offered, recorded as assets on their bank balance sheets, without increasing shareholders’ equity. Their confidence is synchronised through individual banks’ market intelligence and commonly available information concerning lending conditions. What few bankers realise is that it is expansion of their cohort lending which creates the very confidence in the lending conditions being observed.

The benefit to the bank is enhanced by expanding the ratio of total balance sheet assets to shareholders’ equity. A gross lending margin of two per cent becomes 20% for the shareholders on a balance sheet ten-times leveraged. However, this depends on margins being maintained, which, when banks compete with each other for lending business, is unlikely. Furthermore, the trend for declining rates over the decades due to the policies of the monetary authorities has led to a general increase in shareholder leverage as banking cohorts try to maintain profitability on slimming margins.

We all know that this recently reached an extreme position, with unnaturally negative interest rates imposed by central banks principally in Japan, the Eurozone, and Switzerland. In response to heavily compressed rate margins, the large commercial banks in the Eurozone were leveraging up through repos to gear up the slimmest of lending margins. The European repo market has been rolling over in excess of €9 trillion in all currencies with euros the largest component by far.

For these reasons, the most highly leveraged G-SIBs (global systemically important banks) are in the Eurozone and Japan. Table 1 below shows their balance sheet leverage from highest to lowest (the third column), and the price to book rating upon which the market values this leverage risk. Share prices were as of last weekend.

With the Eurozone’s and Japan’s G-SIBs heading the list of most highly leveraged banks, the question before us is now that interest rates are rising, how will these banks adjust their balance sheet ratios to more normal levels, which are probably in the region of eight to ten times or even less? True balance sheet gearing in all cases is likely to be far, far higher principally because of the accounting treatment of derivative obligations. These are the banks leading involvement in repos, have significant derivative positions, have netted out foreign exchange, commodity, and credit derivatives, and have only partially reflected off-balance sheet obligations through standardised credit conversion factors.

In general terms, in the new interest rate environment banks are almost certain to restrict counterparty risk by reducing their exposure to other banks for two reasons. Firstly, contracting balance sheets throughout the banking industry enhance systemic risk significantly, and a significant number of the banks in Table 1 are highly likely to fail. And secondly, as a cohort bankers are motivated to act the same way for the same reasons at the same time, even for banks without derivative exposure. The contraction and consequences of interbank obligations should not be ignored.

The problems of rising inflation, interest rates, and bond yields

After decades of minimal price inflation, central banks were caught unawares when consumer prices started to rise and continued to do so. Initially, they said it was transient. When they were laughed at, they then merely pushed back their forecasts of consumer price inflation returning to the 2% target back a year. The chart below, of the current UK’s Office for Budget Responsibility forecast is typical. It is due to be updated on 17 November, but it is a racing certainty that the OBS will still expect it to return to 2%, a little further delayed. To admit otherwise is to acknowledge a complete failure of monetary policy.

The US Congressional Budget Office is similarly unrealistically optimistic about the outlook for consumer price inflation. The illustration below is lifted from the CBO’s website.

But with consumer prices already rising in the US, UK, and Europe at a 10% clip and likely to go higher in the coming months, the interest rate disconnection is substantial and can only be bridged with interest rates doubling or even tripling from current levels. Even if they only double, business plans for all manufacturers and service providers will go out of the window. And with that catastrophe, bad debts for the banks will simply soar.

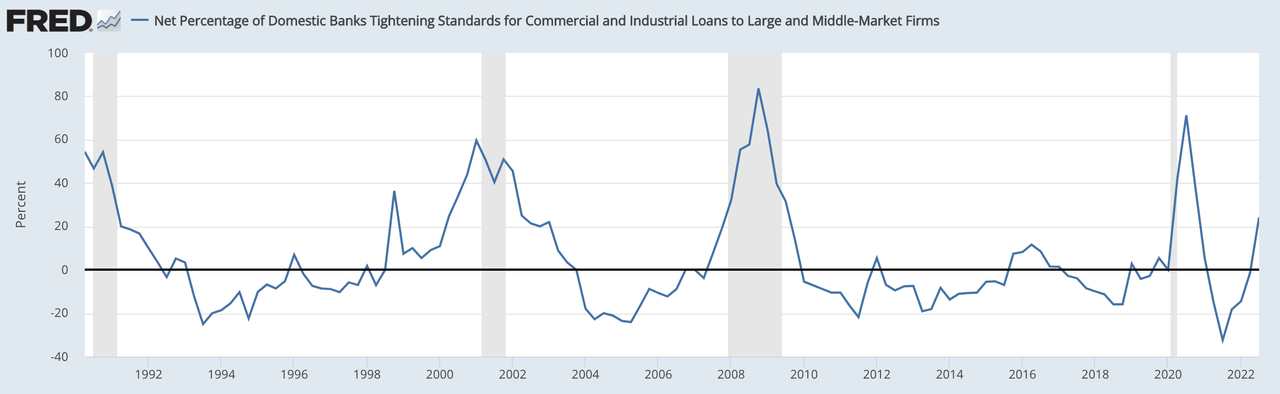

The effect on financial securities will be no less devastating. While banks generally limit their bond exposure to shorter maturities — typically bills and bonds maturing in less than a year — it is likely that banks in the Eurozone and Japan will have some exposure to longer maturities. They might have some exposure to corporate bonds and collateralised debt obligations as well, which will be at risk from rising interest rates. This is not to be ignored, and the evidence of a downturn in credit availability for corporates is already evident in loan officer surveys. Our next chart, of US banking sentiment towards corporate borrowers confirms that credit contraction for non-financial borrowers is already underway.

Clearly, bank credit is set to contract mightily, and together with higher interest rates it is likely to lead to escalating non-performing loans, insolvencies, and rising unemployment. These conditions are likely to develop before interest rates can properly reflect the debasement of the major currencies, reflected in the rise in consumer prices.

Economists commonly assume that the developing recession will restrict consumer demand, leading to an amelioration of the consumer price inflation problem. Furthermore, some supply chains are beginning to flow again, particularly with respect to computer chips. But before we can consider how a fall in demand affects prices, we should remember that the initial market effect of contracting bank credit is always to drive interest rates higher, due to accelerating credit demand arising from lost sales and accumulating inventories while banks are trying to reduce their credit obligations.

Since almost all recorded transactions that make up GDP are settled with bank credit, its contraction will reduce GDP as well. The extent to which this is the case cannot be mechanically predicted. However, since bank balance sheets are very highly leveraged and rising interest rates will force a severe credit contraction, the effect will not be trivial. If a banker is to retain control over non-performing write-offs, he must not delay in reducing his exposure.

It is for this reason that the cycle of bank credit is like a saw-tooth series of gradual increases followed by sharp declines. And the more exaggerated the increase, the more catastrophic the decline.

Mortgage loan books

It turns out that the sub-prime mortgage crisis of 2007-2009 was little more than a blip in the growth of bank lending for residential property ownership. But America with Fanny Mae and Freddy Mac is different from other jurisdictions, where banks have become highly active originators in the mortgage business.

With old memories of ruinous interest rates, borrowers have consistently gone for fixed rate mortgages in preference to floating rates. Some 80% of residential mortgages in the UK are fixed rate for between two and five years before they are reset. Until recently, to opt for fixed rates was the wrong decision. Banks have profited mightily, not by simply lending long and borrowing short, but by covering fixed rate offers with interest rate swaps allowing a healthy turn for the bank, with early termination expenses covered by penalties for the borrower.

For a bank, the beauty of this business lies in the transaction size and minimal administration. And with house prices continually rising, the collateral has been secure. But this has now changed dramatically, with mortgage rates soaring and house prices turning lower. The previous lucky minority who opted for floating rates find they face an enhanced risk of repossession of their homes. And interest rates have probably only started to increase.

From a banker’s point of view, this is turning into a very bad business. Payment defaults are certain to increase rapidly; not just for those on floating rates, but with the majority of borrowers on two- and three- fixed rate deals which are maturing at a rapid rate. A two-year fixed rate of less than two per cent faces renewal at over three times that. And no banker wants the bad publicity of foreclosing on homeowners and their families in droves, “who through no fault of their own” face eviction.

In any event, when homeowners in large numbers face eviction, the lenders have the problem more than the homeowners. It is both politically and practicably impossible for lenders to evict families in large numbers and put their homes up for sale. Apart from anything else, residential property values would collapse under the combined weight of higher borrowing costs (if mortgages are still available) and an increasing supply of liquidated housing stocks. Look no further than what happened to property prices in cities like Atlanta in 2007-2010, as the liar-loans were unwound. All that happens from the bank’s point of view is that even solvent borrowers would be pushed deeply into negative equity.

The difficulties in managing these politically toxic issues will not be the only problem facing bankers. Existing fixed-rate mortgages have been covered through credit default swaps, which are only as good as a bank’s counterparties. If, say, a British bank has a highly leveraged Eurozone bank as its counterparty, it will soon be thinking about counterparty risk in a more focused way. Where it can, it should seek to novate these obligations with more secure counterparties. But that comes with costs.

In a rising interest rate environment, this easy-come business will not be easy-go.

Wider derivative considerations

According to the Bank for International Settlements, OTC derivative market interests in the global banking system amounted to $600 trillion equivalent of notional amounts outstanding last December.[i] Being based on only seventy dealers in twelve countries reporting to their respective central banks, the statistics are not the whole picture, capturing an estimated 94% on average of their wider triannual survey covering an additional thirty nations.

To this can be added a further $40 trillion in regulated futures and options markets, in which banks play a major counterparty role. To give an idea of the sheer scale of these activities, global GDP is estimated at roughly $100 trillion.

The credit nature of OTC derivatives is poorly understood, and therefore widely ignored by commentators. Nevertheless, these are credit obligations which are only extinguished after the terms of the individual derivative contracts have been satisfied. But being purely financial, they differ from a contract which has on one side the delivery of goods or a service, and on the other a settlement invariably in bank credit. A financial transaction, be it a forward settlement, a swap, or an option exercise, involves both debt and credit obligations. And since debt is synonymous with credit because one always balances the other in both parties’ books, until a financial obligation is settled there is twice the notional credit involved.

The simplest example to take is deferred settlements, such as foreign exchange forwards. In these cases, there are two parts to the contract: there is the initial agreement, under whose terms there may or may not be a partial margin payment due immediately, and the second part is satisfaction of the entire contract by its completion.

At a notional $104 trillion — the BIS’s figure for mid-2021— foreign exchange contracts are the second largest segment of the $600 trillion OTC total. Ten per cent of that $104 trillion are options. According to the BIS’s triannual survey, only 84% of foreign exchange contracts are captured in the semi-annual statistics, so a truer figure is $124 trillion.

By maturity, they split 80% up to a year, 15% one to five years, and the rest over five years. Therefore, these are not a simple case of next day settlement, but credit obligations of material duration.

The status of options is different from forward settlements, being initial settlements for a transaction that might not eventually take place. The buyer of the option has no further credit obligation other than the initial payment of a premium to the seller of the option. But the latter party does have a continuing credit obligation which is not in his power to extinguish before it finally matures. Because all foreign exchange contracts on the BIS’s statistics represent only one side of foreign exchange contracts, the whole amount of $124 trillion are definitely credit, the majority of which, only excluding options, is duplicated by matching credit obligations for the other counterparties. Therefore, total foreign exchange derivative credit in trillions is double notional amounts outstanding less one side of notional options. This amounts to $236 trillion.

According to the BIS, the gross market value of this credit is $2.548 trillion. The BIS defines gross market value as “the sum of the absolute values of all outstanding derivatives contracts with either positive or negative replacement values evaluated at market prices prevailing on the settlement date”. In other words, to the extent to which the banking system is counterparty to these OTC derivatives, in total their balance sheets will reflect this figure, and not actual credit obligations, which are almost a hundred times greater.

It is in this context that counterparty risk must be considered. Counterparty risk is a wager that delivery of a credit obligation might not occur, and the relevant figure with respect to foreign exchange commitments alone for assessing it is $236 trillion. As an indication of the scale of these credit obligations, the BIS reports that the total of global bank credit to the non-financial sector amounted to $226.3 trillion at the date of its latest derivative statistics, similar to the scale of foreign exchange derivative credit on its own.[ii]

In round figure terms, all other OTC derivatives in the BIS statistics total about five times the recorded foreign exchange total. They include in the BIS’s notional amounts:

-

Interest rate contracts — $475.2 trillion

-

Equity-linked contracts —$7.28 trillion

-

Commodity contract — $2.22 trillion

-

Credit derivatives — $9.06 trillion

-

Credit default swaps — $8.80 trillion

-

Not otherwise classified — $337 billion.

Interest rate derivatives in rising rates

Interest rate derivatives make up the vast bulk of all OTC derivatives, with the notional contract amount of interest rate swaps totalling $397.11 trillion, and forward rate agreements adding a further $39.44 trillion. A swap is a financial derivative in which two parties agree to exchange payment streams based on a specified notional amount for a specified period. And a forward rate agreement is a contract in which the rate to be paid or received on a specific obligation is for a set period of time, beginning at some time in the future.

What concerns us here are the consequences of a rising trend of interest rates for the values of these contracts. FRAs might continue thrive if interest rate relationships along yield curves permit. But an environment of rising counterparty risk might be a hurdle too high for participating banks to overcome. A far more important consideration is the future for interest rate swaps.

Unlike the foreign exchange contracts described above, interest rate swap notional amounts are not bank credit obligations. The credit commitments of both parties are only for the income streams on a notional amount. An originator, usually a bank, funds a fixed interest stream from a floating rate, rather than the other way round.

A clue to the relationship between the gross market value of these contracts and interest rates is illustrated below, which is of interest rate swaps only originated in US dollars.

The chart confirms what we would expect: that major falls in the Fed funds rate stimulate the gross market value of interest rate swaps; and increases in the funds rate correspondingly leads to falls in their gross value. From this, we confirm that declining interest rates lead to profits for banks taking floating rates and offering fixed rates. This is the protection that customers from the gamut of pension funds to homeowners seek from higher rates. While over the long-term interest rates were declining, interest rate swaps were a profitable form of insurance product for the banks to offer. And we can now see that with sharply rising interest rates, not only will these profits vanish, but the banks are bound to exit this market entirely.

This is the heart of The Great Unwind. It will be a surprise to observers to see the BIS’s OTC derivative statistics collapse as interest rates rise further. Existing contracts with time to run can be closed down by buying out counterparties, entering offsetting swaps, selling the swap to another party, or entering an option on offsetting swaps. But these solutions to a bank withdrawing from interest rate swap obligations will be very costly, if available at all, as the entire banking cohort attempts to depart from this market.

Undoubtedly, large losses will result, threatening the entire global banking network through enhanced systemic risk.

Derivatives and the Bretton Woods III meme

That we are entering an entirely new banking and financial environment was originally put forward by a Credit Suisse analyst, Zoltan Pozsar, earlier this year. Pozsar argued that since the ending of Bretton Woods, a new financial era had dominated financial markets, which he described as Bretton Woods II. He contended that the trend for lower interest rates has now ended, that global supply chains will be repatriated, and that the era of the petrodollar is over. Instead, Bretton Woods III will be the era of commodity-based currencies.

Driving his argument was the imposition of currency sanctions against Russia. In his 3 March article, he posed the question: is the OTC commodity derivatives market the gorilla in the room?[iii] His concern was over margin calls faced by producers and others in the physical commodity business hedging physical product by carrying short positions in the futures markets. As if on cue, Trafigura, the big commodities trader, had to be refinanced within weeks of Pozsar’s note having received massive margin calls on its OTC positions.[iv]

Since Pozsar’s note, Saudi Arabia has signalled the death of the petrodollar by aligning itself with the Russia-China axis, and is scheduled to join the BRICS organisation next year. Members of the Eurasian Economic Union are planning a new trade settlement currency, said to be linked at least partly to commodities. And Moscow is setting up a new gold exchange to handle Russian and other nations’ refined gold, which will almost certainly adopt China’s 99.99% gold kilo standard.

Undoubtedly, the movement towards commodity-linked currencies, the decline of the dollar’s hegemony, and of western financial markets will have a major impact on commercial banking. One wonders how many of the banks weaned on financial activities can make the transition back to traditional lending. And if global supply chains are a thing of the past, will they be prepared to provide the credit for investment in replacement component production in the advanced economies?

As a subset of commodity derivatives, the London Bullion Markets’ forward contracts were estimated to be $781bn on 31 December 2021, of which gold forwards and swaps represented $528bn. At that date, this was the equivalent of 8,975 tonnes compared with 1,595 tonnes in the main gold contract on Comex — a ratio of 5.6 to one

The other side of the LBMA banks’ derivative positions is unallocated customer accounts, originally devised and expanded as a means of diverting demand for gold that would have otherwise driven up the price of bullion. The trend towards increasing quantities of paper bullion relative to the physical is likely to be reversed, because suppression of the gold price is now leading to accelerating demand for physical bullion.

While Keynesian hedge fund managers claim that higher interest rates are bad for the gold price, rising interest rates are bound to render derivative trading unprofitable for banks which find themselves both short of derivatives, and technically short to their unallocated bullion account holders. As quickly as the London bullion market developed in the 1980s, it is likely to diminish as interest rates increase.

Economic consequences of contracting bank credit

Today, the priority for commercial banks is to reduce their balance sheets to more normal conservative levels in their shareholders’ interests. Without considering secondary factors, the likely consequences of a severe credit contraction for the nominal GDP statistic could be to reduce it by a third or more in major jurisdictions. Realistically, central banks will have no option but to finance the losses of tax revenue and the increased welfare burdens falling on their government’s shoulders. The expansion of central bank currency and credit will replace the contraction of commercial bank credit.

Empirical evidence suggests that a population is more alert to the inflationary implications of central bank credit expanding than that of commercial bank credit. Essentially, if the public deems the currency to be stable, it will respond to higher prices when it is the result of bank credit expansion by moderating their spending. But if the public sees the currency as being unstable, they will vary their spending, and therefore their liquidity reserves accordingly.

Clearly, the political imperative will be to replace lost commercial bank credit with central bank credit. Nor can we rule out “helicopter drops” in an attempt to stimulate recovery. But having tried these measures during the covid pandemic, the public reaction to central bank debasement in a deep recession is almost certain to be less tolerant.

Central banks, which are already ceding control of interest rates to market forces will find they continue to rise as currencies’ purchasing powers continue to quicken their collapse.

Conclusion

As dealers in credit, banks face the most difficult times in living memory. Austrian economists have long understood that the business cycle is driven by a cycle of bank credit. The root of the credit cycle has been ignored by statist economists and policymakers who respond by suppressing the evidence. This has been going on with increasing intensity since the 1980s, when the Fed under Paul Volcker broke with interest rate suppression to slay the 1970s inflation dragon.

Since then, the era of pre-Bretton Woods price stability has been replaced by the fiat dollar as the reserve currency, with demand for it engineered by Triffin’s dilemma: balancing the export of dollars through budget and trade deficits with global demand for it. The expansion of derivative markets served to conceal the inflationary effects by shifting the supply of dollar credit into financial markets, away from non-financial activities. This lessened the consequences of currency expansion on the prices of goods and services, allowing the monetary authorities to suppress interest rates without apparent ill effects.

That period has now ended, and The Great Unwind of all the distortions accumulated over the last four decades has begun. No one in government and central banking circles saw it coming, and they are still in denial.

Commercial bankers are becoming acutely aware of the dangers to their business models. At the moment, they have only a growing fear of the consequences of interest rates seemingly out of control. Having been protected from free markets by central banks and their regulators, this loss of statist control is immensely worrying for them.

It is now dawning on commercial bankers that they have been left high and dry, with over-leveraged balance sheets, loan business rapidly souring, loan collateral falling in value, and a derivative merry-go-round about to implode. They must stop pandering to regulators and public opinion, and now protect their shareholders from The Great Unwind by dumping credit obligations as rapidly as possible ahead of the wider banking crowd.

From banking deregulation in the mid-eighties, it took nearly four decades to get to this point. The Great Unwind might take only as many months.

Tyler Durden

Fri, 11/04/2022 – 22:20