US Services Surveys Disappoint In April Amid Stench Of Stagflation

Despite Manufacturing surveys solid (and US factory orders surging), expectations are for the Services sector surveys today to show stagflationary signals (weak growth, surging prices).

S&P Global’s Services PMI disappointed in April (final), falling from its flash print of 51.3 to 51.0, but still up from multi-year lows below 50 in March, showing just marginal activity growth despite weak drop in sales volumes.

ISM Services PMI also disappointed in April, falling from 54.0 to 53.6 (vs 53.7 exp) amid tumbling new orders and high prices.

Source: Bloomberg

Under the hood it was not a pretty picture at all with new orders slowing dramatically, Prices Paid holding near cycle highs, and employment contracting for the second month in a row…

“Although business activity returned to growth after a small decline in March, it’s clear the pace of growth has kicked down a couple of gears since the start of the year,” said Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

The survey data are indicative of GDP growing at a modest 1% annualized rate.

“Growth may weaken further,” warns Williamson, as service providers are reporting lower inflows of new business for the first time in two years, reflecting an intensifying hit to demand from the war in the Middle East.

“The direct impact of the war has been most evident in consumer-facing services, as high prices have led to a pull-back in discretionary spending on activities such as holidays and recreation, though transport has also been curbed by high fuel prices and travel disruptions.”

However, a secondary additional driver of renewed weakness is a drop in demand for financial services, in part linked to heightened uncertainty about market outlooks but also reflecting expectations of higher inflation and interest rates, which has hit real estate and lending activity.

But it’s not just weak growth/orders, prices are surging too… broadly.

“A further increase in input cost inflation reflected not just higher fuel prices but a widening spread of goods and services rising in price, as well as higher wages, which will feed through to consumer price inflation in the coming months.”

The scale of the price rises will put pressure on the Fed to prevent higher inflation becoming entrenched, but the smell of stagflation remains in the air – central bankers’ arch-nemesis.

Shale Giant Diamondback Is Boosting Oil Output “Immediately” On Soaring Prices

With oil prices soaring to multi-year highs, it was only a matter of time: Diamondback Energy, one of the largest shale oil producers, announced it is boosting crude output in response to rising prices caused by the Iran war.

The company that operates in the Permian Basin of West Texas and New Mexico is pumping more than 520,000 barrels a day, 3% more than its original full-year guidance, and plans to sustains those levels, Chief Executive Officer Kaes Van’t Hof wrote in a letter to shareholders on Monday.

“We believe there is a legitimate supply-demand imbalance and that the associated price signal is the catalyst to begin to grow production,” he wrote. “Because of our positioning, our preparation and this price signal, we are bringing incremental barrels to the market immediately.”

Van’t Hof’s comments come just days after supermajors Exxon Mobil and Chevron told investors they wouldn’t significantly alter production plans in response to the unprecedented war-drive disruption to Persian Gulf energy supplies. Exxon’s plan to raise Permian Basin output by 12% this year pre-dated the Iran war, while Chevron is sticking to plans to keep production from the region essentially flat.

However, now that one company has broken the seal, expect a rush to hike output across the US E&P sector.

As Bloomberg notes, Diamondback isn’t the first shale specialist to see the Middle East conflict as an opportunity to bolster production. Billionaire Harold Hamm’s Continental Resources made a similar pledge last month. And who can blame them: crude futures are up by more than 50% since the war in Iran began in late February, and after all, when it comes to commodities, the age-old saying is that “the cure for high prices is high prices.”

Of course, with more output comes more capex: Diamondback is also is raising spending guidance by 4% this year to about $3.9 billion, with plans to add as many as three additional drilling rigs and run a handful of frack crews for the rest of this year, Van’t Hof wrote.

Diamondback’s CEO made waves exactly one year ago when he warned markets that the US is “at a tipping point” saying the US shale output has peaked, and slashed his capex. What a difference a year makes.

The company is also working through its backlog of ready-made wells that have already been drilled and await fracking as a way to unleash more oil more quickly.

After using a stoplight analogy in investor letters over the past year to describe his thinking on whether to accelerate or hit the brakes on output, Van’t Hof said Monday that “the light has turned green, and Diamondback is well-positioned to respond to the current macro environment.”

Ford Sales Post Sharp 14.4% Decline In April As EV & Hybrid Sales Plunge

Ford Motor Company posted a sharp sales decline in April as demand for new vehicles cooled across much of the auto industry, with the company reporting a 14.4% drop year over year to 178,667 vehicles sold, according to Autoevolution.

The weaker month pushed Ford’s year-to-date total to roughly 636,000 deliveries — still ahead of Hyundai Motor Company and Kia Corporation, but well behind Toyota Motor North America.

Autoevolution writes that the slowdown comes as automakers face softer demand after last year’s buying rush, when consumers moved quickly to purchase cars ahead of potential tariff increases. Higher gas prices tied to geopolitical tensions and persistently expensive vehicle prices have also made buyers more cautious.

While General Motors has yet to release April results, several rivals have already reported weaker numbers. Toyota’s U.S. sales fell 4.6% last month to just over 222,000 vehicles, bringing its year-to-date total to nearly 792,000. American Honda Motor Co. was nearly flat, while Hyundai and Kia also slipped slightly after a strong start to the year, though their combined sales still topped 565,000 through April.

Ford’s weakness was broad-based. EV sales dropped nearly 25%, hybrid sales plunged 32.5%, and traditional gas-powered vehicles fell 11.8%. Truck sales declined more than 14%, SUVs were down 16.6%, and the company’s bread-and-butter Ford F-Series slid nearly 14% to just over 61,000 units. Sales at Lincoln were even worse, falling more than 21%.

There were a few bright spots. The Ford Mustang climbed more than 18% in April, while the Ford Bronco rose more than 18% to around 17,000 sales. The Ford Explorer and Ford’s heavy-duty truck lineup also posted gains. On a year-to-date basis, Mustang remains Ford’s strongest performer with sales up roughly 39%, followed by the Explorer, Transit van, Ranger pickup, and Bronco. At Lincoln, the Lincoln Aviator remains one of the few bright spots, with sales up nearly 10% so far this year.

Romanian Pro-EU Government Collapses After No-Confidence Vote, Currency Tumbles To Record Low

Lawmakers toppled Romanian Prime Minister Ilie Bolojan’s pro-EU government in a no-confidence vote on Tuesday, putting at risk the country’s sovereign debt ratings, its access to EU funds and the stability of its currency. Of the valid votes cast in the parliament, 285 voted for the motion of censure and four against, exceeds the 251 signatures collected last week for the motion and above the 233 needed to pass, the official parliamentary count showed.

Bolojan has led a minority government since late April when the Social Democrats – the largest party in parliament – called for his resignation and then walked out of the four-party coalition and teamed up with the far-right opposition to file a no-confidence vote.

Although a snap election looks unlikely, financial markets are concerned that the turbulence could mean Bucharest wavers in its commitment to narrowing the European Union’s biggest budget deficit. Romania’s leu currency fell to a record low against the euro ahead of Tuesday’s vote.

The current coalition came to power 10 months ago with a view to containing the gains of the far right after a series of polarizing elections, and it had begun to reduce the deficit, narrowly avoiding a ratings downgrade from the last rung of investment grade. But the Social Democrats – without whom a pro-EU majority cannot be achieved – have repeatedly clashed with Bolojan as his austerity measures have hit their voters and patronage networks, while their popular support has bled away to the far right.

Nevertheless, opinion polls still show Bolojan is the most popular politician in the ruling coalition. Bolojan will stay on as interim premier with limited powers until a new government is approved by parliament.

“Can anyone say how Romania will function from tomorrow, do you have a plan?” Bolojan asked lawmakers before the vote. “Romanians will understand that you can govern differently, with respect for public money, and you cannot undo that.”

Romania’s next parliamentary election is not due until 2028. It has never held an early election and analysts say the likelihood of one now is small as the opposition hard-right Alliance for Uniting Romanians (AUR) leads in opinion polls.

Centrist President Nicusor Dan, who nominates the prime minister, is now expected to invite parties for negotiations and attempt to rebuild the four-party pro-EU coalition under a different member of Bolojan’s Liberals or perhaps a technocrat as prime minister. The Social Democrats (PSD) have often said they would rejoin a pro-EU coalition under a different premier.

Bolojan’s party has so far ruled out collaborating with the Social Democrats again, though some senior party members have pushed for reconciliation.

There is life after the no-confidence vote,” PSD leader Sorin Grindeanu told reporters. “We want to keep broadly this coalition.”

A Romanian Liberal member of the European Parliament, Siegfried Muresan, called the alliance between the leftists and AUR in support of the no-confidence motion “anti-European”.

“The formation of a new government will become their responsibility,” he told Reuters. However, Liberal deputy prime minister Catalin Predoiu said his party “must leave its options open”.

Romania must continue to shrink its deficit as well as implement reforms in order to tap some 10 billion euros worth of EU recovery and resilience funds before an August cutoff date. The deficit is expected to narrow to 6.2% of economic output this year from more than 9% in 2024.

Tech billionaire Elon Musk on May 4 agreed to pay $1.5 million to resolve a Securities and Exchange Commission (SEC) lawsuit alleging he violated securities laws over the delayed disclosure of his Twitter stake.

A filing dated May 4 states that Musk’s revocable trust will pay a civil penalty of $1.5 million to the commission as part of the settlement, subject to approval by the court.

According to the filing, once the proposed settlement is approved by the court, the SEC will “file a stipulated dismissal of Elon Musk in his personal capacity, which will resolve this case in its entirety.”

The SEC filed the lawsuit in January 2025, alleging that Musk violated federal securities laws by delaying disclosure of his stake in Twitter before his bid to buy the platform in 2022.

The regulator said Musk crossed the 5 percent ownership threshold in March 2022, triggering a 10-day deadline to make the holding public. Musk did not disclose his holdings until April 2022, when he had already acquired a more than 9 percent stake in Twitter, according to the filing.

The SEC said the delay had allowed Musk to buy shares at “artificially low prices” and enabled him to underpay by at least $150 million for his shares after his beneficial ownership report was due.

Musk had previously sought to have the SEC suit dismissed. In August 2025, his lawyers argued that the SEC targeted Musk over his outspoken criticism of the regulator and “government overreach.”

Separately, in March, a federal jury held Musk liable for misleading Twitter shareholders by driving down the social media platform’s stock price months before acquiring it. The decision followed a civil class action lawsuit filed by Twitter investors in October 2022.

Musk agreed to buy Twitter at $54.20 per share in April 2022 but later sought to back out of the deal, prompting the company to take legal action to enforce the deal. He ultimately completed the acquisition in October 2022 and rebranded Twitter as X.

In a verdict on March 20, jurors found Musk liable for misleading investors through two social media posts he shared in 2022. The first post said the deal was “temporarily on hold” pending verification that bots accounted for less than 5 percent of users on the social media platform.

In the second post, Musk suggested that the percentage of bots could exceed 20 percent and said the buyout of Twitter could not go forward until he received confirmation that it was less than 5 percent. Musk’s legal team has said they plan to appeal the verdict.

USAF Stratotanker Squawks 7700 Emergency Near Doha

The fight for control of the Strait of Hormuz flared up Monday and into the overnight hours, with IRGC forces reportedly striking multiple commercial vessels and a UAE oil refinery.

The one positive development: with U.S. forces on heightened alert, two U.S.-flagged merchant ships successfully transited the maritime chokepoint as Project Freedom began, marking the first visible move by the U.S. Navy to unfreeze the world’s most critical energy corridor.

U.S. Central Command, or CENTCOM, said its aerial assets in the Hormuz area were busy on Monday, with helicopters and other aircraft combating IRGC forces to ensure the safe transit of the two ships.

Flight-tracking website Flightradar24 reported early Tuesday that a U.S. Air Force Boeing KC-135 Stratotanker, a military aerial-refueling aircraft, squawked “7700” after operating in a tight pattern near the Hormuz chokepoint.

“A U.S. Air Force KC-135 is squawking 7700, flying in the direction of Doha,” Flightradar24 wrote on X.

A US Air Force KC-135 is squawking 7700 flying in the direction of Doha. https://t.co/wxldcwLX1g

Flightradar24 had no additional information on why the KC-135 crew squawked 7700. Some possible reasons include:

Mechanical failure

Engine problems

Fire or smoke

Medical emergency

Loss of pressurization

Fuel emergency

Other serious onboard problems

Separate but notable, UBS analyst Dominic Ellis provided clients with energy market commentary following the overnight Hormuz chaos:

Brent Down From Intraday Highs, Though Up 7% Relative To Monday’s Low The fragile ceasefire in the Persian Gulf seems to be on the verge of collapse after Iran responded to Project Freedom, the US effort to restart transit through the Strait of Hormuz, by launching attacks on commercial vessels and energy infrastructure in the region.

Brent is down from the intraday high over $114/b but remains close to $113/b, up almost 7% relative to Monday’s low.

The US denies Iranian claims that a US navy vessel was hit, but acknowledges damage to a South Korean cargo vessel. The UAE blamed an Iranian drone attack for a fire in the Fujairah Oil Industry Zone, concerning given the role Fujairah plays in allowing some regional oil exports to bypass the Strait of Hormuz.

Maersk said on Tuesday that one of its vessels, the US-flagged Alliance Fairfax, was successfully escorted through the Strait of Hormuz by US military assets, part of a US convoy involving at least one other US-flagged merchant vessel according to US Central Command.

It remains to be seen whether this was a one-off or evidence that the Iranian ability to disrupt flows via the Strait has been seriously degraded.

Oil could rapidly retreat below $100/b if it appears that the Iranian stranglehold on the Strait has been weakened, but even intermittent attacks on shipping would keep the geopolitical risk premium elevated and the volume of tanker traffic well below the level required for the oil S/D balance to normalise.

The next few days will be crucial – keep an eye on shipping data in the UBS Hormuz Tracker.

CENTCOM and U.S. officials have not provided any details so far on the KC-135’s emergency or what caused it.

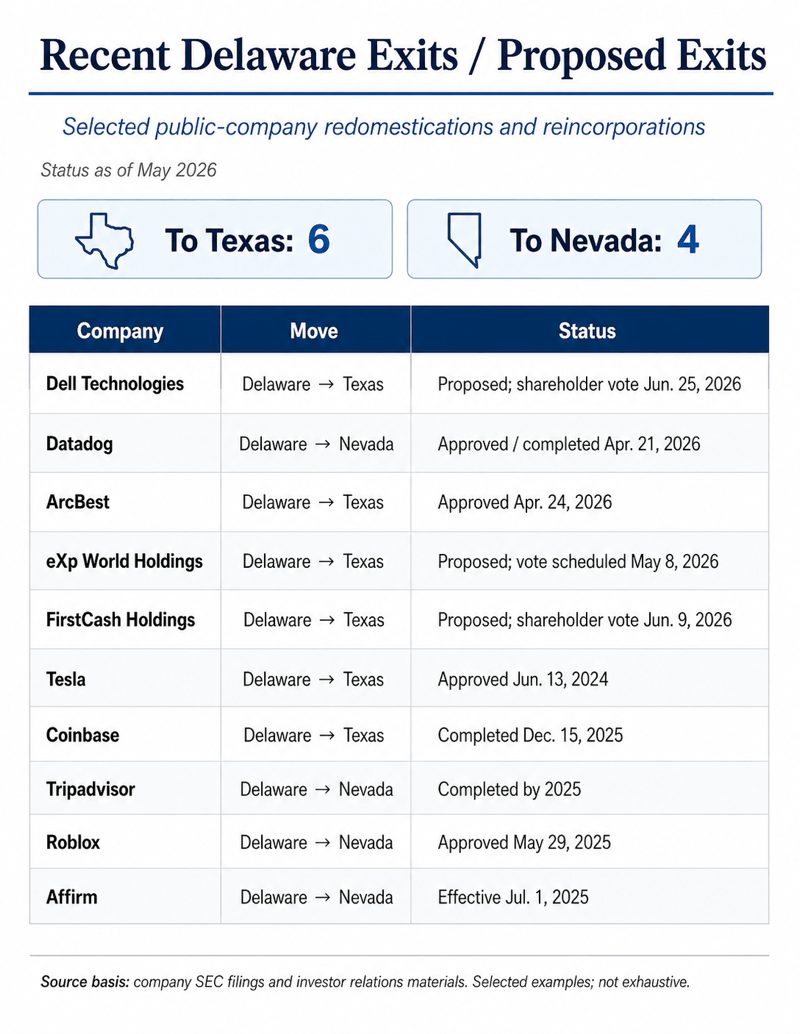

Dell Board Unanimously Backs Redomiciliation To Texas As Delaware Exodus Accelerates

Dell Technologies’ Board of Directors unanimously approved a proposal to move the company’s state of incorporation from Delaware to Texas. This adds to the growing trend of redomiciliation, with companies such as Tesla, SpaceX, Neuralink, Coinbase, Affirm, TripAdvisor, eXp World Holdings, and others moving from Delaware to business-friendly states.

Shareholders will vote on the redomiciliation at Dell’s upcoming 2026 annual meeting on June 25. “The proposed redomestication would align Dell Technologies’ state of incorporation with its roots and long-standing center of operations,” the company wrote in a press release.

Dell said the move would align its legal home with its corporate origin story: Michael Dell founded the company in Austin in 1984, and today Dell’s headquarters, CEO, and largest concentration of U.S. employees are all based in Texas.

“From my dorm room at the University of Texas in 1984 to our headquarters today in Round Rock, Texas, has given Dell what every great company needs to grow — extraordinary talent, world-class research universities, and a business environment that lets us build for the long term,” said Dell CEO Michael Dell. “Texas is where Dell has innovated, expanded, and invested for more than four decades, and bringing our legal home to Texas reflects what we’ve been building here all along.”

If shareholders approve the move, the company plans to opt into Texas provisions that would require investors to own at least 3% of shares or $1 million of stock, whichever is lower, to submit shareholder proposals.

A separate Texas rule would require shareholders to hold a 3% ownership stake to bring derivative lawsuits against management.

The exodus from Delaware all began when a left-wing Delaware judge challenged Elon Musk over his Tesla compensation package.

Delaware Court of Chancery’s January 2024 decision voiding Musk’s roughly $56 billion 2018 pay package, after a shareholder lawsuit argued Tesla’s board process was flawed and too controlled by Musk.

After that ruling, Musk publicly urged Tesla to reincorporate in Texas and asked shareholders to approve the move.

This is what followed next:

Lefty activism in courts is bad for business. FAFO.

Europe is not yet in recession, but the latest business and consumer surveys show that the risk is no longer remote.

The euro area’s flash composite PMI fell to 48.6 in April from 50.7 in March, moving below the 50 threshold that separates expansion from contraction and signalling a quarterly GDP decline of around 0.1 per cent after a 0.2 per cent gain in the first quarter, according to S&P Global Market Intelligence.

At the same time, the European Commission’s flash consumer-confidence indicator dropped to -20.6 in the euro area and -19.4 in the EU, both significantly below their long-term averages and the weakest readings since 2022, according to the European Commission.

The most worrying part of the PMI release is not just that output is contracting. It is that the contraction is arriving both in services and manufacturing and with renewed inflation pressure.

Input costs rose in April at the fastest pace since the end of 2022, while selling-price inflation reached a 37-month high, with S&P Global noting that its prices-charged index is consistent with consumer inflation running near 4 per cent.

That is the dangerous mix Europe should have learned to avoid after the energy crisis of 2022: weaker activity, higher costs, and policy complacency.

The war with Iran is the immediate shock, but it is not the cause of Europe’s vulnerability. As in 2022, an external crisis has exposed the internal weaknesses that politicians prefer to ignore: high taxes, excessive regulation, rigid labour markets, low productivity, energy dependence, and an industrial policy increasingly driven by ideology.

Europe had years to prepare for external shocks, strengthen security of supply, develop domestic resources, diversify energy sources, and reduce the tax burden on companies.

Instead, too many governments chose interventionism, subsidies, and higher public spending and are now dusting off the rationing rhetoric.

Interventionism that will backfire

Europe survived the 2022 energy crisis less because of brilliant policy and more because of temporary relief: a mild winter, emergency purchases of liquefied natural gas and weak Asian demand for some cargoes.

That window should have been used to reopen nuclear capacity, accelerate domestic resource development, secure long-term gas contracts and reduce the regulatory burden on industries. Instead, numerous governments regarded a fortunate escape as a policy triumph.

Europe remains exposed to disruptions in global LNG markets, instability in the Middle East, possible Russian supply interruptions and the rising cost of competing with Asia for energy cargoes.

A region that deliberately limits its energy options, taxes productive activity aggressively and imposes ideological constraints on investment should not be surprised when every geopolitical shock becomes an economic emergency.

Instead of allowing firms to invest, adapt, and secure alternatives, governments respond to scarcity with more controls, more intervention, and more taxation

European governments are talking about windfall profit taxes, demand control, and rationing. Instead of supporting and incentivising the companies that can secure supply and strengthen chains, they prefer to implement more interventionism that, again, will only backfire.

The April PMI data show that the impact is spreading. S&P Global says the war is hitting services hardest, with activity falling at a pace not seen since the pandemic lockdowns of early 2021, while manufacturing output is being supported partly by stock-building rather than genuine demand strength.

This matters because services were the engine that kept Europe’s weak recovery alive. If services roll over while industry remains burdened by high taxes, elevated energy costs, and regulation, the cushion disappears.

Supply chains are also deteriorating again. Supplier delivery times lengthened in April by the most since July 2022. This is the classic European policy trap: instead of allowing firms to invest, adapt, and secure alternatives, governments respond to scarcity with more controls, more intervention, and more taxation.

I find it staggering to read that some European governments want to increase taxes precisely on the companies that can deliver supply security solutions – a clear disincentive to productive improvement.

Approaching a policy test

Consumer confidence confirms the damage. The European Commission reported that confidence fell by 4.2 percentage points in the euro area in April and by 4.0 points in the EU, continuing what it calls a “free fall” since the start of the Iran war.

Households are not reacting only to headlines from the Middle East. They are reacting to a familiar reality: expensive energy, high taxes, weak real disposable income, uncertainty about employment, and governments that offer more restrictions rather than more growth.

Europe is, again, approaching a policy test. The correct response is not rationing, price controls, or new attacks on business. The correct response is deregulation, lower taxes, faster permitting, energy realism, and a serious strategy to rebuild industrial competitiveness.

The euro area does not lack talent, capital, or companies capable of solving supply challenges. It lacks governments willing to remove obstacles.

The latest PMIs and consumer-confidence numbers do not mean that Europe is already in recession. However, they show that the region is dangerously close to repeating the mistakes of 2022, which resulted in persistent dependence from Russia and weaker industrial output.

The lesson is obvious. External shocks are inevitable, but strategic weakness is a choice.

Ceasefire Over? Trump Downplays ‘Mini-War’ After US & Iranians Trade Shots, Missiles Target UAE

Summary

Trump employs interesting new term: “We’re in, I call it a mini-war.”

Fujairah says 3 injured in Iranian attack on Oil Industry Zone, UAE confirms “air defenses are now dealing with a missile threat”, we have gotten reports of explosions in Dubai, which has sent oil higher and Emini futures into the red. UAE threatens retaliation.

CENTCOM hails two US merchant ships exiting Hormuz Strait safely in “first step”. Bessent issues remarks warning the US “will fire if fired upon.”

Iran insists Hormuz is under its control & says it targeted & struck a US Navy vessel, which the Pentagon/Central Command has denied.

Trump announced Sunday US will ‘help free up’ ships stuck in Hormuz Strait through Project Freedom.Iran has in response issued a “redefined the control zone” in Strait of Hormuz.

It’s looking like the White House does not wish to given up just yet on the ceasefire, given this afternoon President Trump referenced the conflict as a “mini-war” – as opposed to a full blown war – in what seemed like an effort to downplay today’s dramatic events. Not only did missiles rain down on the UAE, sparking a fire at a key oil facility, but the US Navy said it destroyed seven Iranian military boats. Here’s what Trump said.

“They did a poll on the war with Iran, and they said only 32% of the people like it,” Trump said, without specifying who conducted the poll. “Well, I don’t like it, I don’t like war at all.”

“We’re in, I call it a mini-war,” Trump added a few moments later.

Trump has previously said he’s been advised to not call it a war. House Speaker Mike Johnson, R-La., said last week that the U.S. is currently “not at war.”

Meanwhile, more details via CENTCOM on the earlier flare-up, which separately saw the UAE engage 12 ballistic missiles, 3 cruise missiles, and 4 drones on Monday:

US Central Command (Centcom) says it has used helicopters to destroy Iranian small boats.

It follows US President Donald Trump’s suggestion that the US has struck seven Iranian small boats as it works to open the Strait of Hormuz. “Earlier today, Sea Hawk and U.S. Army AH-64 Apache helicopters were used to eliminate Iranian small boats threatening commercial shipping”, Centcom writes in a social media update.

Ceasefire Broken? Israel Awaiting US Greenlight, Trump Downplays

There remain lingering questions over whether the US-Iran ceasefire has definitively broken down with today’s Iranian attack on the UAE, as well as tit-for-tat hostilities in the Persian Gulf area. This as Israeli media says the Netanyahu government is awaiting a ‘green light’ to attack Iran again. Also the UAE is now planning a ‘severe retaliatory response’ and ‘harsh revenge’ against Tehran, per MS Now.

Yet strangely, the latest statement out of CENTCOM doesn’t touch on the question of a broken ceasefire, and President Trump himself has been silent on the matter, per the AP:

Cooper declined to say whether the exchange of hostilities between U.S. and Iranian forces in the Strait of Hormuz today amounted to an end to the ceasefire agreement. Cooper told reporters in a phone call this afternoon that Iran “initiated aggressive behavior” in the strait, according to a readout of the call provided by The Associated Press. “What we saw this morning was Iran initiating aggressive behaviors,” Cooper said. “We are simply going to respond to that.”

Trump’s response:

In a phone conversation a short while ago, President Trump stopped short of saying Iran has violated the ceasefire.

Regarding the Iranian drone and missile attacks on UAE today: “They were shot down for the most part,” Trump told me. “One got through. Not huge damage.”…

Meanwhile, amid the looming threat of bigger, renewed war:

UAE SAYS ALL SCHOOLS TO SWITCH TO REMOTE LEARNING

UAE Threatens Military Response

A fresh official statement: “The United Arab Emirates strongly condemns the new Iranian attacks that targeted civilian sites and facilities in the country, using missiles, drones, and cruise missiles, which resulted in the injury of three Indian nationals.”

“The Ministry of Foreign Affairs affirmed in its statement that these attacks constitute a serious and reckless escalation, and a blatant violation of the security and stability of the state, as well as a clear violation of the principles of international law and the United Nations Charter.” And the UAE followed with the threat that it has the right to respond militarily against ongoing “aggression and provocation”:

The UAE stressed that it will not tolerate any aggression against its security and sovereignty, and that it will respond with full force and firmness to these attacks, in a manner that fully protects its national security and the safety of its citizens and residents, in accordance with international law.

There are further confirmed reports of injuries and a fire at one or more oil facilities:

Three Indian nationals have been injured in the drone attack on Fujairah’s petroleum industrial site being blamed on Iran, the Fujairah Media Office says. The three have been taken to the hospital and their injuries have been termed “moderate”.

UAE, Bahrain, Oman Under Threat

UAE air defences are actively engaging multiple Iranian missile and drone threats today, with the Ministry of Defence confirming four cruise missiles were detected heading toward the country; three were successfully intercepted over territorial waters while the fourth fell into the sea. Explosions have been reported in the Dubai area as air defence systems responded, prompting the National Emergency Crisis and Disaster Management Authority (NCEMA) to issue public safety alerts. In Fujairah, Iranian drones struck the Petroleum Industries Zone, causing a fire at the critical oil export terminal that includes the VTTI facility – the UAE’s key Hormuz-bypass hub. The Fujairah Media Office has confirmed three Indian citizens were moderately injured in the attack, marking the first reported civilian casualties in the current wave. UK Maritime Trade Operations (UKMTO) separately reported suspicious activity and a fire aboard a cargo vessel approximately 36 nautical miles north of Dubai, with cause unknown.

The incidents unfold against a backdrop of heightened US-Iran tensions in the Strait of Hormuz, where Iran claims control and has warned it will “forcefully stop” vessels violating its regulations, while denying US reports of safe transits under “Project Freedom.” CENTCOM has rejected Iranian claims of striking a US Navy vessel. Markets reacted sharply: Brent crude pushed back toward session highs above $119, E-mini futures turned lower, equities sold off, and the US 30-year Treasury yield rose above 5.01% for the first time since July. The situation remains fluid with conflicting claims on both sides, and further official updates from UAE authorities are expected.

Injuries Reported

The Fujairah Media Office / Emirate has confirmed that 3 Indian citizens/residents were moderately injured in today’s Iranian drone attack on the Fujairah Petroleum Industries Zone (oil industry complex).

Injuries are described as moderate (no fatalities reported).

This is the first confirmed civilian injuries from the current wave of attacks.

The incident is directly linked to the VTTI oil facility strike and the fire reported minutes earlier in the same zone.

Following reports from the Following a report from the UAE National Emergency Crisis and Disaster that Emirati air defenses are responding to a missile threat, we have seen reports of explosions in Dubai, which has sent oil higher and Emini futures into the red

Bloomberg adds that the UAE has detected four missiles coming from Iran

*UAE DETECTS FOUR MISSILES COMING FROM IRAN: DEFENSE MINISTRY

Air defense systems are currently responding to a missile threat. Please remain in a safe location and follow official channels for warnings and updates. pic.twitter.com/DJFh6q8xi1

At the same time, the UK MTO Operations Center said that it has received reports multiple “Suspicious activities”

*UKMTO RECEIVES REPORT OF INCIDENT 36NM NORTH OF DUBAI

*UK NAVY: CARGO VESSEL REPORTED A FIRE IN THE ENGINE ROOM

*UK NAVY: CAUSE OF THE FIRE IS UNKNOWN AT THIS TIME

Perhaps worst of all, it appears attacks have recommenced on UAE energy infrastructure (specifically, Fujairah – the end point of the pipeline the UAE uses to bypass the Strait of Hormuz).

*UAE’S FUJAIRAH SAYS AERIAL ATTACK FROM IRAN

*FUJAIRAH: IRAN DRONE ATTACK CAUSES FIRE AT OIL INDUSTRIAL ZONE

Operations at the strategic facility have been affected.

In the fog of war, it is increasingly unclear what is real and what is fiction, but while it is certainly possible that Iran has decided to re-escalate against the UAE, which is now as much of a nemesis as Iran, there is the possibility that the UAE is creating conditions for a false flag, hoping to drag the US into what would now be a “defensive” operation and thus not needing Congressional clearance.

In any case, the market is not happy, with stocks turning red…

… and oil pushing back to session highs.

And bonds are being dumped with 30Y yield back above 5.01% for the first time since July…

Bear in mind what Goldman warned on Friday:

It feels as though there are a few lines in the sand starting to develop in markets:

120 USD in Crude (note COA roll likely dampens vol a bit today compared to earlier in the week),

4.5% and 5.0% in UST 10/30yrs,

160 in USDJPY

we would be wary of all of these and the proximity to them all adds further fuel to any future resolution risk rally/Dollar sell-off.

Patience is key as always.

Some of those signals have been hit and others are looming.

* * *

Bessent: Will Fire if Fired Upon

Coinciding with ‘Day 1’ of Trump’s Project Freedom to “guide” stranded vessels out of the heavily contested Strait of Hormuz, Treasury Secretary Scott Bessent has issued fresh remarks and warnings on Monday.

US Treasury Secretary Bessent says US is opening up the strait, we have absolute control of the strait. A quick summary of his main points via Newsquawk:

• Iranians do not have control of the strait.

• Project freedom was not done in coordination with Iran.

• If Iranians want to escalate, we are willing to do so.

• US is firing only when fired upon.

• It is a good time for US partners to step up and pressure Iran.

He further gave a very broad and fuzzy timeline, stating this ‘aberration’ will be over in ‘weeks or months’. At this point, admin officials are careful to avoid calling it a ‘war’ – given it has been 60 days since the start, and there’s the lingering question of Congressional authorization and war powers. Latest out of Hormuz:

Iranian IRGC attack hit a South Korean-linked ship in the Strait of Hormuz. Source: Yonhap

Pentagon: Two US-Flagged Ships Exit Hormuz

On Monday morning, US Central Command announced that within 12 hours after President Trump unveiled ‘Project Freedom’, a pair of US-flagged merchant ships made it out of the Strait of Hormuz. The wording of the statement makes it sound like a US naval escort made this possible – though the degree to which this was the case remains unclear. Below is the CENTCOM statement.

U.S. Navy guided-missile destroyers are currently operating in the Arabian Gulf after transiting the Strait of Hormuz in support of Project Freedom. American forces are actively assisting efforts to restore transit for commercial shipping. As a first step, 2 U.S.-flagged merchant vessels have successfully transited through the Strait of Hormuz and are safely headed on their journey.

This is being hailed as a the latest Pentagon success, however, the reality remains that Washington is celebrating a solution to a problem that did not exist before the launch of Operation Epic Fury. Or in other words, the US is seeking to open the strait which had never been closed prior to the Iran war. Meanwhile…

IRGC Says It Struck US Navy Ship, US Officials Deny

Iran is claiming to have attacked and struck a US Navy vessel, announcing that it stopped US warships from entering the Strait of Hormuz “with a firm and swift warning” and noting that “additional news will be announced later” – a statement by state Tasnim News Agency said. Soon after, Fars news agency said that two missiles hit a US navy vessel near Jask island after it ignored warnings from the IRGC to halt. Jerusalem Post also picked up on the statement, writing:

The ship reportedly turned back after being hit. The report further noted that the missiles had been launched after the US “violated security protocols for transit and navigation near Jask with the intent to pass through the Strait of Hormuz.”

However, soon after Axios stated that a “senior US official denies a US ship was hit by Iranian missiles.” CENTCOM soon after said that no US navy ships have been struck, adding that US forces are supporting Project Freedom and enforcing the naval blockade on Iranian ports. It is the latest claimed major incident soon on the heels of President Trump the night prior announcing “Project Freedom” to “guide” stranded ships out of the Strait of Hormuz. New threats:

But as we also noted, WSJ explained that Project Freedom “is a process through which countries, insurance companies and shipping organizations can coordinate moving traffic through the Strait, according to a senior U.S. official. It doesn’t currently involve U.S. Navy warships escorting vessels through the strait, the official said.” So a lot of confusion remains. UAE meanwhile chimes in with some verification of a strike on a LNG tanker:

UAE SAYS ADNOC VESSEL HIT BY TWO IRAN DONRES IN HORMUZ

UAE CONDEMNS TARGETING OF ADNOC VESSEL BY DRONES IN HORMUZ

🚨 LIVE IN THE STRAIT: The U.S. just launched “Project Freedom” to escort neutral commercial vessels through the Strait of Hormuz, but the sanctioned tanker NOOH GAS (IMO 9034690) is currently attempting transit.

Trump had also said in his Monday Truth Social statement that he is “fully aware that my Representatives are having very positive discussions with the Country of Iran, and that these discussions could lead to something very positive for all.”

Iranian Tanker Crew Swap in Pakistan

Some kind of ‘good faith’ swap is in the works, per Al Jazeera:

The crew members of an Iranian ship that was seized by the United States after it “failed to comply” with the US blockade on Iranian ports have been transferred to Pakistan for repatriation, Pakistan’s Ministry of Foreign Affairs has said.

“As a confidence-building measure by the United States of America, twenty-two crew members held aboard the seized Iranian container ship, ‘MV Touska’, have been evacuated to Pakistan,” the ministry said in a statement on Monday.

Pakistan’s foreign ministry is facilitating their return, after a couple weeks ago the US Navy seized it and characterized the capture of the merchant ship part of the spoils of war.

CNN had reported at the time that “US Central Command (CENTCOM) says the guided-missile destroyer USS Spruance warned the Touska repeatedly over a six-hour period, during which time the container ship was steaming in the Arabian Sea toward Bandar Abbas, Iran.” It was among the earliest direct actions by the US Navy after the US declared a blockade on all Iranian ports.

Iran Warns US It Will Attack

A fresh escalatory warning and rhetoric out of Iran’s military on Monday: US forces will be attacked if they enter the strait, as well as any commercial ship or oil tanker not willingly coordinating their movements with Iran ahead of time. That’s according to Ali Abdollahi, the head of the Iranian military’s unified command, and as cited in Al Jazeera:

“We warn that any foreign armed forces, especially the aggressive US army, will be attacked if they intend to approach and enter the Strait of Hormuz,” the statement said.

All of this means that what Trump touted as an act of “goodwill” has the obvious potential to become a dangerous flashpoint. Some pundits have raised the possibility of a new Gulf of Tonkin incident.

The IRGC reportedly carried out a missile strike on two ships attempting to cross the Strait of Hormuz at night.

The IRGC Navy reports that the ships turned off their transponders and were operating in the interests of the US Navy. pic.twitter.com/64Ez5bFOpR

The Iranian military is claiming it has prevented a US Navy destroyer from entering the Strait of Hormuz.

Iranian state media reports that the public relations arm of the army says: “With a firm and swift warning from the Islamic Republic Navy, the entry of American and Zionist enemy destroyers into the Strait of Hormuz was prevented.”

But it is hard to precisely confirm any of this, also as the Pentagon is mum and not expected to affirm any of Iran’s claimed ‘successes’ in stopping US naval movement in regional waters. There have also been reports of Iranian vessels firing warning shots on a US ship. And according to Axios Monday morning:

A U.S. official said the rules of engagement for U.S. forces in the region have been changed and they were authorized to strike immediate threats against ships that cross the strait, like IRGC fast boats or Iranian missile positions.

Iran’s ‘Control Zone’

Iran has “redefined the control zone” in Strait of Hormuz, stretching from south of Mount Mobarak in Iran to south of UAE’s Fujairah, and from west of Qeshm Island in Iran to Umm al-Quwain in the UAE, according to Tasnim.

A statement from Iranian State TV gives Iran’s perspective on Trump’s new Project Freedom, as it insists the strait is “under the control of the armed forces of the Islamic Republic of Iran”.

Again, all of this directly contradicts Washington’s stance, and the two sides are once again headed toward escalation amid zero sum contrary positions with apparent willingness to use force. As a reminder, Trump had on Sunday described that “For the good of Iran, the Middle East, and the United States, we have told these Countries that we will guide their Ships safely out of these restricted Waterways, so that they can freely and ably get on with their business.”

Some More Regional Developments

via Al Jazeera

Two missiles hit a US navy vessel near Jask in the Strait of Hormuz after it ignored warnings from the Revolutionary Guard to halt, state media quote the IRGC as saying.

The reported attack comes after US President Donald Trump announced a naval mission, dubbed Project Freedom, to guide stranded ships out of the Strait of Hormuz on Monday.

Iran’s Foreign Ministry says it is assessing a response from Washington to its latest 14-point proposal to end the war. Trump had called Tehran’s proposal “unacceptable”.

Israel continues to bombard Lebanon, wounding five medics, and has expanded its area of control in Gaza by announcing a so-called “Orange Line”.

Caught Off Guard: Stunned EU Leaders React To Trump’s Troop Reduction In Germany

European officials have expressed dismay, disappointment, and surprise in the wake of the weekend announcement by the Trump administration that the US will be withdrawing some 5,000 troops from Germany over the coming months.

“There has been talk about withdrawing US troops from Europe for a long time. But of course, the timing of this announcement comes as a surprise,” EU foreign policy chief Kaja Kallas expressed on the sidelines of the European Political Community meeting in Yerevan, Armenia on Monday.

She then tried to find a silver lining, saying this must motivate Europe to strengthen its own role inside NATO. “I think it shows that we have to really strengthen the European pillar in NATO and we really have to do more,” she said.

But she also reasoned, “American troops are not in Europe only for protecting European interests, but also American interests.” Kallas also said: “I don’t see into the head of President Trump, so he has to explain it himself.”

Similarly, NATO Secretary-General Mark Rutte reacted by saying European leaders have “gotten the message” from Trump following the announcement.

Rutte, who is also in Armenia, acknowledged “disappointment from the US side” and said, “European leaders have gotten the message. They heard the message loud and clear.” He followed with: “Europeans are stepping up, a bigger role for Europe and a stronger NATO.”

Norwegian Prime Minister Jonas Gahr Støre when asked about the troop reduction, described “I wouldn’t exaggerate that because I think we are expecting that Europe is taking more charge of its own security.”

“I do not see those figures as dramatic, but I think they should be handled in a harmonious way inside the framework of NATO,” he told reporters in Yerevan.

NATO spokesperson Allison Hart said officials at the 32-member alliance currently “are working with the US to understand the details of their decision on force posture in Germany.”

Over several years, and stretching back decades, the US has maintained the most number of troops on the European continent in Germany – currently estimated at over 36,000 active duty personnel. So the 5,000 – while significant – is still somewhat of a symbolic move and number.

The large US presence hearkens back to the post WWII division of Germany and post-war order, and is also a legacy of the Cold War. Ironically at this very moment European leaders have hyped a ‘new Cold War’ with Russia, as the Ukraine war continues raging.

“The officials characterized the move as a signal of President Trump’s discontent with the level of assistance that European allies have offered in the U.S.-Iran war,” CBS wrote on the reduction decision.

The significance of the planned move also lies in the fact that America’s German bases serve as headquarters of US European Command and Africa Command – with the historic Ramstein Air Base being the key hub.

The announcement via US reporting comes just a day after Trump again lambasted German Chancellor Friedrich Merz:

“The Chancellor of Germany should spend more time on ending the war with Russia/Ukraine (Where he has been totally ineffective!), and fixing his broken Country, especially Immigration and Energy, and less time on interfering with those that are getting rid of the Iran Nuclear threat, thereby making the World, including Germany, a safer place!” Trump wrote on Truth Social.

Merz had in a rare moment torched US foreign policy and the Trump administration’s Iran war gambit in Monday remarks given at a local event in Germany. Included in that very head-on critique of Operation Epic Fury came in the following: “An entire nation is being humiliated by the Iranian leadership, especially by these so-called Revolutionary Guards. And so I hope that this ends as quickly as possible.”

Merz had also claimed, “If I had known that it would continue like this for five or six weeks and get progressively worse, I would have told him even more emphatically.”