Potential Nationwide US Rail Strike May Spark Chaos Ahead Of Christmas

Remember in September when the country was on the brink of a nationwide rail strike that almost froze critical transportation networks?

A similar scenario could be nearing as workers of major freight rail companies have yet to settle on a new contract.

Twelve rail unions representing 115,000 workers must ratify a new contract to prevent an economically devastating strike by early December. If one union disagrees, all other unions must honor the labor action.

So far, seven unions have voted to ratify the tentative agreement. Three other unions representing 60,000 workers have voted it down. And two of the largest unions, representing 60,000 locomotive engineers and train conductors, are voting on the deal.

CNBC’s Lori Ann LaRocco said if the Transportation Division of the International Association of Sheet Metal, Air, Rail, and Transportation Workers (SMART-TD) and the Brotherhood of Locomotive Engineers and Trainmen (BLET), the two largest unions, “do not ratify the deal — they could start striking December 9th — following a mandatory cooling off period.”

“As of right now, even if these two unions vote to ratify the deal, we’re still looking at a strike — why? — because three unions have already voted not to ratify the deal,” LaRocco said.

Here’s more from LaRocco on the possibility of rail strikes next month. She said the first key date for investors to watch is a vote on Monday.

American consumers and manufacturers could be greatly impacted if there was a strike, and it would behoove members of Congress to step in if there’s an impending sign of labor action to prevent a new crisis.

As mortgage rates have risen this year, the demand for home purchases has fallen. That has spelled trouble for the home construction business. Homebuilder confidence dropped for the 10th straight month in October. The decline in builder sentiment reflects what economist Ian Shepherdson describes as “housing … in free fall. So far, most of the hit is in sales volumes, but prices are now falling too, and they have a long way to go.” The University of Michigan’s index of buying conditions for homes has fallen to the lowest level since 1982.

Naturally, this has been a sizable drag on the sale of newly constructed homes. According to the Census Bureau, new single-family houses sold in the US in September were down by 17 percent, year over year. They were also down by 10.9 percent from the previous month. Overall, sales of new homes are down 42 percent from the peak in August of 2020.

Nor does it look like construction of multifamily housing is likely to make up for the decline in single-family. Although it might stand to reason that a decline in demand for purchase housing could lead to more building of rental housing, that doesn’t appear to be the case. According to Housing Wire, the “historic multifamily housing construction boom is already fading.” This is partly due to the fact that rising interest rates are not limited to mortgages for home buyers, and “those same interest rates pushing would-be homebuyers to the sidelines are also hurting [muiltifamily] developers.”

It’s getting more expensive to borrow money up and down the food chain in housing, and that’s slowing down new construction of both for-purchase and for-purchase housing.

For anyone concerned about the availability and affordability of housing, this is bad news. The US is currently in the midst of a housing shortage in the sense that builders aren’t building enough to keep up with population growth. And now, it appears that the short-lived boom in construction that launched in recent years will soon be over.

New housing construction has always been sensitive to business cycles. Over the past 60 years, it’s not hard to find annual swings in construction growth ranging from negative twenty percent to positive twenty percent.

Source: US Census Bureau.

Moreover, the negative swing on housing construction in the years surrounding the 2008 financial crises were especially severe. Construction began to head downward in 2006, with a drop of 12 percent. This was followed by three years of even bigger declines, culminating in a 38-percent drop in 2009.

New housing construction did not return to the post-1990 average again until 2020.

In other words, the end of the housing bubble in 2009 had an enormous impact on the industry and led to more than a decade of below-average home production. In spite of enormous amounts of new money creation, stimulus, and ultra-low interest rates, the home construction industry did not bounce back. As noted in National Public Radio earlier this year, the slow pace of new housing construction did not start with the current economic cycle but dates to an earlier easy-money-induced bubble:

[T]he roots of the problem go back much further — to the housing bubble collapse in 2008.

“What I call a bloodbath happened,” says [builder Emerson] Claus. It was the worst housing market crash since the Great Depression. Many homebuilders went out of business. Claus was building houses in Florida when the bottom fell out.

“A lot of my tradespeople found other work, went and got retrained for new jobs in law enforcement, all sorts of jobs,” says Claus. “So the workforce was somewhat decimated.”

A few years later, as Americans started buying more homes again, building stayed below normal. And that slump in building continued for more than a decade. Meanwhile, the largest generation, the millennials, started to settle down and buy houses.

This trend was then only made worse by the shipping and logistical bottlenecks brought on by the government-imposed covid lockdowns. These have meant a shortage of lumber, appliances, electrical equipment, and cabinetry. The National Association of Home Builders concluded in June “shortages of materials are now more widespread than at any time since NAHB began tracking the issue in the 1990s.”

The Role of Monetary “Stimulus”

Monetary inflation has fueled shortages in both labor and supplies as stimulus programs have driven demand by both businesses and consumers to new heights. Yet, since this demand is based on the appearance of newly printed money, and not on rising real wealth or productivity, we’re seeing more demand for a stagnating supply of goods and services.

The result has been less building even as population has continued to grow. The result, of course, has been a higher cost of living—just as we would expect from an inflationary boom.

The data on home starts and population backs up the anecdotal evidence. For example, if we look at annual housing starts totals the trend has been downward since 1960. Beginning in 1983, every new trough in the housing construction downcycle has been lower than the one before it.

Source: US Census Bureau.

This has only been slightly mitigated by slowing population growth, and we have seen an upward trend in the number of new US residents per new housing start, even as the size of the US household has fallen. In other words, the number of new residents per new housing start has grown over time. From the 1960s through the 1980s, the average number of new Americans per new housing start was approximately 1.6. Since 1990, on the other hand, the average has been 2.2. Since 2008, the average has been 2.5. So, there are progressively fewer and fewer new housing starts per person.

Source: US Census Bureau.

After new housing construction began to collapse in 2006, the number of new residents per new housing unit surged to nearly 5, a new high.

On the other hand, it is true that in 2020 and 2021, new housing construction reached the highest levels seen since 2007. Moreover, the gap between new residents and new housing was eliminated. This was thanks to a sizable decline in new population growth created by covid-era border closures and a fall in fertility rates. Thus, the number of new residents per housing unit then collapsed below 1 for the first time in decades.

But, this trend is unlikely to continue since “after a construction boom in the second half of 2020 and 2021, the home building sector is contracting.” Population growth is also returning to more normal rates. The gap between new population and new units will already be growing again in 2023. It does not look like boom of the last 18 months will be enough to reverse the worsening situation in housing production.

It’s also important to note the effects of repeated boom-bust cycles on total housing production. One might be tempted to assume that new rounds of monetary stimulus—say, the quantitative easing of the past decade—would easily reverse a collapse in housing construction and will bring new highs in housing production. That is not what has happened, however. Rather, relentless monetary stimulus since 2008 has not been sufficient to address the effects of malinvestment and regulatory costs over the past 20 years. Over the past six months, new housing starts have flatlined compared to 2021, and we may even see housing starts end the year down in 2022. The result is a continuation of an ongoing decline in housing production. Not even the runaway money printing of the past two years has been enough to bring home construction back to what was more normal before the housing bubble and resulting financial crisis.

COP27 Climate Virtue-Signaling Boondoggle Ends In Failure, Leaves Out Fossil Fuel Pledge

If you said one week ago that the COP27 virtue signaling boondoggle in Egypt’s Sharm el-Sheikh would be an epic failure, pat yourself on the back: it was. As Argus media reports, a draft of the COP 27 UN climate summit cover decision released today reiterates many of the Glasgow Climate Pact goals agreed at Cop 26 last year, and, as expected, does not mention a broader fossil fuel phase down.

The document repeats a request made at COP26 for all countries to revisit and strengthen their 2030 nationally determined contributions (NDCs) — countries’ climate pledges — to align with the UN’s 2015 Paris Agreement, and to update their long term strategies. The Paris Agreement aims to limit global warming to well below 2°C above pre-industrial levels, and ideally to 1.5°C. Only problem: there is no mandate on how to do it, especially since even Europe is backsliding on its anti-fossil fuel promises and has restarted coal plants (not to mention record coal output in China).

Only around 25 countries updated their NDCs before COP27, and a few more did so during the summit, but it is still not enough to meet the 1.5°C target. The document says the emission gap between pledges and what is needed to hit the Paris Agreement target represent “a grave concern”.

The document reiterates the “urgency of action to keep 1.5°C in reach”, but during informal consultations at the start of this week parties were unable to reach agreement on inclusion of stronger language to limit global warming to 1.5°C. This would be more ambitious than the Paris Agreement.

It’s been 27 COPs and we still have no declaration to phase out fossil fuels.

Fossil fuel lobbying is a powerful force but the science is clear. We cannot keep expanding oil & gas!

And while the G20 summit of major economies, which also concluded this week, strengthened commitments, saying the group “resolves to pursue efforts to limit the temperature increase to 1.5°C”, which could be viewed as an encouraging sign, the COP27 text still makes no reference or pledge to a fossil fuel phase down, language pushed by India at the start of the summit and that has gained support, although the EU stressed it should not distract from efforts on phasing down coal power generation, as agreed at Cop 26.

But language on coal and fossil fuel subsidies does appear in this version of the cover agreement, echoing the Glasgow text. The new draft stresses the “importance of enhancing the share of renewable energy in the energy mix”, and “encourages the continued efforts to accelerate measures towards the phase down of unabated coal power and rationalise inefficient fossil fuel subsidies”. The language on fossil fuel subsidies differs from last year’s text, focusing on rationalising rather than just “accelerating efforts towards” their phase-out.

The energy and cost of living crises have put efforts to phase out fossil fuel subsidies at risk. Subsidies are likely to increase this year, partly because of higher energy prices arising from Russia’s war in Ukraine. The commitment in the draft Cop 27 text still does not set a deadline for a phase-out of inefficient subsidies. So far only G7 countries have one, for 2025.

Pan-African Parliament president Fortune Charumbira said today that the issue of fossil fuels cannot come “before other major commitments are delivered”. Fossil fuels will remain a reality in terms of use until “we have financed the alternatives”, he said.

On loss and damage, the document does not mention the creation of a new facility, but it welcomes the inclusion on the Cop 27 agenda of discussions on a new funding arrangement. Loss and damage refers to the destructive effects of global warming, and is a priority for many vulnerable countries experiencing extreme climate-related events such as storms and rising sea levels.

The draft decision “expresses deep concern towards the significant financial costs associated with the loss and damage for developing countries” and “reiterates the urgency of scaling up action and support”. Many countries and observers said Cop will be a failure if parties fail to agree on the creation of a loss and damage fund this year, and progress on the issue could be critical to move forward with other negotiations.

Perhaps the only good thing to come out of the COP27 is that while everyone’s favorite attention who… er, seeking woman, Greta Tunberg, boycotted it because it did not place her on a pedestal and accused the summit of being an exercise in Greenwashing (for once she actually is right), the summit which took place in Egypt unveiled to the world the new and improved Greta 2.0: meet Sophia Kianni, 20-years-old, who is an advisor to the UN Secretary General on Climate.

“Young people are definitely shaping outcomes here at COP27,” Kianni told BBC even as Swedish teenager Greta Thunberg skipped the Sharm el-Sheikh meeting, calling it a forum for “greenwashing“.

San Francisco has launched a new pilot program offering guaranteed monthly income to a number of low-income transgender residents of the city, Mayor London Breed announced on Wednesday.

Known as the Guaranteed Income for Transgender People (G.I.F.T.) program, the new plan will provide “economically marginalized transgender people with unrestricted, monthly guaranteed income as a way to combat poverty our most impacted community members face,” according to its official website.

Specifically, the website states that the monthly guaranteed income of $1,200 a month for up to 18 months will be granted to 55 low-income transgender residents.

Those residents will receive the funds via a pre-loaded debit Visa card which will be reloaded every month.

The program is being run by the Transgender District, which was founded by three black transgender women, and Lyon-Martin Community Health Services, in partnership with municipal city departments in the City and County of San Francisco.

Applications Close in December

Applications for the program are open from Nov. 15 to Dec. 15, 2022, and applicants must be age 18 years or over and identify as transgender, nonbinary, gender non-conforming, or intersex.

Individuals who apply for the program must also not be receiving more than $600 a month in income, must be living in the City and County of San Francisco, and must be willing to complete a survey every three months aimed at helping to improve the program.

The program will prioritize enrollment of “transgender, non-binary, gender non-conforming, and intersex people who are also Black, indigenous, or people of color (BIPOC), experiencing homelessness, living with disabilities and chronic illnesses, youth and elders, monolingual Spanish-speakers, and those who are legally vulnerable such as TGI people who are undocumented, engaging in survival sex trades, or are formerly incarcerated,” the website states.

The program will run for 18 months from January 2023 to June 2024 and participants will not have to report to officials exactly what they are spending the money on.

Participants will also receive gender-transition treatment, mental health care, and an array of other benefits, according to multiple reports.

Inflation Hits American Families Hard

The program comes as inflation has soared across the country, impacting American households, which are facing increasingly costly energy bills and having to fork out more for everything from food to accommodation.

A report from The Heritage Foundation published on Nov. 10 found that working families have lost $6,100 in real annual income under “Bidenflation.”

“Our Guaranteed Income Programs allow us to help our residents when they need it most as part of our City’s economic recovery and our commitment to creating a more just city for all,” Breed, a Democrat, said in a statement.

“We know that our trans communities experience much higher rates of poverty and discrimination, so this program will target support to lift individuals in this community up.”

This is not the first time that San Francisco has launched programs aimed at low-income residents.

Last year, the city rolled out a Guaranteed Income Pilot Program for artistsaimed at “dismantling structural racism and oppression” in “the everyday lives of artists of color, their families, neighborhoods, and communities.”

In 2020, Breed announced the launch of a pilot program providing a basic income to black and pacific islander women during pregnancy.

According to a 2015 U.S. survey (pdf) of 27,715 transgender people across the District of Columbia, American Samoa, Guam, Puerto Rico, and U.S. military bases overseas, 29 percent of respondents reported living in poverty.

Zelensky Backtracks After Urging NATO Action For Polish Border Blast

Ukrainian President Volodymyr Zelensky is doing some belated backtracking after his prior false and highly dangerous claims that Russia launched a missile attack against NATO member Poland, killing two Polish citizens Tuesday.

As of Thursday Zelensky says he’s not sure about what happened. “I don’t know 100 percent — I think the world also doesn’t 100 percent know what happened,” he said. “We can’t say specifically that this was the air defense of Ukraine.”

This after everyone from NATO Secretary Jens Stoltenberg to Poland’s president to US President Joe Biden assessed it was most likely a Ukrainian anti-air missile that errantly struck the Polish border town of Przewodow. A flurry of accusations from Western officials and media ensued, with fears dominating Tuesday into Wednesday of the potential to spark WWIII.

“Zelensky previously insisted that the rocket was not Ukrainian and wanted evidence if Ukraine’s air defense was responsible,” The Hill writes. “But he softened his position at Bloomberg’s New Economy Forum in Singapore on Thursday, saying that Ukrainian military leaders told him that the crater from the blast site suggested that a Ukrainian anti-air rocket could not be solely responsible.”

According to more via The Hill:

Polish President Andrzej Duda said on Wednesday that it was “highly probable” that the strike resulted from Ukrainian air defense and appeared to be an accident.

Zelensky said in the interview that he was “sure” that it was a Russian missile but also knew that Ukraine launched weapons to defend against the Russian attack.

Recall that Tuesday night, almost immediately following the explosion on the Polish border and without evidence, Zelensky had demanded “action” from the West over the supposed brazen aggression against a NATO member.

“Hitting NATO territory with missiles… This is a Russian missile attack on collective security! This is a really significant escalation. Action is needed,” Zelensky said his Tuesday night video address.

In referencing “collective security” of NATO he was attempting to convince Brussels that military intervention was needed against Russia in defense of Poland. But now it seems with world opinion diverging from Ukraine’s blanket assertions for once, Zelensky is slowly backing off his initial claims.

If we needed more proof that Kiev is trying to embroil US and NATO in direct, possibly nuclear war, with Russia it’s these reckless, false claims by @ZelenskyyUa. In fact no Russian missiles hit Poland. As even NATO governments admit, these were Ukrainian https://t.co/GpZv1qtMTWhttps://t.co/GYpVVxhh1E

CNN subsequently cited Ukrainian military sources who are belatedly admitting the likelihood that it was their own missile. “The Ukrainian military told the US and allies that it attempted to intercept a Russian missile in that timeframe and near the location of the Poland missile strike, a US official told CNN,” the report says. “It’s not clear that this air defense missile is the same missile that struck Poland, but this information has informed the ongoing US assessment of the strike.”

The Regime Is Shifting, And Here’s What That Means

Authored by Simon White, Bloomberg macro-strategist,

The macro landscape is changing. Inflation will remain in an elevated and unstable regime, but the first stage of the crisis is drawing to a close. That means the dollar in a downward trend, bonds in an upward trend, stocks underperforming bonds, and growth outperforming value.

Regime shifts can be almost imperceptible in real time, but in retrospect they mark fundamental turning points. Inflation today is going through one of these shifts, analogous to the 1970s. In that decade, inflation could be understood as a play in three acts, a drama that is likely to be repeated in this cycle.

In the first act, inflation makes new highs and the Fed tightens aggressively.

The second is when inflation begins to recede, allowing the central bank to pull back from tightening.

The final act is when we see inflation return with a vengeance, eliciting a Volcker-esque monetary response and a deep recession in order to fully snuff it out.

So what’s brought the curtain down on the first act? Three important indicators have made a decisive turn:

The market is now ahead of the Fed’s rate projections (the Dots)

The real yield curve is emphatically flattening

My Advanced Global Financial Tightness Indicator (AGFTI) is rising

All through this cycle, the market has been anticipating a lower peak rate than desired by FOMC members. That changed in the last couple of months, signaling that Fed hawkishness was peaking as the market was amplifying — not inhibiting — the Fed’s intended policy.

The real yield curve had steepened relentlessly as shorter-term real rates kept falling while the Fed rate lagged inflation. But the trend definitively turned in July, pointing to a peak in the dollar. The greenback’s rise has been one of the defining aspects of the macro environment over the last 18 months, and its turn lower signifies an easing of pressure on, most significantly, EM equities and commodities.

Global monetary conditions are likely at their tightest.

It’s not just the Fed that has been raising rates; central banks globally have been doing likewise. However, even though many began to raise rates after the Fed, any sign the US may not need to tighten much further will be enough to let other central banks take their foot off the monetary brake too.

What does the second act in the Inflation Play mean for asset prices? As just mentioned, the flattening in the real yield curve indicates the dollar has likely peaked for now. This opens up room for greater support in the euro, yen and sterling as most of the weakening in these currencies can be attributed to dollar strength.

Treasuries should see more upside. As well as a more economy-friendly Fed, higher US short-term yields have stifled foreign demand for Treasuries, while both positioning and seasonal factors are very favorable for them.

Stocks will face less formidable headwinds, but until excess liquidity begins to definitively turn up and the looming threat of a recession persists they will continue to be stuck in a bear market, facing the risk of sharp sell-offs. That being said, recent price action points to a bias for upward surprises in the short-to-medium term.

What is more certain is that stocks will continue to underperform bonds.

The stock-bond ratio remains only marginally below its fair value, and tends to overshoot to the downside, reaching its nadir in the depths of the recession.

Within stocks, though, there should now be a window where growth starts outperforming value again. Growth stocks, especially tech, have lagged and have been the worst performing sectors. A change of regime and the rising threat of a recession likely means potential for tech to outperform. As the chart below shows, tech tends to underperform before a recession, and outperform afterward.

A warning: the second act is only an intermission before inflation and higher rates return for the finale. Positions should be rented, not owned.

Nomura: Good (Data) Is Bad (For Assets) – The Difference Between R* & R**

It certainly seems like people are taking off some of their US Equities “risk rentals” which have rallied so violently over the past week since the CPI downside surprise…

…and thematically, have even begun to lay back into their Shorts in all the trash that exploded 20% over the week…

…hence, US Equities Long Term Momentum factor +3.1% and Low Risk factor +3.0% again yday, respectively, as they feel the recent move has “overshot” particularly on the “expensive” / “unprofitable” stuff

And this morning, St.Louis Fed’s Jim Bullard poured even more cold water on the pause/pivot prayers as he hinted at even higher rates for longer.

As Nomura’s Charlie McElligott notes the resilience of the US economic data sits at the core of this renewed confidence in taking some shots again on “FCI tightening” trades, as we see the Bloomberg US Economic Surprise index reaching highs last seen in mid-May ’22, as data continues to beat expectations on the margin – Labor, Retail / Wholesale and Surveys / Biz Cycle Indicators bearing the concentration of the gains (while Housing, Industrials and Personal / Household sectors continue to drag)…

Translation: ”Good (data) is Bad (for assets)”…

As McElligott lays out, this all keeps coming-back to this recent NY Fed research paper concept of R* (neutral rate for the real economy) simply sitting in a totally different universe from R** (neutral rate for financial stability)…

It now seems abundantly clear that “markets” cannot handle much more rate hiking after a decade + of duration- and leverage- binging, as evidenced by the list of “market breakages” experienced over the past 12 months…

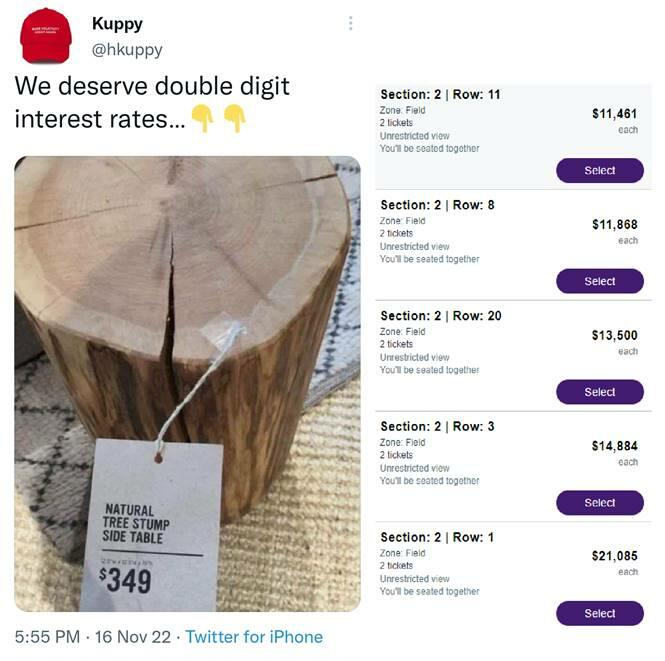

…but in the meantime, the real US economy (admittedly outside of Housing and structurally-shrinking Manufacturing sector) keeps banging along, where in peak (cringe) anecdotal fashion, restaurant ressies are “no offer,” luxury malls like Short Hills are packed with lines out of some of the most high-end retailers doors, airports are foaming at the mouth and airline tickets are running 2-3x’s ‘sanity levels,’ there is no locate on new Range Rovers in New Jersey until 2024….and all while New Yorkers are apparently lifting $21k Taylor Swift tickets for next Summer…

And this is why “High for Longer” continues to persist (Fed “Terminal” projections back above 5.00% this morning – but our house view is that it’s gonna have to push through 5.50-5.75, while GS took their Fed projection up yday as well)…

…it’s the same thing: the Inflation is going to soften down to 4-5% on pure base-effect math – but it’s not going to head back to 2% target if you don’t see actual job losses mount…bc right now, Labor and Wage gains are just too strong.

And because of that economic ‘strength’, equities still feel fragile:

The “sign of possible regime change” I highlighted in the last note – where US Equities Index Option Skew has steepened for 5 out of the past 6 days while Stocks violently rallied, standing in stark contrast to the perpetual flattening in Skew to 0%ile over the course of 2022 YTD – I believe has been a function of folks actually needing to hedge again, because they were starting to actually put on some exposure again after this violent “force-in” rally that very few people actually wanted to happen

And also as previously mentioned in recent weeks, my spidey senses too have been tingling with this persistent VIX Upside being sought for 6 consecutive weeks in size, most of it “wingy” / “crash” stuff

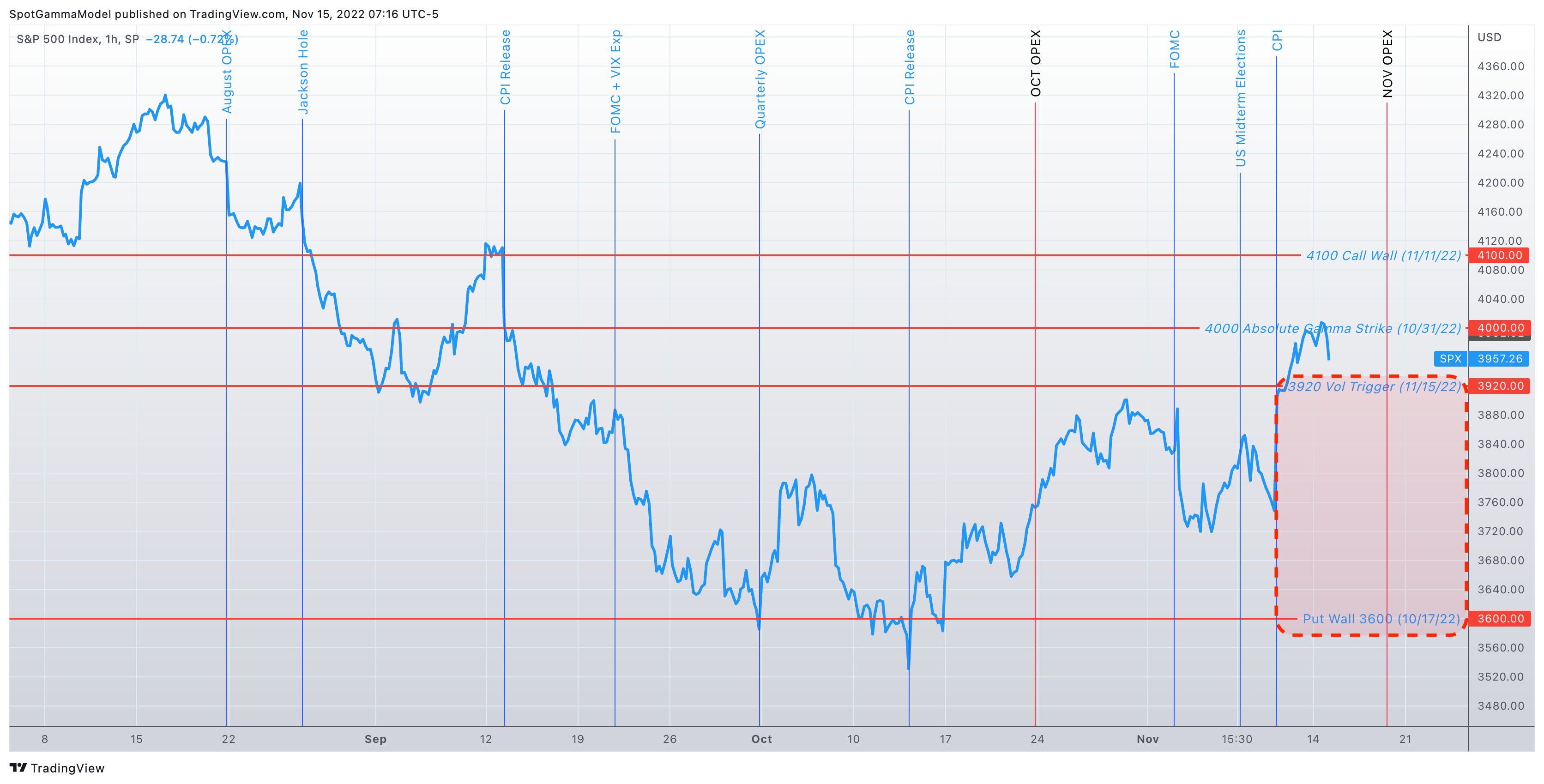

The S&P has tumbled back down to its 100DMA this morning…

…as we see Spot selloff this morning, we now see SPX back at “Gamma Flip” level as we speak (3918), while both QQQ and IWM have pushed back into “Short Gamma” territory

And as SpotGamma notes, that ‘negative gamma’-inspired volatility could be triggered with Fridays OPEX, and we have been therefore recommending adding some puts (here & here). The concern here is that we do not see much support of any kind from 3900 down to 3600 (chart here, description here).

I had a conversation with my good friend Tom Bodrovics from Palisades Gold Radio earlier this week. Tom is a private investor from western Canada with a background in oil and gas. In 2014 he identified the top of the housing cycle and sold his home to invest in the junior resource sector. He gained a libertarian and contrarian perspective in 2013 when he attended an entrepreneurship course in Europe and has been studying markets of all types ever since. He operates a successful business servicing the oil and gas sector in Alberta and is the host of one of my favorite podcasts, Palisades Gold Radio.

We took an hour this week to discuss all things FTX, crypto, the Fed, the economy, monetary policy, some of my recent blog posts and, of course, gold. Our entire conversation was recorded as a podcast and is available to listen to, for free, at the end of this post.

The first topic Tom broached with me was the ongoing FTX saga. He asked about what I thought about Sam Bankman-Fried blowing up his firm and I told Tom that I couldn’t believe how quickly it happened and how swift the fall was.

“A week ago this guy was the savior. He was just generally being praised,” I told Tom.

“Then, what we found out is that it was just another straight up ponzi scheme fraud, which is just incredible,” I said, stunned by how quickly it came crumbling down.

“I’m often saying to people ‘Everything is fine until one day you wake up and it isn’t.’ That’s my stance on equities right now. I think we have a 400 bps pipe bomb making its way through he economy right now and we’ll wake up limit down. That’s what happened with Bankman-Fried. One day he was the man and the next day we woke up and there was a tremendous shift in psychology.”

I summed it up: “We woke up one day and the guy that was supposed to be the end-all be-all turned out to be nothing more than a run-of-the-mill fraudster. It was just a bunch of kids playing with billions in customer deposits like they were playing World of Warcraft. I don’t know if the reality has sunk in for them as to how big of a deal this is, but I’m sure it will. You had a group of kids just…fucking around with customer deposits. It’s not fraud on the blockchain, its not decentralized fraud…it’s just run of the mill fraud.”

Tom then directed the conversation away from FTX and SBF and onto the broader topic of bitcoin. He asked me why I owned and continue to buy a very small position in bitcoin, which Tom referred to as a “religion”.

I responded: “I’m pretty religious about gold actually. I think gold is going to be the answer come hell or high water for this looming global economic mess. Bitcoin I’m interested in probably moreso as just a contrarian – watching a huge blowup like this cast a negative light on crypto in general is something that piques my interest.”

“I think 95% of coins out there will have no use case,” I told Tom. “To the extent that Bitcoin remains the grandaddy of them and the underlying, I’m more interested in listening to the bull case when Forbes is doing a cover story on how crypto is the biggest fraud of our generation.”

“Really, it’s just pure speculation and I’m fine with taking 100% loss,” I said about my Bitcoin position. “I’m still very skeptical that it’ll become a global reserve currency. Now it’s going to be a time for far more regulation [thanks to FTX].”

From there, we moved the conversation on to where more blowups in the crypto space may take place. I mentioned to Tom that Michael Saylor, Binance and Tether are all in my crosshairs.

“Either way I think we’re going to see more blowups,” I said. “How do you let Tether go forward now without producing a full and complete audit of all of their assets at this point? This is a company with $60 billion in stablecoins that’s deeply intertwined into the crypto universe.”

From there, we moved on to the topic of the Fed, monetary policy and interest rates. Tom asked about my contention that I still think equities will move lower, as I wrote about just days ago in a piece called Keep Your Nerve.

I told Tom: “I think that if the Fed even came out tomorrow and cut 100 bps…I think even in a case where the Fed came out and cut rates tomorrow that there would still be a looming blowup. The speed with which we’ve raised rates so far is breakneck and stunning. The reason the market hasn’t reacted yet is there’s a lag.”

“That’s all playing out now and will continue to play out regardless of what the Fed does in December,” I added.

Tom asked about the idea of a soft landing, to which I replied: “Everyone is acting as though Powell has already achieved a soft landing. CPI came in at 7.7% – not exactly where we want to be. If I had told you 2 years ago that’s what CPI would be at you would have had a f*cking heart attack. And now we’re going to celebrate it as a win?”

“The Fed is going to do what it always does: too much, too late. And it’s not going to stop the selling when it starts,” I added. “Imagine in 2018 when we were trying to do unlimited QE to get from 1.7% to 2%…imagine if I told you rates were at 4% and the market is celebrating. You would think that I’m smoking some shit. I mean, even when I’m high I make points that make more sense than that.”

Get 50% off: If you enjoy this article, I would love to have you as a subscriber and can offer you 50% off for life: Get 50% off forever

Finally, Tom asked me about whether or not the Fed was ‘winning the war’ on inflation – and where I see inflation going next year.

I told Tom: “There’s so many unknowns. A lot depends on Russia and Ukraine, China has basically been conditioning their economy with this Covid Zero policy to shut down and open up whenever the government says. Xi Jinping is flipping the economy on and off like a light switch. Then you have Russia, and then OPEC – and who knows what color their mood ring is on any given day – and then the BRIC nations trying to start their own global economy. So who knows where CPI will come in?”

“It’s completely opaque, other than what we can do just tracking spot prices. That can be helpful.”

Finally we talked about the idea of a Santa Claus Rally, which I wrote about days ago in an article called The Santa Pause Rally.

“The point of the article is basically ‘look, we’ve spent the last 3 or 4 years trying to make investing, which is a risky business, dumbed down for retail investors’,” I explained.

“If there’s one piece of nefarious patronizing lingo that I hear every year it’s the idea of a ‘Santa Claus Rally’ – just another bullshit term made up by the financial media to further the Keynesian monetary policy experiment as if it is some virtuous undertaking that is never going to end poorly. It’s terminology that tells people it’s OK and normal for markets to only go up.”

I added: “That kind of stuff does a disservice to amateur investors.”

“The same monetary policy experiment that the media is trying to legitimize and encourage is the same policy that got us into the current crisis that we’re in,” I said.

I continued: “Rather than celebrating it and passing it off as some raging success, I think people need to recalibrate themselves and understand monetary policy is why we’re watching Sam Bankman-Fried blow up and incinerate people’s cash. The Fed sent a behavioral incentive to markets that speculation was fine for way too long – a signal to markets that there was no risk when, in fact, risk was everywhere.”

QTR’s Disclaimer:I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. These positions can change immediately as soon as I publish this, with or without notice. You are on your own. Do not make decisions based on my blog. I exist on the fringe. The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

UK’S Hunt Hikes Taxes, Slashes Spending To Tackle “Cost-Of-Living Crisis”

One month after stepping into his new role as UK Chancellor for the Exchequer, Jeremy Hunthas raised taxes on the UK’s top earners and tightened spending in an effort he says was needed to repair the country’s public finances amid a predicted 1.4% contraction in 2023.

Hunt is also lowering the threshold for paying the top 45% rate from £150,000 ($176,000) to £125,140 ($150,000). Those who earn at least £150,000 per year will pay an additional £1,200 as well in order to help pensioners and low-income households, Bloomberg reports.

There will also be a significant increase in the energy and windfall taxes.

Hunt has been tasked with stabilizing the country’s finances following ‘one of the most chaotic periods in British history,’ when his predecessor, Kwasi Kwarteng (and short-lived PM Liz Truss) pushed for unfunded tax cuts – resulting in a run on the pound.

Since taking office last month, he’s been warning the British public — and the Tory backbenchers who’d cheered on the tax cutting plan — that he would have to take “difficult decisions” to win back the confidence of investors. -Bloomberg

“Today we deliver a plan to tackle the cost-of-living crisis and rebuild our economy,” Hunt said in a Tuesday statement to the House of Commons. “We also protect the vulnerable because to be British is to be compassionate and this is a compassionate Conservative government.”

Ironically, Cable is lower on Hunt’s Austere budget…

Hunt’s plan should provide an annual cost saving of £55 billion in 2027-28 (around 2.5% of GDP), according to Goldman.

Here are five key takeaways from Bloomberg:

The outlook is grim: the country is already in recession and households face the biggest hit to disposable incomes ever as the government seeks £55 billion of fiscal consolidation

Tories will hate this, because the government is taxing the rich to help the poor. That’s the opposite of the Liz Truss plan they were cheering a couple of months ago

The poorest will get some protection, with pensions and benefits to rise in line with inflation. The energy aid is also extended, albeit with a higher cap on prices

Energy firms are in the firing line with a new windfall tax on low-carbon generators and an extension to the raid on oil and gas companies

The pound and bonds were lower, but market reaction was generally muted when compared to the fallout from the Kwasi Kwarteng budget

What won’t change? Thresholds for paying into the national insurance system, and the inheritance tax – at least until 2028.

State pensions and benefits were raised by 10.1%, in line with inflation, while the minimum wage was boosted 9.7% to £10.42. Rent hikes for social housing have been capped at 7%.

A Polish politician has blamed Ukraine for causing a “provocation” by falsely claiming its own missile that struck Przewodow had been fired by Russia.

Immediately after news broke of the incident, President Zelensky called on NATO to take action against Russia, accusing Moscow of firing the rocket.

However, within hours it became clear that the accident, which killed two people, was actually caused by a Ukrainian air defense missile.

That didn’t stop British Prime Minister Rishi Sunak, NATO and other prominent officials blaming Russia for the incident anyway, despite it clearly being Kiev’s fault.

Now the former chairman of the city council of Lublin, the seat of the region where Przewodow is located, is calling for Poland to rethink its approach to the war in light of the incident.

Having up until now been a staunch supporter of Ukraine, Jaroslaw Pakula said the missile accident showed Warsaw needed to send a blunt message to Kiev rather than telling its own citizens “fairy tales.”

“Of course, this is a Ukrainian rocket. Of course, this is a provocation on the part of the Ukrainian authorities,” Pakula posted on his Facebook page.

“The rocket could not be fired 100km in the opposite direction by mistake,” he added, asserting that the incident was an attempt to scare the EU into sending more money to Ukraine.

Demanding that Warsaw should “no longer put up with this behavior” from Ukraine, Pakula remarked, “I urge you to rethink Poland’s position [regarding] this war in the event that the red line is crossed again!”

Despite all evidence indicating the missile was fired by Ukraine, Zelensky has doubled down, denying that Kiev was involved and asking for his country to be at the forefront of an investigation.

However, after President Joe Biden swiftly said the evidence for Russia’s involvement was minimal, CNN reported that Ukrainian military officials told their American and western allies that they were responsible for the blast.

Kiev had “attempted to intercept a Russian missile” at the same location and in the same time france as when the missile strike at the Polish village of Przewowdow occurred, according to the report.

The Associated Press also had to issue a retraction, noting that it had “erroneously” reported that “Russian missiles” had killed two people in Poland, and that this was based on a claim by one single anonymous senior US intelligence official.

Thank you AP, for correcting a story that nearly launched WW3. Now maybe you can also name the “senior American intelligence official who spoke on condition of anonymity” and who may have had ulterior motives in bringing the world to the edge of nuclear war pic.twitter.com/xtruXlv6U3

{kind=link}