Authored by Peter Tchir via Academy Securities,

According to Google, the MAG 7 are MSFT (+8% on the year), GOOG/GOOGL (both -2%), AMZN (+15%), AAPL (-6%), META (+36%), NVDA (+60%) and TSLA (-20%). Looks more like the “Magnificent 7” is more like the “Magnificent 4” with 3 of the alleged members down on the year and underperforming the S&P 500 and Nasdaq 100.

Purists will probably tell me I’ve used the term “moniker” incorrectly. So be it. I think continuing to refer to some mythical group as the “Magnificent 7” will do your portfolio far more harm than good. It isn’t helpful (any longer) and is likely detrimental as that narrative is hiding other, more important trends. None of that changes whether or not I’ve used moniker correctly, so I’m going to run with it.

In this weekend’s report A Global Game of Chicken we highlighted some of the challenges money managers face when stocks are such a large percentage of benchmark indices. We also highlight that the much maligned (I think we can use that word) Chinese stock market has outperformed the U.S. in February (we focused on FXI vs QQQ).

Far more (and in some ways, as we will demonstrate, far less) is going on in these markets.

I must admit, I did not know much about NVDL or NVDQ until last week. NVDL is a 2x leveraged ETF tracking one stock – NVDA. It looks like it was launched back in December 2022 and has accumulated almost $1 billion in AUM. Shares outstanding have increased significantly, with a big bump in August 2023 and another series of inflows starting at the end of January of this year. I will give credit for the inverse ETF’s ticker symbol (who doesn’t like to see a Q at the end of a ticker – it is commonly done once a company has gone bankrupt), but it isn’t surprising that ETF has only $12 million.

I bring these two ETFs up, as I’m not really sure why the world needs ETFs tied to a single stock, but also because CHATGPT helped me identify some other interesting symbols.

Remember FNGU? Back when FANG was the “moniker” of choice for a group of stocks allegedly driving everything. That ETF still has a market cap of over $4 billion, but shares outstanding are down around 80% from its peak in late 2022.

CHATGPT also found UWTSL, apparently a 3x leveraged TESLA ETN, but I couldn’t find any evidence of that – not sure whether it exists, did exist, or just sounded cool to CHATGPT (btw, it was the first ticker it presented in response to my single stock etfs and it didn’t come up with either of the NVDA ones). Not bashing AI,, but can’t say I’m horribly impressed versus other searches I might have conducted on my own. In theory that’s a story for another day, but given AI is quite literally the biggest driver in today’s market, maybe it shouldn’t be the story for another day?

When I was interviewing a guest on Bloomberg TV last Friday as guest host, I asked questions about whether the current state of data is good enough for all the current investments around AI. He effectively told me not to worry about it, as there is AI that is creating data. I tried not to visibly cringe.

While on the one hand, it makes a lot of sense for AI to be out their collecting, scrubbing and transforming data into usable forms, I couldn’t help but think of CDO^2 and the Great Financial Crisis.

Of all the issues that wound up hurting markets, the CDO^2 (or CDO squared) product deserves a lot of the blame (the mortgage backed securities at the heart of the crisis and referenced in ABX, of big short fame) were CDO squared. My view, which I think is absolutely correct, is that potentially small mistakes in the original model to create tranches, were amplified to extreme levels, when the model was used to tranche the tranches.

But again, I digress (or maybe, I’m actually not digressing given the importance of AI, its potential, couple with concerns of how ready for “prime time” it is, versus today’s spending).

So, here we are on this seemingly random walk, and we really haven’t reached any conclusions, except that:

-

The Magnificent 7, like FANG is no longer a construction that helps you think about markets.

-

That signs of froth, like the appeal of ETFs that leverage a single stock are garnering flows and volumes, are worth thinking about.

What started today’s piece, which I haven’t gotten to were a series of charts and thoughts I’ve been seeing on media (social and otherwise).

While I cannot today, recreate all these charts, I will copy one from a friend who is extremely good, and try and point you in the right direction on others.

-

Equity put call ratios. I never fully understand this one, but basically when the ratio is low, it means there is a lot more call buying than put buying, which often signals complacency. We saw references to that last week. What I’ve started to see is indications that the ratio is “normalizing” but stocks are not rebounding – which in itself is supposedly a warning sign. As a bear, I will be poking around into this a little bit more.

-

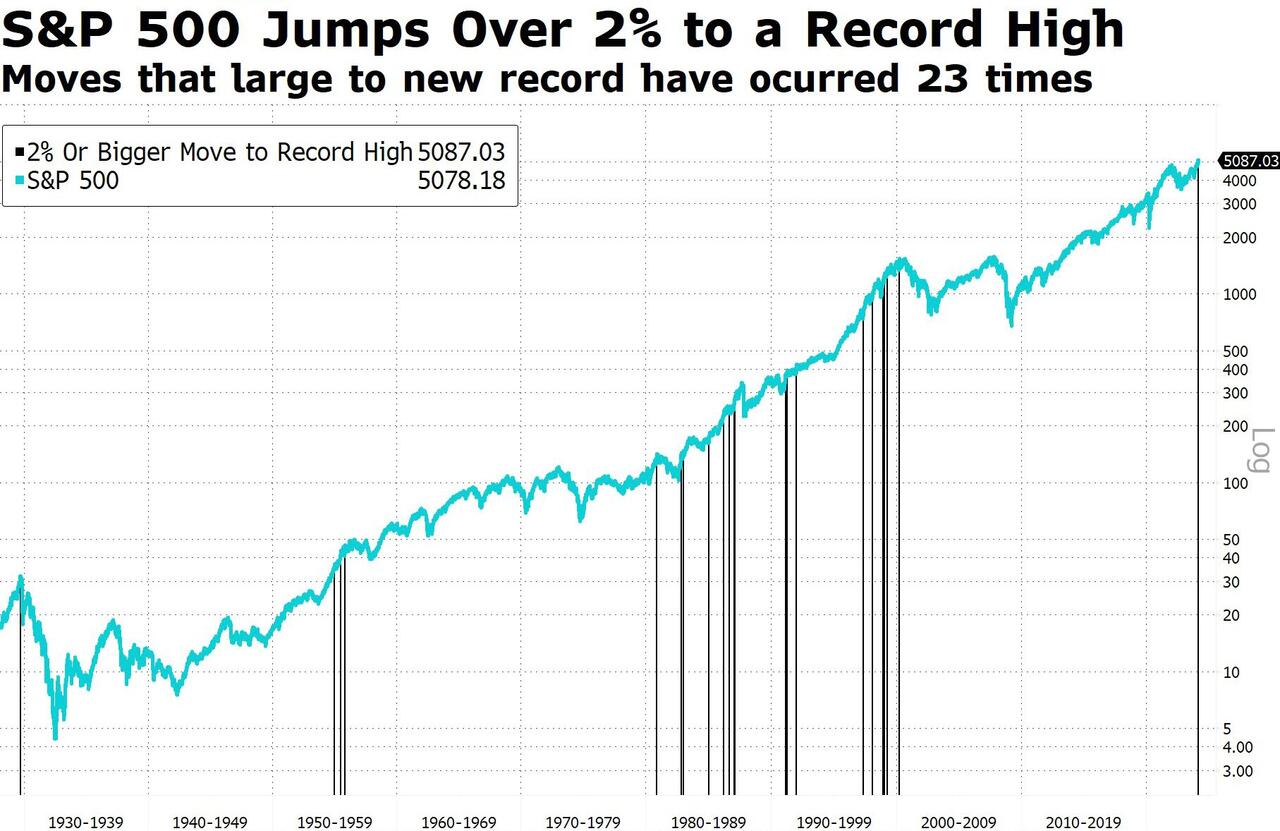

Abigail Doolittle on Bloomberg, had a story that “outsized moves into a record” have preceded corrections and tops in the past. The timing certainly varies, but it was an interesting observation and goes back in time. It included periods in 1929, 1980 and 1987, where the timing was reasonably close to large drops. It makes some senses to me, as has the feel of “the last gasp” as bears get pushed in and the last reluctant buyers, decide they cannot wait for a dip. If you have a Bloomberg terminal, you can find the chart with the command G #BTV 6877

. The time horizon on the chart is a bit too big for my tastes, but seems worth at least thinking about.

-

The market performance is very narrow and concentrated. I have used this chart created by a friend, Michael Green of Simplify Asset Management, who is also known as @profplum99 on twitter (or X). Highly recommended follow.

The argument, with some historical evidence is that as the market returns become more “narrow” – i.e. lower correlations, we are susceptible to pullbacks.

-

Margin debt. Seeing indications that this has accelerated again. In general, it increases over time as the size of the market and the economy and the money investors have grows (all good reasons). It is always unclear if the debt is used to fund short or long positions (typically viewed as being skewed towards leveraged longs). It can grow for extended periods without “triggering” anything. On the other hand, sharp rises in margin borrowing has preceded many severe pullbacks.

-

I do watch TQQQ and SQQQ closely. Triple leveraged ETFs linked to the Nasdaq 100. We have seen big outflows out TQQQ (3x long) since late October. That is “positive” as a contrarian, but the shares outstanding are still higher than prior peaks. The timing of retail, which always seems to surprise professionals, is actually pretty decent. Peak shares outstanding, were at the start of 2023, so these investors caught most of the rally. (If you are keeping score at home, TQQQ is still $21 billion). SQQQ (3x inverse), had a recent low of shares outstanding back at the end of October. Inflows have picked up again recently (in theory, good for stocks as a contrarian indicator, but the investors in this vehicle have timed things well enough that I’m not sure it is contrarian). SQQQ is only $3 billion. If past trends occur, I think we see ongoing selling of TQQQ to be replaced with purchases of SQQQ. That in itself would create bearish flows, but my real concern is the $60 billion that TQQQ represents (3x leveraged) and the impact that has at the close on positive and negative days, though clearly I’m thinking more about forced selling than I am about the forced buying into the close. Though that certainly helped markets last Thursday.

I would not put on a single trade based on any of these charts or ideas. Collectively, though, they are more interesting. As a bear, they become very interesting.

Bottom Line

I remain bearish on U.S. stocks for many reasons, and nothing I’ve written today, changes that view. For me, it only reinforces that view.

I do like Chinese stocks for a trade, and don’t understand why people want to fight the CCP?

I didn’t even get to mention treasury auctions as a reason to be bearish, but think that too will play a role as we debt and deficit chatter will fill the airways, especially once people get bored of hearing the old (and currently inaccurate) Magnificent 7 narrative.

Tyler Durden

Wed, 02/28/2024 – 08:50