Authored by Ryan McMaken via The Mises Institute,

When Congresswoman Marjorie Taylor Greene called (again) for “national divorce” this week, a common retort among her detractors on Twitter was to claim that so-called red states are heavily dependent on so-called blue states to pay for pretty much everything.

Reporter Molly Knight claimed, for example, that “Red states get their money for roads and cops and schools from blue states. You cut off that gravy train and you e [sic] got a third world country.”

Others claimed that red states would be “entirely broke” without blue states. America’s social democrats have apparently fully gone over to pushing the narrative that the “red states” are poor and backward while the “blue states” are productive and economically sophisticated.

The implication here is that red states would never survive any sort of separation from the blue states because the red states would then miss out on the presumably large amounts of free money.

Unfortunately for these critics, the data doesn’t really back them up. While it is certainly true that a handful of red states receive much more in federal spending than their residents pay in federal taxes, this is not at all the situation across most red states. This is especially not the case in states with states with larger metropolitan areas such as Florida and Texas.

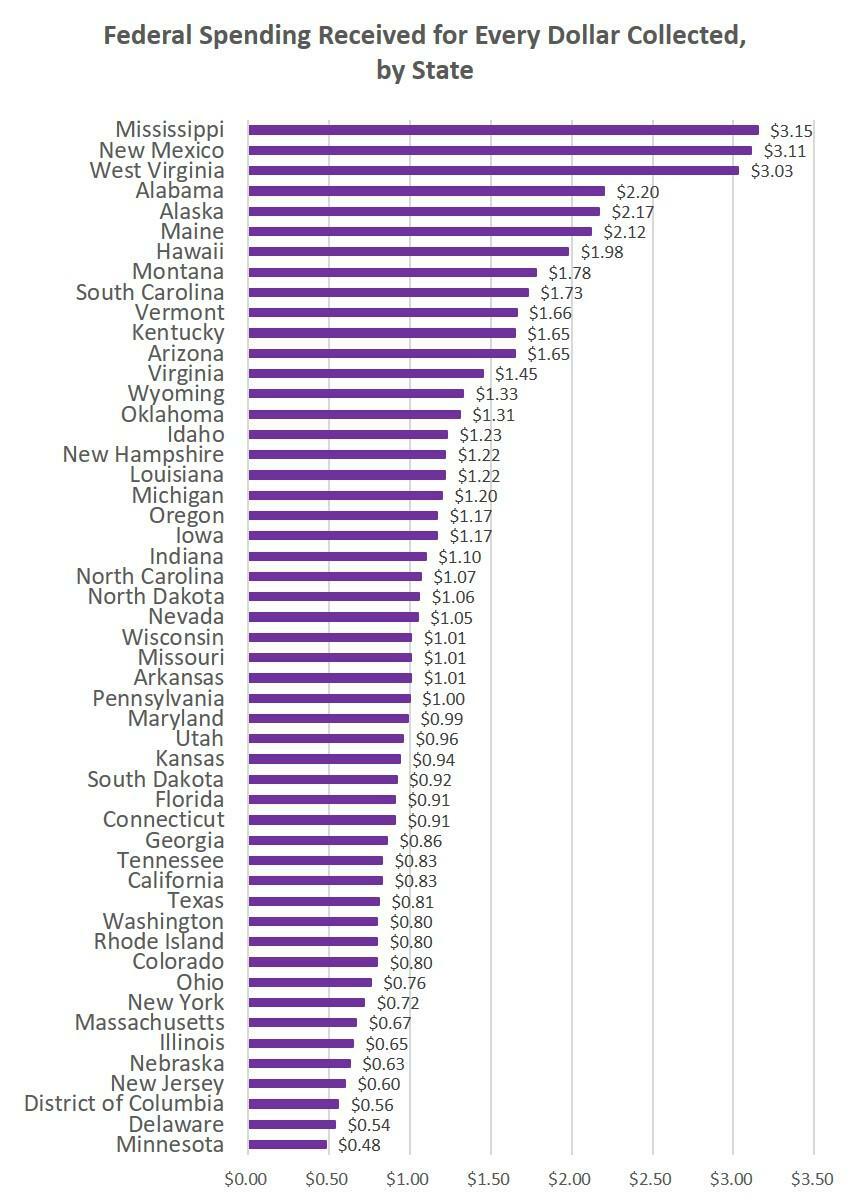

The real story is more complicated, and to see the details, we can look at state-by-state comparisons in terms of “return on taxes paid.” This is a measure of how much each state receives in federal spending for every dollar extracted in federal taxes. States with a “return” above one dollar are getting back more than their residents paid in federal taxes. Residents in a state with a “return” below a dollar pay more than they receive.

To do this analysis, we start with the tax collections from each state, as reported by the Internal Revenue service. Then, we look at federal spending in each state. There are some smaller categories of spending that are difficult to track, but we can capture the overwhelming majority of federal spending in each state by looking at several key categories:

Once we add it all up we can see the “return on taxes paid” in graph form below:

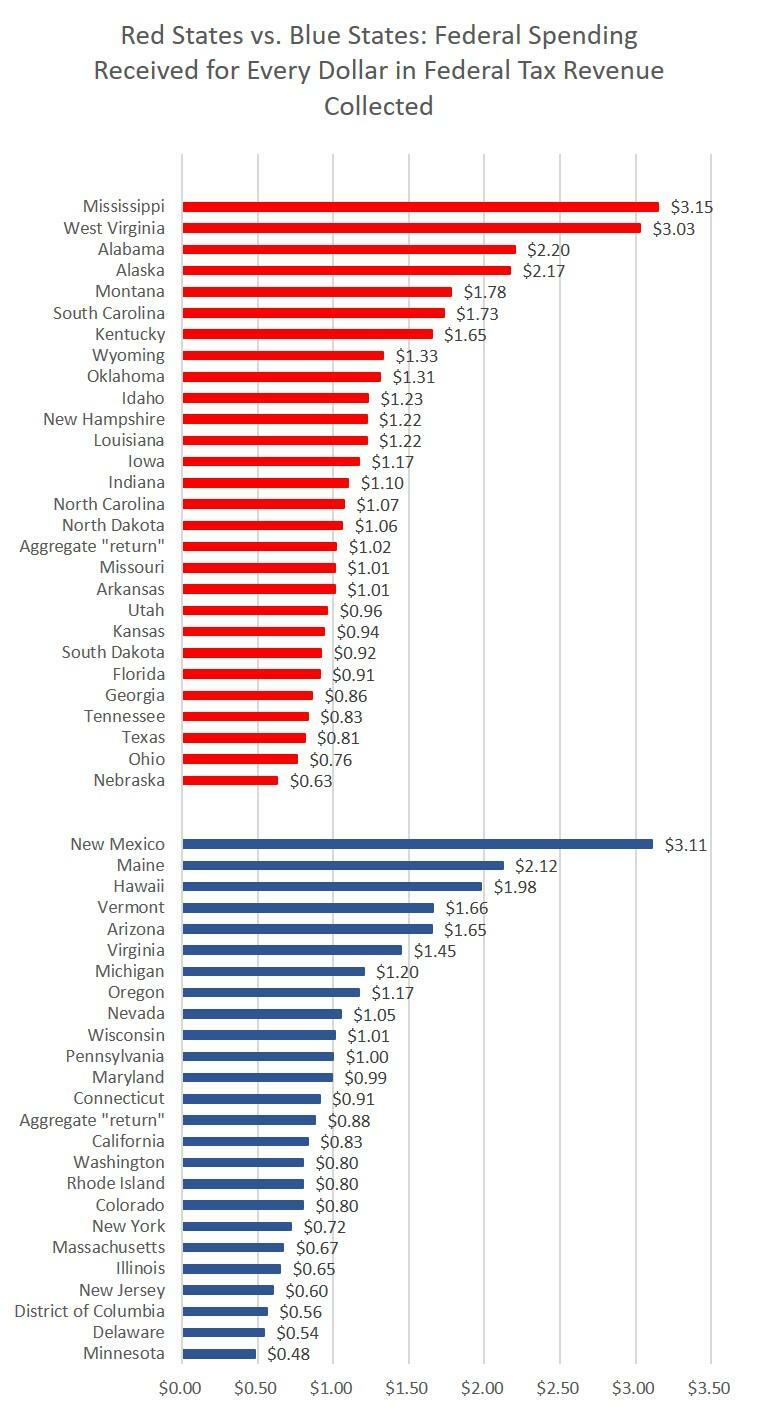

By this analysis, the federal spending in Minnesota only amounted to 48 cents for every tax dollar extracted from the state. On the other hand, Mississippi received more than three dollars for every tax dollar paid by residents. Contrary to the idea that most red states are like Mississippi, however, we find that most states—both red and blue—are much closer to the middle on this. The states that are within a few cents of receiving a dollar for a dollar—i.e., “breaking even”—include the Dakotas, North Carolina, Nevada, Wisconsin, Missouri, Utah, Maryland, Kansas, and Florida. Meanwhile, California and Texas are approximately equal with each other, receiving about 80 cents in federal spending for every dollar paid by residents in taxes.

My findings here are similar to the study that was repeatedly sent to Rep. Greene by many of her scoffing critics. Specifically, Green was instructed to read this Moneygeek article which purportedly “proves” that the red states depend heavily on blue-state largesse to survive. Yet, with both our analysis here, and with the Moneygeek article, we will find that the characterization of red states as an economic drain on the country requires quite a bit of hyperbole.2

After “National Divorce”: A Red State vs. Blue State Breakdown

Just how badly would red states fare if they were to break off from the blue states? Well, only a minority of these states would be “in the red” and get back significantly more than they pay in. 15 out of 27 red states are either net-tax-paying states or within a few cents of “breaking even.” In other words, with the exception of states like Mississippi and West Virginia and Alabama, most of these states could realistically expect to be self-funding in case of a national break-up. Moreover, viewed as a single bloc, the red states’ overall “return” on taxes paid is only $1.02. Were these states to become an independent region of their own, it would hardly be impossible to manage with current tax resources. In fact, if a “Red States of America” wanted to ensure available revenues exceeded current tax liabilities, the bloc could simply exclude the less productive states. If Mississippi and West Virginia don’t bring much to the table, there’s no immutable law of nature requiring the “Red States of America” to include them.

Some of the current net tax receiver states could also easily change their fortunes by simply splitting off the less productive areas such as southwest Alabama, western Mississippi, and eastern Kentucky. The blue states would surely be happy enough to have those areas as dependencies

How Much GDP Do the Red States Produce?

One other tactic used to portray the red states as a bunch of impoverished welfare queens is to claim that the overwhelming majority of the US’s GDP is produced in the blue states. Again, this is a sizable exaggeration. Breaking out the blue and red states as we did above, we find that the blue states naturally produce more GDP because they have more people. Specifically, the blue states contain about 54 percent of the US population and they produce about 59 percent of GDP. In contrast, the red states contain about 46 percent of the US population and produce 40 percent of GDP. In this scenario, a red state bloc would still have a GDP over $8 trillion and would have the world’s third largest economy behind China and the “Blue States of America.” It would have an economy larger than Germany, Japan, and India.

Looking at GDP per capita, we find the red state bloc would remain on a par with western Europe and Canada. If divided up, the blue states today would come in around $69,000 per capita. The red states would come in at about $55,000. Taken as two groups, this would place the blue states on a par with Denmark (at approximately $68,000), and the red states a little above Finland (at approximately $54,000).

Why Some States Are Net Taxpayers, and Some Aren’t

Why do we have these large disparities among states? Federal tax revenues are driven heavily by the number of high-earning and full-time workers in each state. States with large numbers of retirees and elderly will thus produce less tax revenue while receiving more in federal spending. States with large low-income populations (relative to overall size) will receive a proportionally higher amount of federal spending. Thus, it’s not surprising that Mississippi, with its large low-income population in the Delta region, is a net recipient of federal spending. Similarly, the population in West Virginia is relatively low-income and elderly. Neither of these states have notably large metropolitan areas to balance out these lower-income households. On the other hand, Florida, Texas, Utah, and Ohio have the productive metropolitan areas necessary to balance out populations of pensioners and the unemployed.

It should also be noted that when I say “metropolitan area” I don’t mean “urban core.” Activists on the Left often like to promote the idea that the most entrepreneurial, productive, and dynamic sectors of society are necessarily concentrated in urban cores. But the data does not show this. Rather “suburbanization” of both employment and labor is a longstanding trend, meaning that many sectors of the economy in recent decades have been decentralized out of the urban core, and each state’s most productive centers are often found in the suburban counties—where political leanings are not at all necessarily “blue.” Moreover, many of a state’s most productive workers—engineers, medical personnel, entrepreneurs, financial workers, for example—choose to live in suburbs. Thus, the most productive states are often states with large sprawling suburban areas, and not necessarily “big cities” in the twentieth-century sense.

The Red States Would Survive

Rep. Greene’s Twitter critics are clearly very enthusiastic about portraying Americans in red states as impoverished unsophisticated welfare queens unable to get by without wealth transfers from the blue states. It’s a convenient narrative, although an inaccurate one. It is likely in most scenarios, however, that secession would come with short-term economic dislocations and disruptions. Yet, short-term economic troubles have never been an insurmountable obstacle to secession and revolution. The American revolutionaries, after all, voluntarily cut themselves off from trade and took on huge debts to achieve political independence. Short term economic realities also do not dictate long-term prospects. If a Red States of America embraced global trade and a reduced regulatory burden, it could expect to see its economy accelerate in the medium and longer term. Moreover, cultural issues often trump economic ones, and residents may be willing to sacrifice some amount of wealth (measurable in dollars) for the perceived advantages of political self-determination. Were red-state Americans given the option to secede in exchange for per capita GDP levels similar to those of Germany, I suspect that many would take that bargain.