Authored by Matthew Pipenburg via Gold Switzerland,

Below we look at the interplay of embarrassing debt, dying currencies and failed monetary fantasies masquerading as policies to confirm that no matter how one turns or spins the inflation/deflation, QT/QE or recession/no-recession narratives, the global financial system is already doomed.

Recession: The Elephant in the Room

As I’ve been arguing in report after report, my view has been that the US, with its 125% debt-to-GDP and 7% deficit-to-GDP ratios, was, and already is, in a recession heading into 2023, despite official efforts in DC to re-define the very definition of a recession.

But a recession is still a recession, and an elephant is still an elephant, and both are fairly easy to see at a distance.

As of now, however, the recession has officially been avoided.

How comforting.

As with the inflation data, it’s nice when the folks in Washington can exercise their magical powers to move the goal-posts in mid-game whenever a little “cheating” helps their odds and fictional narrative.

For me, an elephantiac recession is now in the room.

The Empire Manufacturing data in my latest report, for example, supported this recessionary outlook.

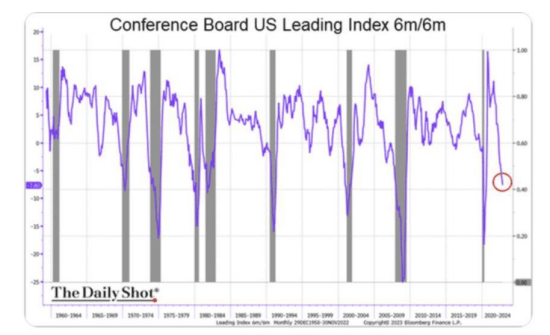

In case, however, we still need more recessionary evidence, the dramatic 6 month decline in the Conference Board’s index of leading indicators serves as yet another neon-flashing warning that the recession—if not under our bow—is certainly right off our bow.

Still Hoping for a “Softish” Landing?

Furthermore, and despite Powell’s belief that his office can manage a recession with the precision of a home thermostat, his faith in what he lately described as a “softish landing” is almost as farcical as his prior attempt to describe inflation as “transitory.”

Without wishing to appear “sensational,” as many of us blunt and math-based observers (from Burry to Middelkoop) of late are described, I will stick my tin-foil-covered head out and say candidly that I see nothing “softish” ahead.

Instead, I see either: 1) a financial crisis which will dwarf 2008 and/or, 2) an absolute tanking of the USD, whose unsustainable strength throughout 2022 was indeed “transitory,” as I argued numerous times.

The Simple Math of Liquidity

The simple math and reality of even centralized and central-bank distorted markets is quite simple: These markets rise and fall on liquidity.

Once the monetary “grease” required to maintain the MMT fantasy of mouse-click money as a debt solution “tightens” too tight or runs too dry, the entire house of cards of the post-2008 fairytale comes to a hard rather than “softish” end.

Again, we saw the first signs of this collapse in the “tightening” backdrop of 2022.

Of course, this critical “liquidity” won’t be coming from economic growth, rising tax receipts, a robust Main Street or a fairly-priced market.

Instead, and as expected, it now comes from out of thin air…

Is It a Race to the Bottom for Risk Assets?

The honest but scary numbers rather than fluffy but fictional words of our financial central planners make it all too clear that unless Powell puts his finger on the Eccles-based mouse-clicker to create more fiat money (highly inflationary), US and global credit markets will simply continue their race to the ocean floor (highly deflationary or at least dis-inflationary).

As credit markets sink and bond yields and rates rise, this also means that equity markets, who have been sickly addicted to years of central-bank repressed low rates and cheap debt, will merely join those bonds on the bottom of the dark ocean floor.

In short, bonds (and hence risk parity portfolios) won’t save you. Rather than hedge stocks, they are now correlated to the same.

More Easing Won’t Bring “Ease”

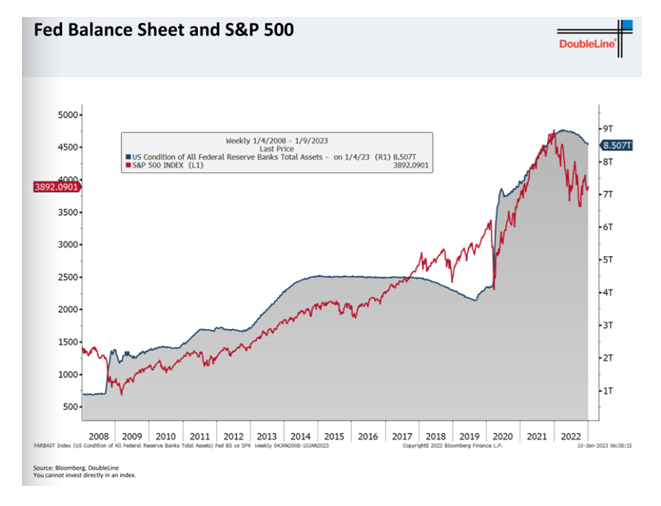

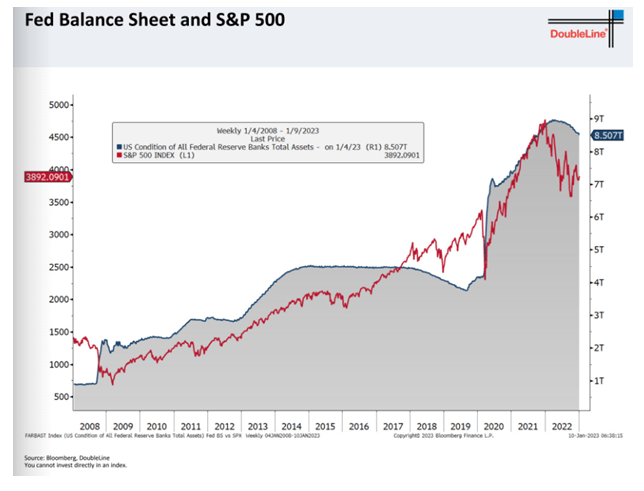

Failing outright and open bond default, it thus seems that an eventual capitulation to more magical “liquidity” and renewed QE is nothing short of inevitable, which means the USD’s fall from its 2022 highs is equally the case, as shown below.

But such “easing,” if realized, will lead to more inflationary-debased Dollars and hence more inflation dis-ease for investors.

This is hard for investors to fully grasp when the Dollar seems “strong,” but even that was an illusion, and one which hardly did any asset class any good in 2022 but for the Dollar itself.

The Damage Already Wrought by the Strong USD

In the interim, the cancerous ripple-effects of the Fed’s strong USD policies, as warned throughout 2022, continue their waves of destruction, as openly evidenced by the earnings reports from our beleaguered S&P.

Already, the early data coming from its listed companies is anything but positive.

As in the July and October earnings seasons of 2022, corporate earnings for 2023 are still drowning under the weight of the USD.

But we must also keep in mind that the DXY (which measures the relative strength of the USD) has fallen 11% (from 113.9 to 101.8) over the last quarter.

If the S&P hit an October bottom during a DXY high, what can we deduce from a now falling DXY?

Will markets rise like Lazarus?

This will be something worth tracking.

But why?

Strong Dollar or Weak Dollar, No One Wins…

Should earnings and hence stocks continue to decline despite the DXY declines, this would suggest that not even a weakening USD can save these post-08, over-stretched, Fed-addicted and debt-soaked markets.

However, should stocks rise on a weaker Dollar, the percentage gains in price will only be eaten away by the invisible tax of inflation and the increasingly debased value of the very dollars used to measure those so-called “appreciating” stocks.

In short, a no-win scenario…

For now, it seems the stock market only cares about the Fed rather than the DXY, as the Fed is the market.

That is, when QE is the meme, zombie markets rise; when QT is the meme, they fall.

Again, see for yourself:

Yellen, Squawking for a Weaker Dollar?

In fact, it was during those October market lows that the queen of toxic liquidity, former Fed-Chair-turned-Treasury-Secretary (imagine that?) Janet Yellen, was suddenly ringing the bell for more magical money—i.e., “liquidity.”

Specifically, Yellen was wondering who would be buying Uncle Sam’s IOU’s without more mouse-click money from the Eccles Building?

As my latest reports on the UST markets confirmed, the answer was simple: No one.

Instead, foreign central banks were and are selling rather than buying America’s bonds. Just ask the Japanese…

Is Yellen, contrary to Powell, silently suggesting that QT has backfired? Is Yellen, unlike Powell, realizing that there are no buyers for our increasingly issued yet unloved USTs but the Fed itself?

Perhaps these tensions within the Treasury market provide the hidden clues as to why the USD has been sliding rather than rising from the DXY’s October highs?

After all, a weaker USD means less forced need for foreign nations to dump their UST reserves to come up with the money to buy their own dying bonds and strengthen their own dying currencies as a direct response to Powell’s (and originally, Yellen’s) strong USD policy.

In short, perhaps our Treasury Secretary now wants to stop the bleeding in her Treasury market…

Weaker Dollar Ahead?

My current view is therefore this: We are seeing the slow end of the strong USD policy.

Why?

Because as warned throughout 2022, such a strong USD was a massive gut-punch to foreign currencies and hence foreign holders of USD-denominated debt.

Indirectly then, the strong USD was also a gut-punch to the UST market, which saw more sellers than buyers around a crippled globe. Hence Yellen’s backfired and back-stepping fears above…

Furthermore, and returning to the aforementioned topic of recessions, I also argued throughout 2022 that no recession in history has ever been solved with a strong currency.

Given that such a recession is, again, either directly off our bow or already under it, it is likely no coincidence that the USD/DXY is now falling rather than rising.

In short has Uncle Sam’s strong Dollar finally cried, well… “Uncle”?

Or more simply stated, has Yellen realized, in private, what we’ve been arguing in public, namely: That we are already in a recession and thus need a weaker Dollar.

Powell: Ignoring Reality & Yellen?

Meanwhile, however, you have the math-challenged but psychologically tragic Jay Powell wanting to save his legacy as a Paul Volcker rather than as an Arthur Burns.

Like a child wanting to be John Wayne rather than Daffy Duck, Powell and his rate-hiked strong USD refuses to see the $31T debt pile in front of him which makes it impossible to be a reborn Volcker, who in 1980 faced a much smaller debt pile of $900B.

In short, Powell’s America of 2023, unlike Volcker’s America of 1980, can’t stomach rising rates or a strong USD.

Or stated even more simply: Powell can’t be Volcker.

Will someone at the Eccles Building please remind him of this?

Doomed Either Way

Yellen or Powell, QT or QE, strong Dollar or weak Dollar, the global financial system is nevertheless doomed.

We either tighten the bond and hence stock markets into a free fall and economic disaster, or we loosen and ease liquidity into an inflationary nightmare.

As I’ve said so many times: Pick your poison—depression or hyperinflation.

Or perhaps both…namely stagflation.

Either way, of course, Powell, and the American economy, is now doomed. And he has only Greenspan, Bernanke, Yellen, himself and years of mouse-click fantasy to blame.

Supercore (CPI) Lies from On High

Meanwhile, the lies, twisted math and Nobel-Prize level mis-information continues…

Last week, for example, I reminded readers of DC’s latest attempt to mis-report otherwise humanly-felt inflation by tweaking an already-tweaked (i.e., bogus) CPI inflation scale.

But if that comedy wasn’t already comical enough, now welcome none other than Paul Krugman to this stage of open theatrics masquerading as economic data.

According to one of Krugman’s latest neoliberal economist tweets, “3-month ‘supercore’ CPI is below Fed’s 2% inflation target,” which naturally had those equally raggish economic playwriters at the WSJ almost galvanic with theatrical “good news.”

Hmmm.

What neither Krugman nor the WSJ seemed to recognize is that “supercore” CPI excludes food, energy, shelter and the price of used cars, so yes, absolutely, if you take away all the things that actually cost lots of money, inflation is no problem at all… Bravo!

Such shameless misuse of data and headlines, of course, is almost as shameless as the misuse of monetary policy we’ve been enjoying since the Troubled Asset Relief Program…

But as stated last week, such desperate tricks from on high will continue to mount as global financial problems do the same.

An Historical Turning Point

The astounding lack of accountability from the foxes guarding our financial hen house will one day be the stuff of history books, assuming history itself is not cancelled, as it seems the study of economics has already left the room.

The best we can hope for from the very “experts” who have brought the global economy toward a mathematically unavoidable cliff are now empty words and twisted math, as per above.

Such disloyalty from our financial generals on the eve of an unprecedented strategic and tactical economic defeat of their own making reminds me of officers sitting miles from the trenches as investors go “over-the-top” toward a row of cannons pointed straight at their trusting chests.

In short: Sickening.

Gold: A Far More Loyal Lieutenant

Gold was a far more loyal asset than stocks and bonds in the turbulent times of 2022; and given that 2023 portends to be even worse, we can expect better loyalty from this so-called “barbarous relic” of the past.

With inflation ripping and war blazing, many still argue that gold did not do enough.

Hmmm…

But gold in every currency but the USD (see above) would beg to differ.

Furthermore, and as argued so many ways and times, that USD strength will not hold, as gold’s price moves this year have already tracked.

Gold’s future strength and rise is thus easy to foresee, as gold doesn’t rise, currencies just fall.

It’s really that simple.

Got gold?