Oil prices are modestly higher this morning, erasing overnight losses on Trump’s ‘ceasefire extension’ after Iran attacked three ships in the Strait of Hormuz.

While headline roulette continues to drive oil prices incrementally, this morning’s inventory/supply data from DOE will provide some color on how the

API

-

Crude -4.5mm

-

Cushing +700k

-

Gasoline -5.2mm

-

Distillates -4.6mm

DOE

-

Crude +1.925mm

-

Cushing +806k

-

Gasoline -4.57mm – 10th weekly draw in a row

-

Distillates -3.43mm – 4th weekly draw in a row

Crude stocks unexpectedly saw a build last week (after a draw the week before) as did Cushing inventories. However, on the product side, the sizable drawdowns continue…

Source: Bloomberg

Since the war started, Crude stocks have risen significantly, while gasoline inventories have seen non-stop draws…

Source: Bloomberg

Weekly US implied gasoline demand is holding up despite elevated prices. The 4-week moving average indicate a slight rise of 32,000 barrels per day, while the more volatile weekly data series ticked down by 33,000 barrels per day. Meanwhile, US average gasoline prices remain above $4 a gallon. It was near $3 a gallon right before the Iran war.

Source: Bloomberg

The crude inventory build was more than offset by a huge 4.14mm barrel drawdown from the SPR…

Source: Bloomberg

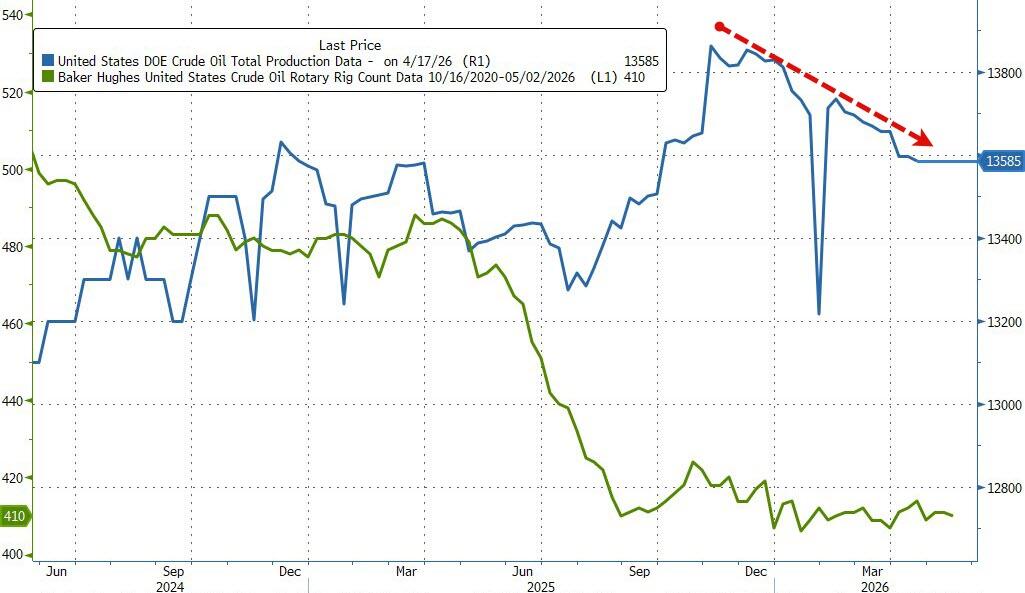

US crude production dipped once again…

Source: Bloomberg

Notably, total US oil product exports accelerated to a new record high last week…

Source: Bloomberg

WTI is holding gains for now, near yesterday’s highs around $92…

Finally, as The Wall Street Journal reports, analysts and commodities trading company executives are expressing shock at what they call a disconnect between market pricing and reality.

Prices of the most-active Brent futures contract are holding below $100 a barrel despite escalating tension in the Strait of Hormuz and the cancellation of U.S.-Iran peace talks. Just today, two attacks on ships in the waterway showed that the fight for control of the strait continues and spooked shipowners and crew members. Here’s what I’m hearing from experts and industry leaders at the Financial Times Commodities Global Summit in Lausanne, Switzerland:

“The lack of price discovery that we are seeing is so worrying to me, because in reality we are storing up a bigger problem for the future,” said Amrita Sen, founder and director of market intelligence at Energy Aspects. Price discovery refers to the process of buyers and sellers determining the fair price of a good or an asset in the futures market.

“Futures prices are meant to do the job of giving signals to sort out supply and demand. We are doing the opposite,” she said in a panel.

In 2022, when Russia invaded Ukraine, the market didn’t experience nearly as large a physical disruption as this time, and yet oil prices went much higher and stayed between $110 and $125 a barrel for months, said Saad Rahim, chief economist at Swiss commodity trader Trafigura, at the conference yesterday.

“This time, the scale seems to be something where the market cannot get its head around it, and therefore it says, we are not going to think about it.”

The world is already losing an average of 10 million barrels a day of crude oil and 5 million barrels a day of oil products. Hits to the world’s supply of fertilizers and chemicals are also severe.

Tyler Durden

Wed, 04/22/2026 – 10:40