Summary:

- Colombian Bonds, Stocks Rise as Right-Wing, Trump-Backed Espriella Wins Vote

- Trump-Backed “El Tigre” Wins Colombia Presidency As Socialist Era Ends

Colombian Assets Rise After Trump-Backed Candidate Wins Presidential Election

Colombian-dollar bonds surged across the curve on Monday, led by notes due in 2054, as traders bet that right-wing Abelardo de la Espriella’s presidential win will cut taxes, reduce spending, crack down on crime, and reopen the oil industry to unleash an energy revolution.

According to Bloomberg data, bonds due in 2054 led the advance, up 0.8 cent to 116.9 cents on the dollar.

Colombian 2036 dollar bonds are rising. Peso jumped 1.5%.

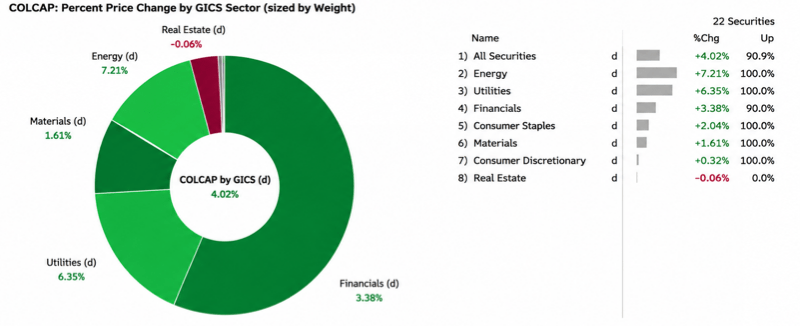

Colombia’s version of the S&P 500, COLCAP, jumped 4% on Monday, with energy stocks leading, up 7.2%.

Credicorp said Colombian stocks could rise 5% following the election and as much as 20% over the longer term, while local yields could slide by 150-200 bps in the months ahead.

BTG Pactual analyst Munir Jalil penned a note earlier today that outlined De la Espriella’s win as “directionally constructive given the market-friendly platform on security, taxes, investment, and hydrocarbons.”

“However, the near-term asset rally may be more contained than after the first round, as part of the outcome was already priced and the external backdrop is less supportive,” Jalil said, adding, “We expect the COP and TES to react positively at first. Still, the move’s durability should depend on the cabinet, the transition, fiscal signals, and the ability to build a stable congressional majority.”

De la Espriella’s government plan

JPMorgan analyst Diego Pereira said, “A one-point win is still a win, but one this thin reshapes both the mandate and the politics of delivery across fronts.”

Pereira’s view on Colombian markets:

Local markets:

We remain OW TES and long Sep-2030 TES, expecting the next leg of the rally to be driven by greater clarity on governability and fiscal consolidation plans. We stay MW COP and close the outright short COP vs BRL and MXN we had as a hedge for our position in bonds as the market settles after the open

Sovereign credit:

We reduce our OW weighting from 1.0 to 0.5 given potential tensions during the transition period from the revealed stark polarization.

Corporate Credit:

In the corporate space, we have expressed our view on Colombia’s elections through OW recommendations on the belly of Ecopetrol’s curve — the ’32s, ’33s, and ’36s — alongside an OW on Bancolombia’s 2034 notes

Equities:

With today’s official confirmation of Abelardo de la Espriella’s victory, we view the result as confirmation of a policy regime change, which should support a broader re-rating in Colombian equities. From an equity strategy perspective, Energy offers the clearest opportunity around this outcome, and Ecopetrol (Neutral, covered by Milene Carvalho) stands out as the most direct way to gain exposure.

De la Espriella’s win on Sunday night is part of a once-in-a-generation political shift across Latin America, a region ruled for years by nation-killing socialist regimes that have been voted out of office due to failed progressive policies sparking violent crime waves and economic turmoil. The rise of market-friendly, right-wing leaders has sparked rallies across the continent.

Amazing what happens when USAID gets defunded.

Take Argentina, for instance, where assets have jumped under right-wing President Javier Milei as he pushes to reset the economy.

Trump-Backed “El Tigre” Wins Colombia Presidency As Socialist Era Ends

South America is undergoing a once-in-a-generation political realignment as voters turn against left-wing and unhinged socialist governments and embrace common-sense right-wing leaders who promise law and order, economic reform, and national renewal.

The political shift across the Americas gained further momentum on Sunday evening after Abelardo de la Espriella, backed by President Trump, won Colombia’s presidential runoff in a narrow victory over left-wing senator Iván Cepeda. This is a major blow to the socialists, coming after four years under the left-wing administration of Gustavo Petro.

With 99.65% of ballots counted in the preliminary tally, de la Espriella had 12.91 million votes, or 49.65%, compared with Cepeda’s 12.67 million, or 48.7%. The margin was about 248,000 votes, narrower than de la Espriella’s first-round advantage three weeks earlier.

Polymarket

De la Espriella, who has referred to himself as El Tigre (the Tiger), has now put Colombia back on track to shift right after four years of disastrous socialism. This follows recent right-wing victories in Honduras and Chile, with Peru also leaning right. The 2024 re-election of right-wing Nayib Bukele, who fundamentally transformed El Salvador into one of the region’s safest countries, is another example.

In 2023, Javier Milei was sworn in as president of Argentina, aiming to reverse years of far-left control that had devastated the nation with inflation and debt. Earlier this year, U.S. Delta Force operators removed socialist Nicolás Maduro from power in Venezuela.

The shift across the Americas is part of a broader backlash against progressive policies that have sparked surging violent crime, economic stagnation, debt traps, currency declines, and collapsing public confidence.

Americas Political Map: Presidential Shift From Left To Right

Country-by-country presidential shift tracker

Back to De La Espriella, who ran on a simple platform popular among right-wing leaders in the Americas: restore law and order and rescue the country from the economic ruin progressives had created. He has also vowed to “disembowel” the left in Colombia.

Meanwhile, Petro, who was constitutionally barred from seeking re-election and backed Cepeda, alleged irregularities in the preliminary vote count and blamed Israel…

“This means that the software was compromised and others wrote data for polling stations and voting posts. The only entity in the world capable of doing that is the state of Israel,” Petro wrote on X.

The pattern is clear: the Western Hemisphere experimented with nation-killing progressive policies that have largely failed and have entered a rejection phase. This gives rise to right-wing governments that support Trump, coinciding with his mission to clean up the West, whether by dismantling narco-terrorist command-and-control structures, pushing Chinese influence out of the region, or simply stopping the rise of socialism and communism.