Last year, a cocoa shortage drove up prices for European chocolate makers and consumers.

This was largely due to an exceptionally wet rainy season as well as a viral cocoa disease that severely impacted the 2023/2024 harvest in West Africa. However, the situation is expected to improve this year, according to industry experts.

In a note published at the end of February, the International Cocoa Organization (ICCO) estimated that the 2024/2025 harvest is expected to show a surplus, after three consecutive years of deficit.

Nearly 65 percent of the world’s cocoa is harvested in just four West African countries: Côte d’Ivoire (38 percent), Ghana (12 percent), Nigeria (7 percent), and Cameroon (7 percent).

South America comes in a distant second place for volume, with Ecuador and Brazil as the main producing countries, accounting for 10 percent and 4 percent of global production, respectively.

The vast majority of the world’s cocoa is then exported to Europe and North America, where it is processed into chocolate and primarily consumed.

The Netherlands, Germany, and Belgium, for example, together import approximately 25 percent of the world’s cocoa beans. This makes the European Union the world’s largest importer of cocoa, accounting for 60 percent of global imports.

The United States and Canada, for their part, together import the equivalent of approximately seven percent of global production.

Germany has activated its first permanent foreign troop deployment since World War II, establishing a 5,000-strong armored brigade in Lithuania. This decision follows Defense Minister Boris Pistorius’ announcement in 2023 to bolster troop presence on NATO‘s eastern flank in response to the ongoing Russian-Ukrainian War.

The deployment demonstrates Germany’s willingness to take a leading role in the conventional defense of Europe with Brig. Gen. Christoph Huber emphasizing, “We’re not only moving toward operational readiness; we’re taking responsibility.”

According to the Bundeswehr, the brigade will consist of three major combat units—including a mechanized infantry battalion, a tank battalion, and the multinational enhanced Foreign Presence Battle Group Lithuania—and will be complemented by combat and support elements. The brigade aims to be at full operating capability by 2027.

Addressing a NATO Vulnerability

The need for additional NATO forces in Lithuania is largely due to its geographical location between Russian-allied Belarus and the Russian exclave of Kaliningrad. Kaliningrad, an isolated port city, was once part of Prussia and was ceded to the Soviet Union after World War II under the Potsdam Agreement. Following the collapse of the Soviet Union, the region was incorporated into the Russian Federation and now hosts the country’s Baltic Fleet, as well as troops, fighter jets, and nuclear-capable Iskander missiles.

The narrow corridor between Lithuania and Belarus, known as the Suwalki Gap, is widely regarded as NATO’s most vulnerable point. Should Russian forces launch an attack on Lithuania, Latvia, or Estonia, which are all NATO member states, they could potentially sever their supply lines from Poland by linking Belarus and Kaliningrad through an offensive. Stationing permanent NATO troops in the three Baltic states serves as a long-term security guarantee.

Germany’s New Policy of ‘Zeitenwende’

Due to its historical responsibility following World War II, Germany has traditionally maintained a cautious and restrained military stance. Massive defense cuts in the 1990s and 2000s further weakened its defense capabilities. In response to new geopolitical challenges, Federal Chancellor Olaf Scholz introduced in 2022 the Zeitenwende—a “turning point”—in German security policy. This new strategy aims to strengthen defense capabilities, increase military spending to meet NATO targets—which Germany achieved for the first time in 2024 by reaching the 2 percent mark—and enhance European security cooperation. The recent deployment to Lithuania serves as its flagship project.

Germany has made meaningful progress, and a clear shift in thinking within the German defense establishment is evident, particularly through initiatives like the creation of a special fund for defense spending to kick-start military investment.

Europe Needs to Step Up So US Can Shift Focus to Indo-Pacific

In times when European politicians express concerns that the U.S. is indifferent to Europe’s fate, it’s important to remember that the current administration is encouraging allies to step up and ensure they are able to deter potential dangers on their own terms. This is a task that all sovereign nations must undertake.

The United States needs to shift strategic focus to the Indo-Pacific to deter China, and steps like this one taken by Berlin are critical if Germany and other European NATO members are to take primary responsibility for their own conventional defense. Washington should applaud the new German base in Lithuania and encourage other wealthy Western European nations to follow suit with bases in Latvia and Estonia.

* * *

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

People and businesses across China are feeling the pressure as the Chinese authorities vow staunch resistance to the United States and the Trump administration’s tough approach to trade and bilateral relations.

Chinese companies, workers, and industry insiders have reported being caught in a bind by the escalating U.S. tariffs, as usual orders are not coming in, and some companies are being compelled to take extreme measures.

While Chinese social media is flooded with anti-U.S. propaganda and nationalist content, posts and videos warning of mass layoffs and prolonged “vacations” offer some indication of the unease spreading throughout an export-driven economy already struggling with high unemployment, shrinking profits, and declining foreign investment.

On April 11, U.S. President Donald Trump hiked the blanket tariff on most Chinese products to 145 percent in response to the Chinese regime slapping its own 125 percent retaliatory duty on American goods the same day.

In addition, Beijing on April 14 restricted the export of seven types of rare earth products critical for high-tech and military manufacturing in the United States and other countries.

According to a White House fact sheet published on April 15, some Chinese products may now face U.S. tariffs of up to 245 percent.

Trump has cited unfair trade practices and illegal drug trafficking as reasons for imposing the levies on Chinese goods.

Washington, particularly starting with the first Trump administration, has long called out the Chinese regime for decades of distortionary and protectionist economic policies, as well as rampant industrial espionage.

Trump also criticized Beijing for failing to curb the production and export of the deadly synthetic opioid fentanyl, which often entered the United States through Mexico.

The U.S. Drug Enforcement Administration said in a December 2024 press release that more than 107,000 people died from drug overdose in 2023, with nearly 70 percent of those deaths linked to opioids such as fentanyl.

Chinese Companies Feel the Crunch

Li Meng-chü, a Taiwanese businessman, told the Chinese edition of The Epoch Times that the heightened U.S. tariffs will force a significant number of export-oriented factories in China to scale back their businesses or close entirely.

The owner of a factory that makes flashlights in the city of Yiwu, Zhejiang Province, told The Epoch Times that while export companies used to place three or four bulk orders with the factory a month, business has completely dried up as of late. Many workers who used to work six days a week now take three or four days off.

Li, the Taiwanese businessman, said that to his knowledge, factories in the southern Chinese province of Guangdong that produce electronics, garments, and lighting that had U.S. orders placed through to the end of the year, have now seen those orders abruptly canceled. Much stock has been left sitting in the factories.

The South China Morning Post, a Hong Kong-based English-language outlet, reported on April 10 that some Chinese exporters have opted to surrender their cargo to the shipping companies mid-voyage rather than deal with the new tariffs.

“No one will buy them after the tariffs are imposed,” the publication quoted one client as saying to a Chinese exporter.

Mainland Chinese outlet Caixin reported that the port of Shanghai—normally bustling with ships—was virtually empty on the day after the United States imposed its 145 percent tariff. The outlet expects U.S.–China shipping to fall by half in the near future.

In the wake of the tariff hikes, Chinese fashion giant Shein attempted to shift some of its production out of China, but was barred from doing so by the Chinese authorities.

Shein and Temu, another Chinese online retailer, will see price hikes following the cancellation of the de minimis shipping exemption, which allows packages containing goods worth $800 or less to be imported duty-free to the United States.

The restriction is set to apply to mainland China and Hong Kong starting on May 2, affecting about 11 percent of current U.S.–China trade.

Beijing Doubles Down

On April 8, a day before the Trump administration put a 90-day pause on tariff hikes targeting scores of countries worldwide, Beijing’s commerce ministry said it would “fight to the end” with the United States on trade.

The Chinese commerce ministry said China’s retaliatory actions were a “completely legitimate” means of protecting national interests and “maintaining the normal international trade order.”

Introducing a 28,000-word white paper on U.S.–China trade, a commerce ministry official said on April 9 that Beijing “possesses resolute determination and a wide range of measures” to counter American tariffs and other economic and trade restrictions.

In a regular press conference held April 10, Chinese foreign ministry spokesman Lin Jian said that Beijing “is not scared” of fighting a trade war.

Tough Times Ahead

Meanwhile, Chinese businessmen and bloggers have questioned where the Chinese Communist Party’s (CCP) obstinacy and propaganda will lead them.

According to an early April report by a mainland Chinese blog called “Logistics and Supply Chain Management,” a furniture factory owner in Jiangsu Province, eastern China, calculated that with all the additional fees, a tariff of just 20 percent would consume the factory’s entire profit.

Liu Ming, director of an electronics factory in the Jiangsu city of Suzhou, who used a pseudonym, told the blog that while the company had a profit margin of 16 percent in 2024, “now that the tariffs have been applied, we are operating at a loss.”

Posting on social media platform X, a Chinese exporter who works with American clients said that when the tariff was still 34 percent, it was still possible to work with the raised rate, but the 125 percent tariff “amounts to wiping out Chinese workers’ jobs.”

“As far as I know, nearly all U.S. importers have stopped shipments from China,” he said.

A worker in Dongguan, Guangdong Province, said in an April 9 video posted to Chinese social media that with tariffs eliminating all profit margins from those exporting to the United States, factories and suppliers will be compelled to compete with each other in the domestic Chinese market.

“It’s going to be a race to the bottom,” he said. While not directly criticizing how the CCP handled the trade disputes, he called out Chinese netizens who “spend all day on the internet talking about fighting [the trade war] ‘at all costs.’”

“I bet you’ll soon find yourselves among those ‘costs,’” he added.

A vlogger in Nanjing, the capital of Jiangsu Province, said earlier this month on social media that the Chinese market’s ability to absorb the country’s consumer products would not be enough for a significant number of workers to keep their jobs.

“Many companies engaged in foreign trade are sure to cut production,” the vlogger said.

A finance worker in Xiamen, a coastal Chinese city in Fujian Province, warned on April 9 that the export business coming to a standstill would have far-reaching effects beyond manufacturing and logistics. “Don’t quit your job, keep it if you can,” she said in a social media post.

‘A Series of Traps’

China expert and current affairs commentator Wang He told The Epoch Times that the CCP may not have anticipated Trump’s move to pause the raft of global reciprocal tariffs he announced on April 2.

“The CCP wanted to take the opportunity to form an anti-U.S. united front” with countries around the world affected by the U.S. tariffs, only to be the odd one out in refusing to negotiate, he said. “As a result, communist China walked into a series of traps that Trump set for it.”

Earlier, on April 9, while at a White House event, Trump had expressed confidence that “China wants to make a deal.” However, he added, “It’s one of those things they don’t know quite—they’re proud people.”

Speaking on April 15 at a press briefing, White House press secretary Karoline Leavitt said that “the ball is in China’s court” as far as talks go.

“China needs to make a deal with us. We don’t have to make a deal with them,” Leavitt said, noting that she was quoting the president.

On April 17, Trump told reporters at the White House that China had contacted his administration.

“I believe we’re going to have a deal with China, and if we don’t, we’re going to have a deal anyway, because we will set a certain target, and that’s going to be it,” the president said.

Satellite Images Expose China’s Secretive Nuclear Submarine Force

Newly published satellite imagery shows the latest developments at a Chinese naval base, which serves as the hub for China’s nuclear-powered submarine fleet.

Naval analyst Alex Luck noted that Google Earth recently updated satellite imagery of China’s Qingdao First Submarine Base on the eastern coast. The images reveal at least six submarines docked near a pier, with one additional submarine visible in a drydock, per Luck’s observations.

The analyst observed that five of the nuclear-powered submarines captured in the imagery were equipped with conventional armaments.

The sole Chinese Type 092 nuclear-powered ballistic missile submarine also appeared in the image. The experimental Type 092 is now inoperable and is replaced by its more advanced successor, the Type 094, the Federation of American Scientists wrote in a report in March. With regard to the unidentified submarine in the drydock, Luck suggested that it could be a boat undergoing scrapping, given maintenance is regularly also performed at another site. -Newsweek

The latest research by Department of Defense says it believes that China will expand its submarine fleet from 60 to 65 by the end of 2025. China’s submarine fleet could reach 80 in the next ten years, according to the Pentagon.

As China continues to expand its military might, the new chairman of the Joint Chiefs of Staff, Gen. Dan Caine, is sounding the alarm of the U.S.’s ability to confront China. “The U.S. does not have the throughput, responsiveness, or agility needed to deter our adversaries,” Gen. Caine told the Senate Armed Services Committee.

The U.S. military is bracing for possible confrontation with China over the Taiwan Strait. Adm. Sam Paparo, head of U.S. Indo-Pacific Command, warned that China is actively preparing for major military actions targeting Taiwan, according to the Washington Times.

China is said to be building a novel type of amphibious vessel called Shuiqiao, or “water bridges,” to bolster a possible Taiwan invasion, the India Defense Review reports. These adaptable barges are engineered to swiftly transport heavy equipment across challenging coastal terrain, the report said.

Taiwan’s president, Lai Ching-te, has vowed to boost the island nation’s defense spending to 3 percent of its gross domestic product. The increase would bring its military spending to up approximately one-fifth of its total spending budget.

“Of course, there is the possibility that Xi Jinping would decide that this is the right time for the Chinese Communist Party to take aggressive action,” Sen. Chris Coons (D-DE) said of China’s dictator. “I think it’s exactly the wrong thing for them to do,” Coons added. “I think they would find a forceful and united response.”

A federal judge ruled against the Trump administration’s executive order banning the use of an “X” on passports marked by people self-identifying as neither male nor female.

U.S. District Judge Julia Kobick of the District Court of Massachusetts – who in 2017 was part of a legal team that sued the Trump administration over an ACA provision and has been a judge less than 18 months, awarded the American Civil Liberties Union (ACLU) a preliminary injunction on April 18, staying the president’s executive action requiring sex, instead of gender identity, to be used as an identifier on government-issued identification documents.

The executive order titled “Defending Women from Gender Ideology Extremism and Restoring Biological Truth to the Federal Government” was one of several signed by President Donald Trump on his first day in office.

“It is the policy of the United States to recognize two sexes, male and female,” the order stated. ”These sexes are not changeable and are grounded in fundamental and incontrovertible reality.”

The order stated that gender identity “reflects a fully internal and subjective sense of self, disconnected from biological reality and sex and existing on an infinite continuum, that does not provide a meaningful basis for identification and cannot be recognized as a replacement for sex.”

It ordered the secretaries of State and Homeland Security, and the director of the Office of Personnel Management to “implement changes to require that government-issued identification documents, including passports, visas, and Global Entry cards, accurately reflect the holder’s sex.”

It also ordered the rescinding of prior federal guidance documents, including “The White House Toolkit on Transgender Equality.”

The ACLU took legal action against the order on behalf of five plaintiffs who identify as transgender and two who identify as nonbinary, seeking to preserve the pro-LGBT policies put in place under President Joe Biden, allowing a third option on identification documents.

“We all have a right to accurate identity documents, and this policy invites harassment, discrimination, and violence against transgender Americans who can no longer obtain or renew a passport that matches who they are,” ACLU lawyer Sruti Swaminathan said in a statement.

The Trump administration argued that the president had broad discretion in setting the passport policy, and those policy changes did not “violate the equal protection guarantees of the Constitution.” The federal government also denied any harm befalling the plaintiffs due to the policy, since they were still free to travel abroad.

The judge said the administration didn’t demonstrate substantial government interests in changing the rule.

“The Executive Order and the Passport Policy on their face classify passport applicants on the basis of sex and thus must be reviewed under intermediate judicial scrutiny,” Kobick wrote. “That standard requires the government to demonstrate that its actions are substantially related to an important governmental interest. The government has failed to meet this standard.”

Stacy Robinson and The Associated Press contributed to this report.

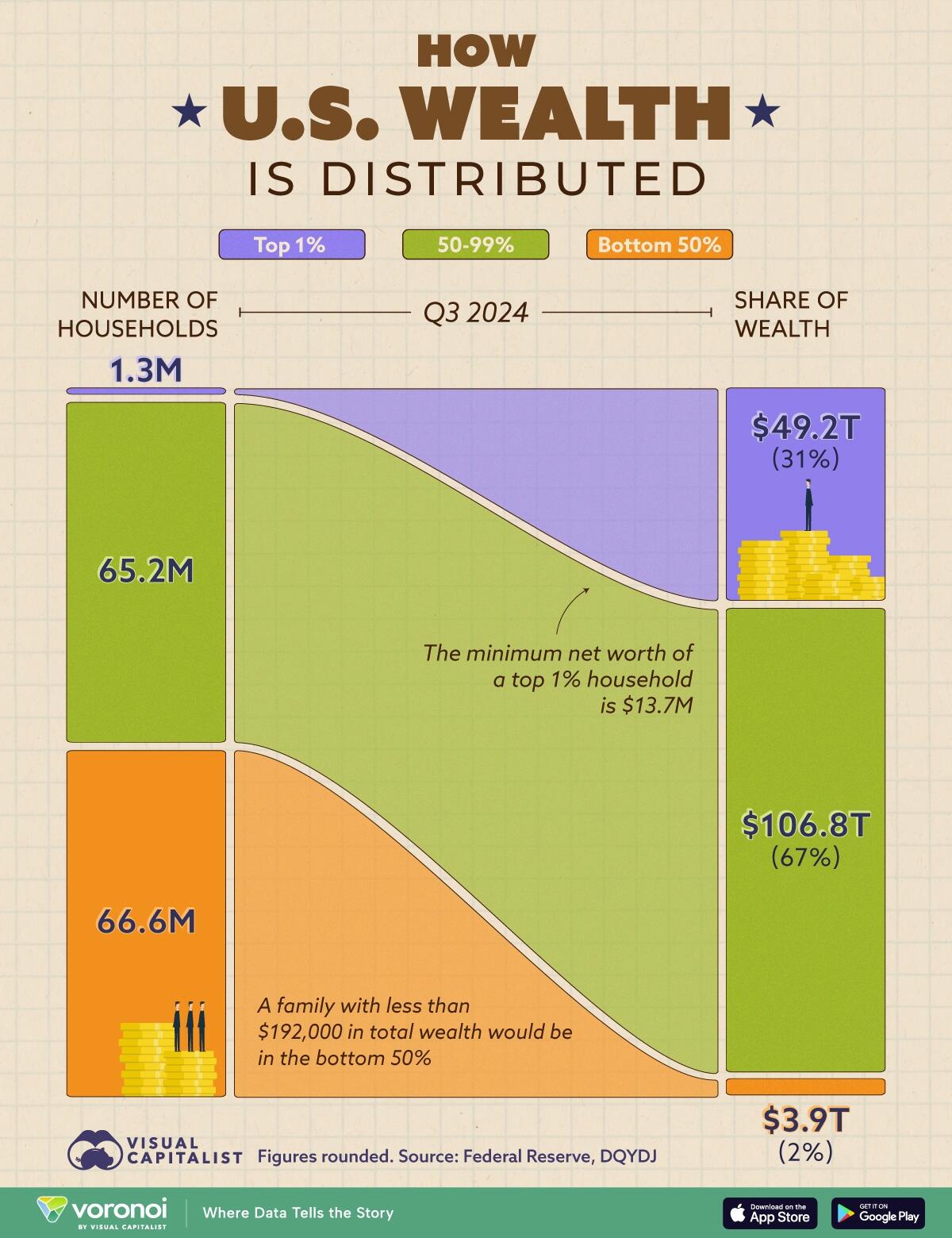

There are two types of households in the U.S.: the rich half and the poorer half.

And the data is quite striking in this regard.

This graphic, via Visual Capitalist’s Pallavi Rao, breaks down America’s wealth (the total net worth of all U.S. households) by wealth percentile, and lists the number of households in each percentile.

Data for this chart is sourced from the Federal Reserve as of Q3, 2024.

U.S. Wealth Distribution is Top Heavy

For reference, the total net worth of all U.S. households is close to $160 trillion.

The rich half own about $156 trillion (or about 98% of it). The poorer half only own about $4 trillion.

Breaking down that top half even further, the top 1% (1.3 million families) owns about $49 trillion (or about one-third of the total share) by themselves.

And going even further, about half of that $49 trillion is owned by the top 0.1%. That’s only around 136,000 households and includes all of America’s wealthiest people.

Demographics of Wealth Bands

The Federal Reserve also has some insight of how much one needs to own in each wealth band.

From their last analysis in 2022, households with less than $192,000 were the bottom 50% of the country. This band also had a higher concentration Black or Hispanic families without a bachelor’s degree.

On the other hand, to be in the top 10% (not pictured in this graphic), a household needed at least $1.92 million in 2022. Asian and White families with at least a bachelor’s degree were overrepresented here.

To find out the threshold for the top 1%, a different source, DQYDJ, estimated $13.7 million as the minimum household wealth. It takes $62 million for a household’s net worth to be in the top 0.1%.

We’re getting close to 90 days and even coming up close, in a week, 10 days, to the first 100 days of the Trump administration and this counterrevolution that he’s waging.

I thought it might be wise just to see where we are as far as the political landscape and the dynamics of the progress of this counterrevolution.

I think I would sum it up as flooding the zone. And that is, he’s going to try to propose and enact so many radical corrections or revolutions or reforms or recalibrations that his opposition doesn’t know where to start.

So, abroad, he is looking at the Iran deal and he got rid of it. He put sanctions.

He’s got maximum pressure. And now, the Iranian economy is about defunct. And they want to negotiate about this nuclear weapon. I don’t think they’re going to negotiate it away, but we’ll see.

And then, he’s dealing with Ukrainian President Volodymyr Zelenskyy and Russian President Vladimir Putin and trying to get a ceasefire.

He’s basically dealt with the Houthis.

On the domestic front, there is no more illegal immigration.

He’s basically stopped it. Now, the task is what to do with the 12 million illegal aliens that came under former President Joe Biden. And what do you do with the 20 million-plus, maybe 30 million that were here already illegally but for a longer period of time?

At the same time, he’s had a blanket mandate that in every Cabinet they will eliminate diversity, equity, inclusion and, by association, things like transsexual, biological males competing in women’s sports.

Women—lowering the physical standards so women could compete and pass these very rigorous endurance physical tests so that they would be in combat units on an equal level. No problem that they can’t. But they have to have the same physical requirements as men.

I could go on, but you see what he is doing.

He’s doing so many radical corrections in a way that a Romney or a McCain or the Bushes, even Ronald Reagan would not have dreamed of that he feels the opposition will say, “Well, what do we do? Should we reply here? Do we put our interest here? Should we do this?”

And so, what is the strategy that the Left is using?

They’re flooding the zone, too. But they’re doing it not with counterproposals. They don’t say, “This is what’s wrong with closing the border and we wanna reopen it. This is what’s wrong with the Houthis policy. This is what’s wrong with the trade deficit. This is what’s wrong”—no specific proposal.

They’re just flooding it with hysteria, the Spartacus talk, late-night comedy trashing him, another person arrested saying that he wants to kill Donald Trump, keying Teslas, firebombing Tesla agencies, outrageous things from Hollywood stars, videos from Congress. All of a sudden—we didn’t even know who Rep. Jasmine Crockett was. She’s filled that void.

But what I’m saying is they want to be so rambunctious, so crazy, so 360 degrees unhinged that they’ll create an image or a malu—where everybody wants to get almost in a fetal position: “Please, please make it all go away. I don’t know what Trump is doing but it’s so disturbing. Everybody’s so angry.” That is their strategy.

Now, what is Trump’s counterstrategy?

His counterstrategy is to actually get people on the other side of the aisle in Congress or in the country at large or in the popular culture and try to at least be friendly to them so then they can say, “I don’t agree with Trump but what he’s doing might be needed.”

So, we have Bill Maher going to Mar-a-Lago and actually saying very nice things about Donald Trump.

On the one hand, we have Health and Human Services Secretary Robert F. Kennedy Jr. fighting with a bulwark of the Left at one time, fighting with left-wing people who were calling him all sorts of names and saying that he is illiberal.

We had Gretchen Whitmer, the governor of Michigan. She was in the White House. Can you believe it? She was so embarrassed about a photo-op. She had to almost cover her face.

But you can see what Trump is doing. He’s trying to get people from all sides of the Democratic and liberal progressive movement and not compromise them, but get in the picture, so then the Left will say, “Well, how can we appeal to the public and get them all angry and frenzy and hysterical when some of our major celebrities, our political figures are in Mar-a-Lago?”

Bush-Era Swamp Creature Revealed To Be Key Figure In OKC Bombing Coverup

“As I have always said: The only difference between the KGB and the FBI is that the KGB has never claimed to be a legitimate law enforcement agency.” ~ Jesse Trentadue

Readers may know the name John Ashcroft, attorney general under George W. Bush.

Well, good old Ashcroft was at the heart of a high profile cover-up: the Oklahoma City bombing, according to attorney Jesse Trentadue.The following comes from a court filing provided to ZeroHedge by Trentadue, attorney to OKC bombing accomplice Terry Nichols.

For context (per Jesse from kennethtrentadue.com): Jesse is the brother of Kenneth Michael Trentadue who died in August 1995, while incarcerated at the Federal Transfer Center in Oklahoma City, Oklahoma. Following the death, the Department of Justice (DOJ) immediately deemed it a suicide, denied the medical examiner access to the cell where Kenneth Trentadue was killed, ordered the cell cleaned and painted, and repeatedly asked both the medical examiner and Kenneth Trentadue’s family to authorize the cremation of his body. The medical examiner could not legally authorize cremation and the family refused, demanding that Kenneth’s body be returned to them. When Trentadue’s body was returned to the family, they removed heavy makeup and discovered bruises all over his body, from head to foot. The bruises, cuts, and other wounds depicted an obvious beating and murder.

Now for the story…

While serving his prison sentence, Nichols attempted to spark an investigation into FBI involvement in the OKC bombing. He sent a letter stating that he could provide such information to the then head of the DOJ Ashcroft.

Ashcroft did not respond to the letter but immediately forbade the media from speaking to Nichols, which resulted in 60 Minutes cancelling a sit-down interview they had scheduled with Nichols, says Trentadue. Shortly thereafter, Nichols said he received a visit from a man presenting an offer from the DOJ to undo Nichols’ death sentence if he agreed to three conditions:

Take ownership of an anonymous warning the DOJ received saying the Murrah Building was bombed 30 minutes before it actually had been.

Implicate Nichols’ own brother in the bombing plot.

Reveal the location of the “Kinestick”, an explosive used in the bombing. Nichols mentioned having knowledge of an unused stache in his letter to Ashcroft. The existence of a remaining stache was not known at the time.

The existence of the mysterious call was independently corroborated in Stephen Jones’ book Others Unknown and even covered by ABC News:

ABC News 20/20 reports on how someone called the Executive Secretariat in DC about a half hour before the OKC bombing and said “the Murrah building has just been bombed” pic.twitter.com/XzMTFiCG6r

It was discovered that the DOJ proxy (Michael Selby) who visited Nichols previously worked in Ashcroft’s private security detail. Trentadue helped to further corroborate that this meeting took place by telling ZH:

After the declaration was filed, Selby called me upset as hell. Said that I had just got him “fucking killed.” The attorney who brought Selby into meet Nichols is Rodney Uphoff. A law professor at the University of Missouri. I called Uphoff and he confirmed the event.

It is strange that such an offer – giving leniency to an accomplice to one of the most horrific domestic terrorist attacks in U.S. history – would be presented by someone who does not work at the DOJ and stipulate that Nichol take credit for an anonymous tip which he did not make.

Nichols ultimately did not accept the deal because he did not want to throw his brother under the bus.

The story, now part of official record thanks to Trentadue, serves as an interesting look into the true conspiracies that Ashcroft may have had a hand in.

To see the full spectrum of official documents that Jesse Trentadue has fought hard to force the government to release, follow his website named in honor of his brother who he believes was murdered by the FBI: http://www.kennethtrentdue.com/

And for a great interview where Trentadue discusses the contents of this article and more, listen to friend-of-ZeroHedge Scott Horton interview Jesse just last month.

As for Ashcroft, after ‘retiring’ he started a private lobbying firm that quickly secured the Israeli government as its first client.

The company he heads is a prime example of that spirit. Founded more than 50 years ago by a Vietnam vet with machinery made from parts found in a local landfill, the knife company boasts that it’s “three generations strong.”

Roy believes domestic companies will thrive under the import tariffs enacted by the Trump administration.

With consumption accounting for nearly 70 percent of the U.S. economy, Roy believes there is a strong market for products made in America.

In 2023, nearly half of the goods purchased by Americans were “made in America,” according to the Department of Commerce. That figure comes with the caveat that “made in America” sometimes means “assembled in America,” with products containing imported components.

The total gross domestic purchases in the country reached $3.7 trillion, with $1.9 trillion of that amount attributable to U.S. industries.

“When you keep it domestic and your dollars here [in America], it pays off,” Roy says proudly, wearing a T-shirt and cap emblazoned with his company logo.

“We rode out a pandemic, and we’re going to ride through these tariffs,” he told The Epoch Times.

That’s not just a bold statement, Roy said.

After President Donald Trump announced a sweeping array of tariffs on April 2, Roy reported that Dawson’s knife sales increased from $11,000 to $15,000 per day.

He said the company expects orders to double from 4,000 to 8,000 for 2025. It produces 40 different models of knives, including hunting, survival, culinary, and heirloom varieties.

Roy is convinced that many American companies can withstand a global trade war by sourcing materials domestically and maximizing production efficiency.

“In order to have that efficiency, we have to really invest in computers … everything to help us down the line to make better models, better manufacturing, and reduce steps,” he said.

The company currently employs 15 people and operates within 12,000 square feet of industrial space.

Roy said many consumers prefer goods that are “completely American-made.”

He does not foresee any problems sourcing materials as long as his domestic supply remains steady within a global tariff environment.

Government policies that impact his suppliers have also been a challenge.

Roy said that a longtime steel producer and supplier in New York recently went out of business due to restrictions on coal—a key ingredient in steel production.

Dawson Knives had maintained a working relationship with the steel producer since the company started in 1973.

However, another U.S.-based company has stepped in to smelt the needed steel, Roy said.

Despite potentially higher costs for some raw materials in the United States, Roy expects that using domestic suppliers will mean fewer “headaches” related to shipping and no import duties.

He views this as a distinct advantage.

With the materials he currently has in stock, and absent any unforeseen circumstances, he expects to weather a global trade upheaval for at least a year and a half.

Roy based his timeline on his supplier’s steel inventory for the next year and a half.

“After that, we would have to pay tariffs on steel because one component of the steel we use can only be found in Switzerland,” he said.

“The tariffs will not affect us unless they go on for a long time.”

Sweet Success

Jay Levine owns San Francisco Chocolate Factory, a Phoenix-based company with more than 28 years of experience.

His company currently employs four full-time staff members, who produce gourmet chocolates, fudge, and treats for special events and walk-in customers.

The chocolatier sources his ingredients domestically, making his business largely immune to tariffs.

“Everything I buy is local [or it] comes from the United States,” Levine, a Montreal native, told The Epoch Times.

He buys his apples from Washington, strawberries and nuts from other domestic suppliers. The American-grown items are not subject to import restrictions and are readily available.

The one exception is high quality Callebaut chocolate from Belgium, an ingredient that is now subject to a 10 percent import duty.

As he completes a new facility on Van Buren Street in Phoenix, Levine said his business has continued to do well despite the imposition of new tariffs.

“Quality really has no rights on it,” he said, “so you want to do top quality chocolates. All of our food products come from the United States.”

If tariffs continue, Levine said he “would switch to good [domestic] chocolate, which is locally grown here.” However, even that local supplier gets its cocoa beans from Ivory Coast.

According to the Observatory of Economic Complexity, an international trade data platform, the Ivory Coast’s main imports to the United States in January included cocoa beans valued at $161 million and cocoa paste valued at $41.7 million, followed by rubber valued at $19.1 million.

The U.S. government imposed a 21 percent tariff on goods from the tiny West African country, although it was paused for 90 days to facilitate negotiations. However, all U.S. trading partners are still subject to a baseline tariff of 10 percent.

Tariffs aren’t driving the current high prices though.

“I know that chocolate has doubled [in price] in the past year—and the reason for that was just price inflation,” Levine said. “I’ve never seen chocolate so high—ever.”

Levine expressed confidence that his company can endure the current tariffs, due to a steady demand for chocolate in America.

“This is an indulgence,” he said. “People will pay extra for it.”

That being said, “they won’t be buying as much chocolate“ under the tariffs, he predicted. ”Price is a factor.”

Don’t Tread On Me was founded in 2004 and American-made shirts and hoodies are the foundation of its clothing product line.

The exception are the company’s hats, which feature American motifs with the company’s signature coiled rattlesnake emblem.

“Right now, all of the hats and beanies are [produced] overseas, but I’ve been looking into domestic options,” company president Tyler Windes told The Epoch Times.

“There aren’t very many USA hat manufacturers, so it does make it difficult sourcing those.”

Windes said that even before the recent tariff changes, the company was considering moving its hat production to the United States.

“These new policies have simply reinforced our commitment and accelerated that timeline,” Windes said.

Sourcing his hats from a domestic manufacturer has been challenging, nonetheless Windes remains hopeful that the tariffs will lead to increased investment in American textile and apparel production.

This development would make it easier for companies like his to manufacture their products fully within the United States, he said.

A single death is a tragedy; a million deaths is a statistic.

The quote attributed to Joseph Stalin has become the modus operandi for attacks on President Trump.

Each day brings horror stories of specific victims allegedly caught in Trump’s dastardly web: the wrongfully deported migrant, the African child whose life-saving medicine is threatened, the promising young bureaucrat felled by Elon Musk’s axe.

Even accounting for the hyperbole that casts each illegal immigrant as an angel and every government program and federal employee as doing God’s work, these anecdotes do fall somewhere between unfortunate and tragic. Would you want to trade places with these people? Their stories pull on the heartstrings of Americans, a generous and compassionate people who recoil at suffering.

But their stories are also a cynical strategy deployed by those who seek to derail Trump’s reforms by trumpeting the ”tragedy” of isolated individuals. The same crocodile tears crowd that dismissed struggling Americans’ concerns about crushing inflation, the victims of sexual violence and human trafficking of children brought about by Joe Biden’s border policies, and massive job losses as mere “statistics.”

We do not know how President Trump’s reforms will shake out. Only his most devoted acolytes could have 100% faith in his unpredictable governing style. Still, there is a strong moral case for the spirit of Trump’s actions, which has been tendentiously ignored in coverage of his first 100 days.

A million deaths is not a statistic, but a million tragedies. Trump’s reform efforts hinge on the blindingly obvious premise that tomorrow’s pain will be far worse and more widespread if we do not act today. He is a doctor addressing a sick patient; his opponents seem happy to let the grave illness metastasize. Irony doesn’t quite capture the commitment of those who see existential threats around every corner and then ignore the clear and present dangers to our country.

A fiscal meteor is heading our way; everybody knows it. But our deeply secular ruling class seems to be banking on divine intervention to save the day. That speeding rock everyone can see is, of course, our national debt, which now stands at almost $37 trillion. We added $1.3 trillion to that total in the first half of the 2025 fiscal year. Since the Reagan administration, fiscal Cassandras have warned that our spending path is unsustainable. And yet, here we are. At some point, this looming threat will become a wrecking ball, forcing huge cuts in the programs hundreds of millions of Americans count on. Those who decry the knife Trump is bringing to government jobs and services are only setting us up for the chainsaw tomorrow.

Pay me now, or pay me later – but pay me you will. This isn’t politics, it’s math.

Everybody knows this, but only Trump seems willing to do something about it.

Thanks to Elon Musk’s Department of Government Efficiency, the waste, fraud, and abuse that infects so much government spending has become front-page news. These revelations should be a rousing call to action for everyone who believes in the necessity of government to improve people’s lives. They should be thanking Trump for trying to rescue their sinking ship.

Instead, they attack him. In an ideal world, Trump and Musk would be more measured in their assault on spending. They would have studied every program and job, delivering a detailed blueprint for reform. The political reality, of course, is that they had to move quickly. Our recent history has been filled with blue ribbon panels and special commissions on the deficit and debt that accomplished little. Act now, or never.

In a further irony, Trump’s progressive opponents are taking a page from the reactionary playbook, which years ago argued that, yes, slavery was wrong and integration was necessary, but change? Not just yet. In time.

The time is now because of the urgency of our crisis and because we finally have a leader who is willing to suffer slings and arrows to save us. Will Trump succeed? Ultimately, this will depend far more on the will of the people than on his vocal detractors in politics and the press. The cuts and reforms he has initiated are just the beginning. Getting our fiscal house in order will almost certainly require real, painful sacrifice from taxpayers and beneficiaries of government programs. It is still not clear if he has the will to do all that is necessary. If he does, history suggests that he will be punished instead of rewarded for this courage.

That doesn’t change the choice before us: some tragedies now or millions later.

J. Peder Zane is a RealClearInvestigations editor and columnist. He previously worked as a book review editor and book columnist for the News & Observer (Raleigh), where his writing won several national honors. Zane has also worked at the New York Times and taught writing at Duke University and Saint Augustine’s University.